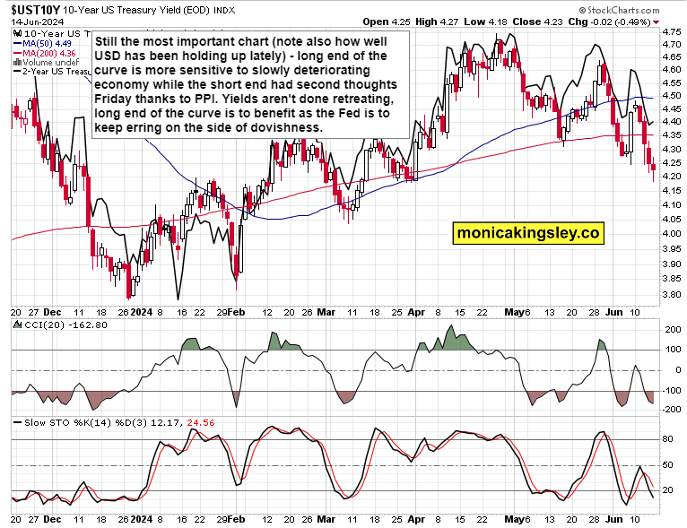

Why you should care about still lower yields

S&P 500 recovered from the opening drop, and also from weak consumer confidence data, but the distinct risk-off was there. This is what I wrote within Friday‘s stock market analysis for clients well before the data release:

(…) 5,385 is support remains out of reach, and sellers will have a hard time breaking below 5,400 today. Weak UoM consumer sentiment (likely to come in weak) and consumer inflation expectations (likely not to be as weak as PPI let alone the relevant CPI) would help stocks rally and keep no rate cut move odds for Sep below 29%. In the context of being short-term overbought, we need to watch whether bullish reaction to the incoming data gets overpowered that soundly as yesterday, or whether the dip would be less profound (the latter looks more likely, but BoJ has added to risk-off sentiment today, making for a trappy, volatile day where swing traders would prefer to stand aside).

For all the market breadth warning signs, the bull run in equities isn‘t over, it would be premature to turn bearish just here. Just as I have written in Thursday‘s extensive analysis, PPI and consumer confidence data confirmed the rising Treasuries trend and ultimately dovish interpretation of Wednesday‘s FOMC. Rightfully so.

(…) If you looked at equities, bonds and the dollar yesterday, what was a greater driver? CPI or FOMC? Here are the inflation readings and what kind of moves they spawned across the three assets, and how these moves were then merely retraced during Powell.

Next week is bringing us Empires State manufacturing, retail sales, and then SNB and BoE with more PMI data from the Old Continent before the same are released Friday for the States. I‘ll make these predictions and cover them including the market reactions for clients as we go.

Here comes the key chart with USD doing quite well last week (digesting the headline NFPs from preceding Friday and not slumping on retreating yields, hello Europe) – let me just say that the decline in yields isn‘t about strengthening economy. To the contrary, unemployment claims initial and continuing are picking up, consumer sentiment (soft data) is weak, and retail sales (hard data) would definitely cast more light on willingness and ability to spend while XLY remains objectively strong.

