Why the Indonesian Rupiah is suddenly flashing warning signs for global markets

The Indonesian Rupiah is sliding deeper into uncharted territory. The problem here isn’t just the Rupiah, but the increasing signs that market pressure is overpowering policy action, bringing back painful memories for many emerging currencies in Asia.

After falling to fresh all-time lows against the US Dollar, pressure on Indonesia’s currency intensified again this week even as Bank Indonesia delivered a surprise 50 basis point rate hike in an attempt to stabilise markets and slow capital outflows.

Under normal circumstances, such an aggressive move might have been enough to calm investors.

This time, markets barely blinked. And that may be the most important signal of all.

Because the Rupiah’s weakness is no longer just an Indonesia story. It is increasingly becoming part of a much bigger global macro narrative, one driven by surging bond yields, persistent US Dollar strength, geopolitical tensions and growing concerns that the era of easy money is finally coming to an end.

The strong Dollar problem is back

Emerging market currencies tend to struggle when three things happen at the same time:

- US Treasury yields rise,

- the US Dollar strengthens,

- global risk appetite deteriorates.

Right now, all three are happening simultaneously.

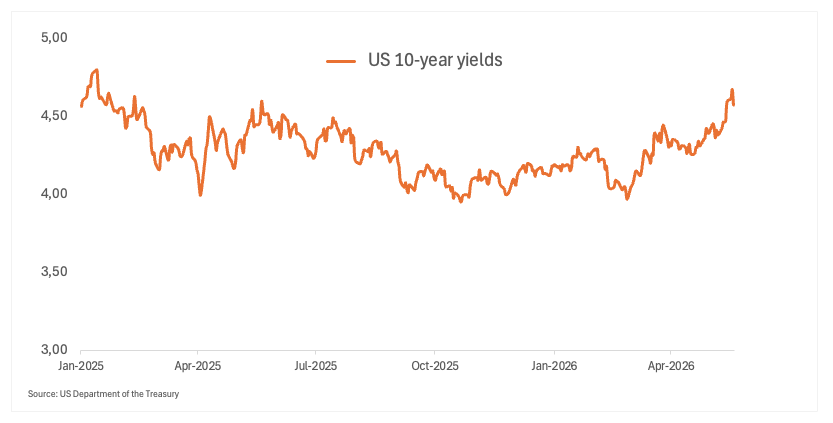

US yields have climbed sharply in recent weeks as investors reassess how long the Federal Reserve may need to keep interest rates elevated. At the same time, geopolitical tensions in the Middle East have supported safe-haven demand for the Dollar while keeping energy prices volatile.

That combination is uncomfortable for many emerging markets.

But Indonesia is particularly sensitive because the country relies heavily on foreign capital inflows to help finance its economy and bond market. A stronger Dollar and higher US yields make Indonesian assets relatively less attractive while increasing pressure on the Rupiah.

As capital starts flowing back toward safer US assets, emerging market currencies often become the first casualties.

Bank Indonesia is trying to defend confidence

Bank Indonesia’s decision to raise rates by 50 basis points highlights how seriously policymakers are taking the situation.

The move was aimed at:

- supporting the Rupiah,

- limiting imported inflation,

- restoring investor confidence,

- slowing capital outflows.

But aggressive rate hikes come with their own risks.

Higher borrowing costs can weigh on domestic growth, pressure consumers and complicate investment activity at a time when the global economic backdrop is already becoming more fragile.

That leaves policymakers walking a very difficult line: raise rates too slowly and the currency risks falling further, raise them too aggressively and the domestic economy could begin to weaken more sharply.

The Rupiah is becoming a global liquidity stress gauge

What makes the current move particularly interesting is that the Rupiah increasingly looks like a barometer for something much larger than Indonesia itself.

Markets are starting to price a world where:

- global borrowing costs stay higher for longer,

- central banks have less room to support growth,

- fiscal deficits continue expanding,

- geopolitical risks keep inflation pressures alive.

That environment tends to expose vulnerabilities across emerging markets very quickly.

And investors know this story well.

Periods of persistent Dollar strength and rising US yields have historically created stress across emerging market currencies, particularly in economies dependent on foreign investment flows.

That is one reason why memories of past Asian currency crises inevitably begin resurfacing whenever currencies such as the Rupiah come under heavy pressure.

Japan may also be adding to the pressure

Another important dynamic may be quietly building in the background.

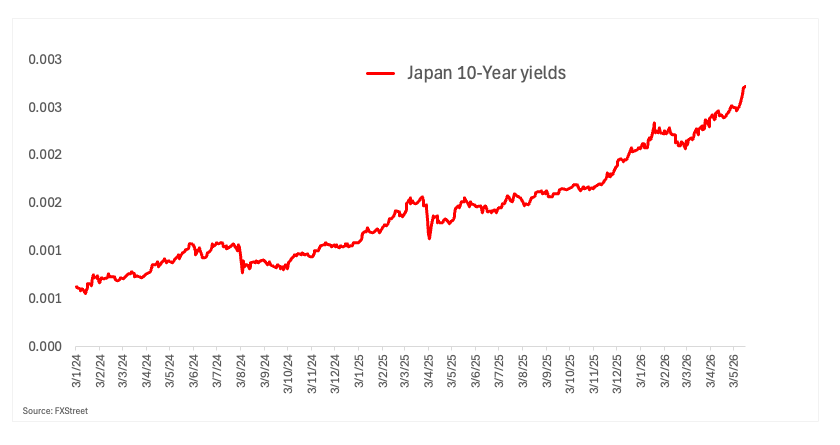

Japan’s bond market has seen a dramatic rise in yields, with Japanese Government Bond yields climbing to multi-decade highs. That raises the possibility that Japanese investors could gradually begin shifting capital back home after years of investing abroad in search of higher returns.

If that process accelerates, emerging market assets could face another headwind.

For years, abundant global liquidity helped support higher-yielding emerging market trades across Asia.

If Japanese money starts retreating while US yields remain elevated, the environment for currencies such as the Rupiah becomes even more challenging.

This is about more than Indonesia

The deeper issue is that markets may be entering a very different financial regime from the one investors became used to over the past decade.

For years, cheap global liquidity masked many vulnerabilities across markets. Now, higher yields, stronger funding costs and geopolitical uncertainty are beginning to expose them again.

The Indonesian Rupiah may simply be one of the first warning signs.

If pressure on emerging market currencies continues building despite aggressive central bank action, investors may soon begin asking a far more uncomfortable question:

What happens if the world is no longer flooded with cheap money?

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.