Who Faces the Risk of Collateral Damage from U.S. Tariffs?

Taiwan Appears to Have the Most to Lose

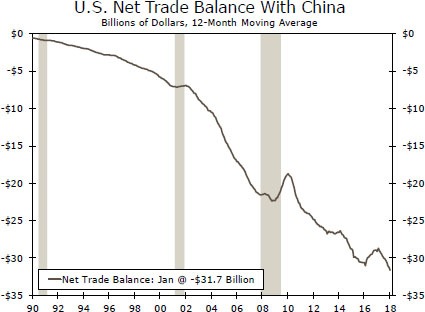

The bilateral trade deficit that the United States incurs with China has widened significantly over the past two decades (top chart). Indeed, the red ink that the United States racked up with China totaled $375 billion in 2017, nearly one-half of the total American trade deficit in goods last year.

Due in part to this bilateral trade deficit, the Trump administration recently announced tariffs on Chinese goods that will affect at least $50 billion worth of goods, and China has responded with some modest retaliatory measures. In a worst case scenario, tit-for-tat retaliation, should it develop, could spiral into an all-out trade war between the world's two largest economies. China generally imports raw materials and unfinished products, assembles the inputs and exports finished goods. As shown in the middle chart, China incurs sizeable deficits in trade in primary products and large surpluses in trade in manufactured goods. In the event of a trade war, Chinese exports to the United States could be significantly affected. Consequently, countries that export raw materials and intermediate inputs to China could be indirectly affected by a Sino-American trade war. Which countries would be most at risk of collateral damage?

To answer this question, we turned to the Trade in Value Added (TiVA) database that is compiled by the Organisation for Economic Cooperation and Development (OECD). Our analysis shows that Taiwan would be the economy with the most to lose from a trade war between mainland China and the United States (bottom chart). Specifically, products that are exported from Taiwan to the mainland, assembled into final products and subsequently re-exported to the United States account for 1.5 percent of total value added in Taiwan. This finding makes intuitive sense due to the significant amount of exports from Taiwan to the mainland, which in 2017 totaled almost $90 billion (nearly 30 percent of total Taiwanese exports). Taiwan is followed by Korea, Malaysia and Hong Kong. With the exception of Chile, South Africa and Costa Rica, all the countries with the most indirect export exposure to the United States (via exports to China) are in Asia.

There are some caveats to keep in mind. First, the most recent data in the TiVA database are from 2011. (The database is very extensive, and the OECD does not update it on a regular basis.) Given solid growth in Chinese exports to the United States since 2011—they grew 4 percent per annum between 2011 and 2017—indirect export exposure to the United States is probably a bit higher today than in 2011. That said, none of the countries in the bottom chart, with the possible exception of Taiwan, have so much indirect export exposure to the United States that they would be at risk of recession from a Sino-American trade war. And if cooler heads prevail in Washington and Beijing, then the risk of even a modest slowdown in economic growth in those countries would recede even further.

Author

Wells Fargo Research Team

Wells Fargo