Source: www.stockcharts.com

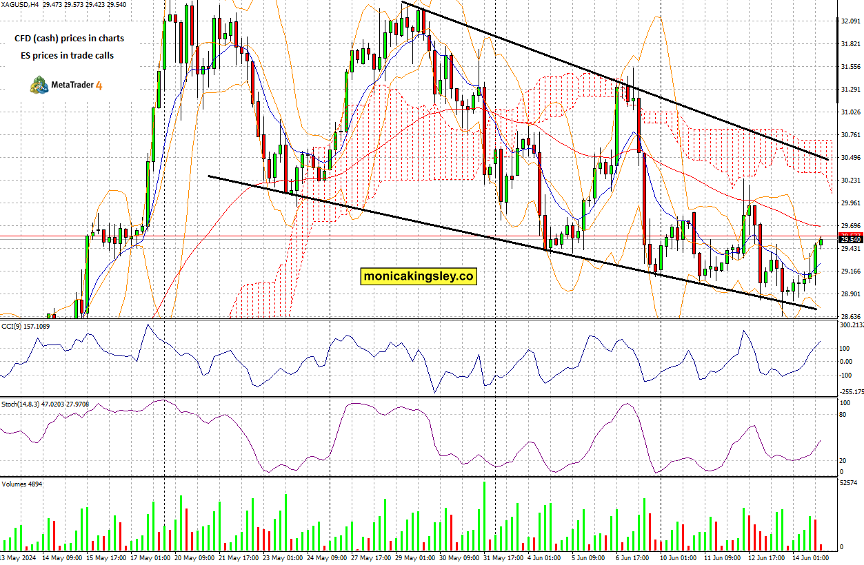

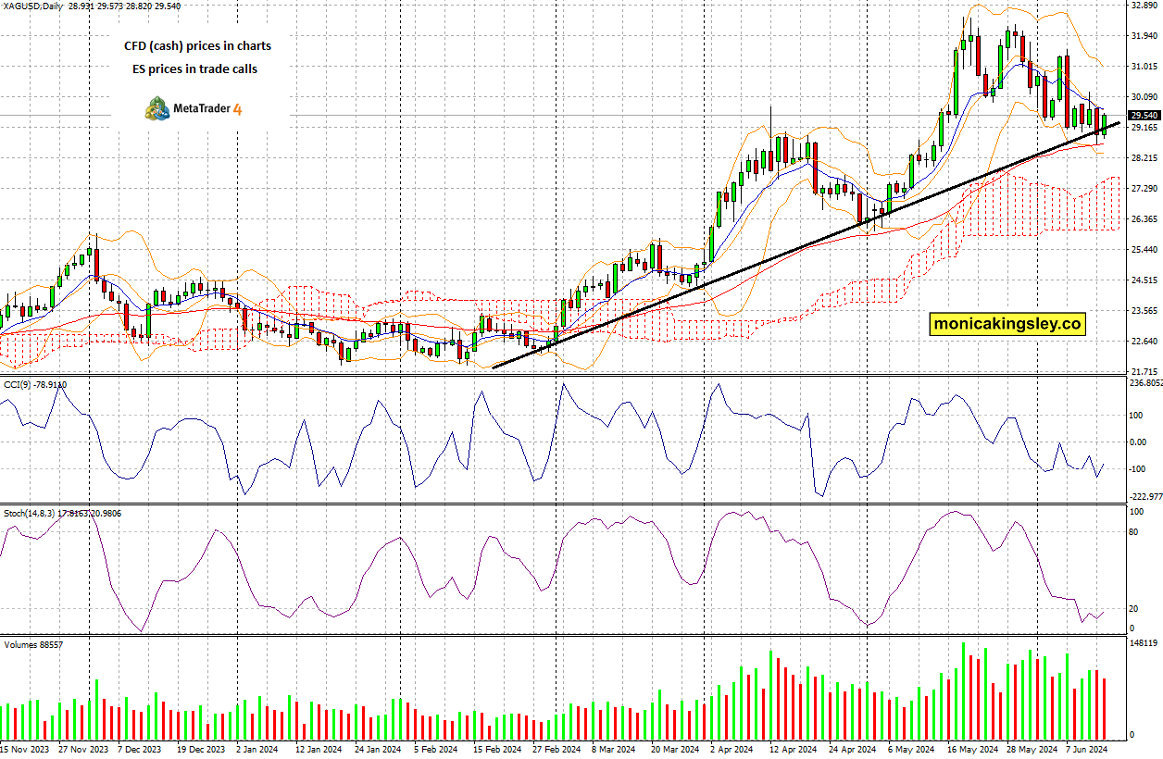

Gold, Silver and Miners

Miners are lagging, yet last two days offer signs of starting accumulation – the real move is though still to play out in gold and silver. Friday‘s session has been very encouraging, especially in the way silver caught up to gold‘s relative outperformance since last Friday – as you can see from the below two charts, the reversal and reclaiming of the broken rising support line on the second chart, was badly needed. Now, there comes brief consolidation following this sellers‘ fatigue with upside resistance at roughly $30.50 spot if you go with a wedge chart pattern.

Source: www.stockcharts.com

Source: www.stockcharts.com

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.