When economics don't work: Inflation and exchange rates

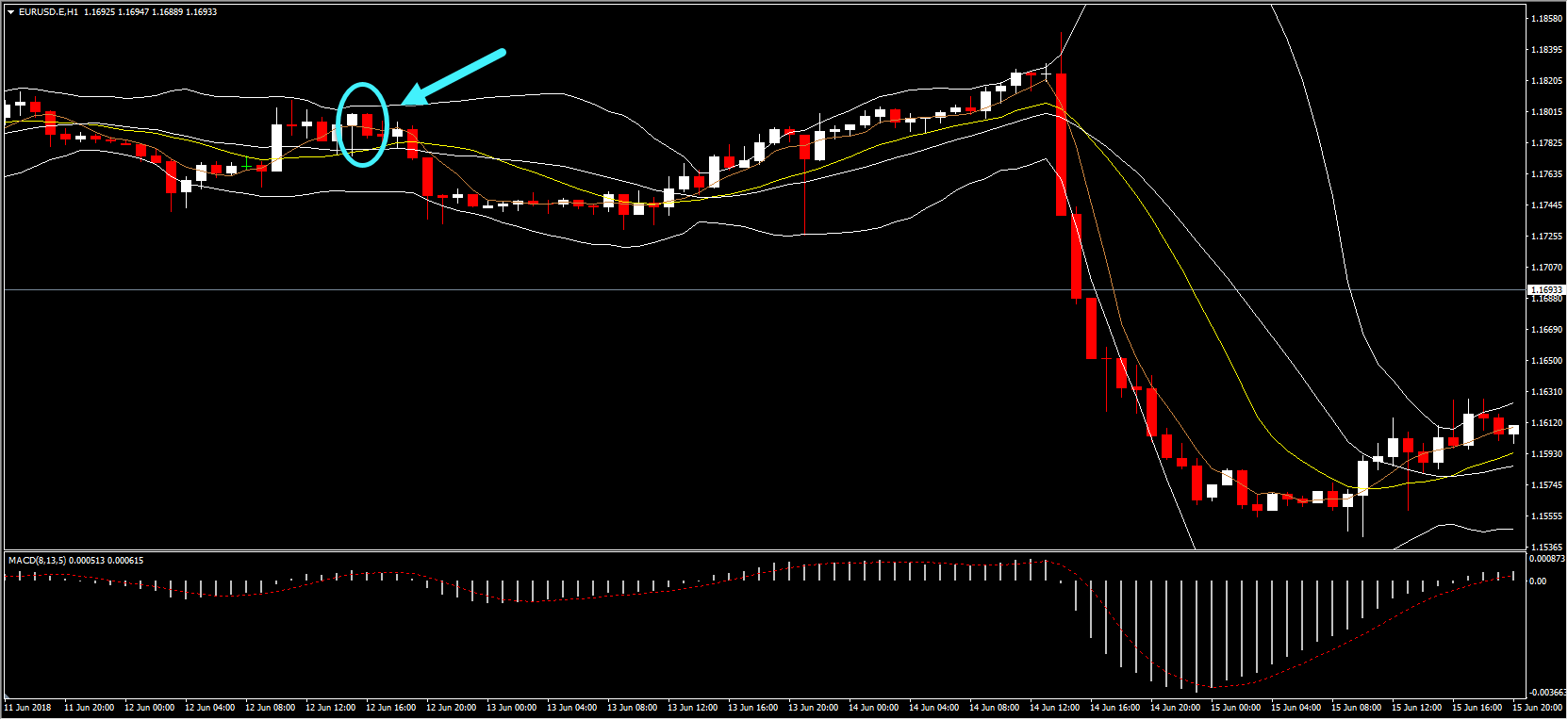

We’ve been adamant that when it comes to trading on the news, what matters is the difference between expectations and actual data. As we have already shown, exchange rates should react to any sort of data surprise, either positive or negative. If no surprises are recorded, then we would expect no change in the exchange rate. For example, the June CPI figure came out on June 12, 12:30 GMT, almost exactly as predicted, with only a small change in the YoY figure. As you may see from the figure above, no significant changes have been recorded in the exchange rate.

In contrast, on September 13, all CPI measures were less than expected. Economic theory would suggest that the USD would appreciate, given that, again, in theory, investors would have to correct their previous, worse than expected projection. However, the reaction was negative for the USD, as it registered a large drop in value. How is that possible?

Was anything wrong with data release? From what we tell, not really. Furthermore, previous data releases should have supported an appreciation of the USD. Average Hourly Earnings actually came out higher than expected at 2.9% YoY, compared to expectations of 2.7%. At the time of the announcement, the USD gained approximately 50 pips. Following this response, the market should have revised its perceptions about future inflation upward given that there should be a positive relationship between inflation and wages. According to theory, lower actual inflation compared to higher predicted inflation should appreciate the USD. This didn’t happen though.

Why did the USD depreciate when theory suggested that it should have appreaciated?

In reality, the answer is that, often more times than we expect, markets do not abide by economic theory. The reason is that economics teaches using a system of beliefs which, by definition, cannot abide to changing market conditions. Remember that inflation occurs because production cannot keep up with changes in demand, as it is more-or-less fixed in the short-run. As such, inflation would increase if demand increases and vice versa. Thus, the higher consumption and spending is, the higher inflation will be. Too much inflation can be bad but there has really been no research pointing out whether a 2% level of inflation is worse than a 3% level of inflation. Thus, markets can interpret lower inflation as a sign that growth does not move as fast as it was expected. Naturally, this does not abide to the inflation differential story which dictates that the higher the inflation rate, the more the exchange rate would depreciate.

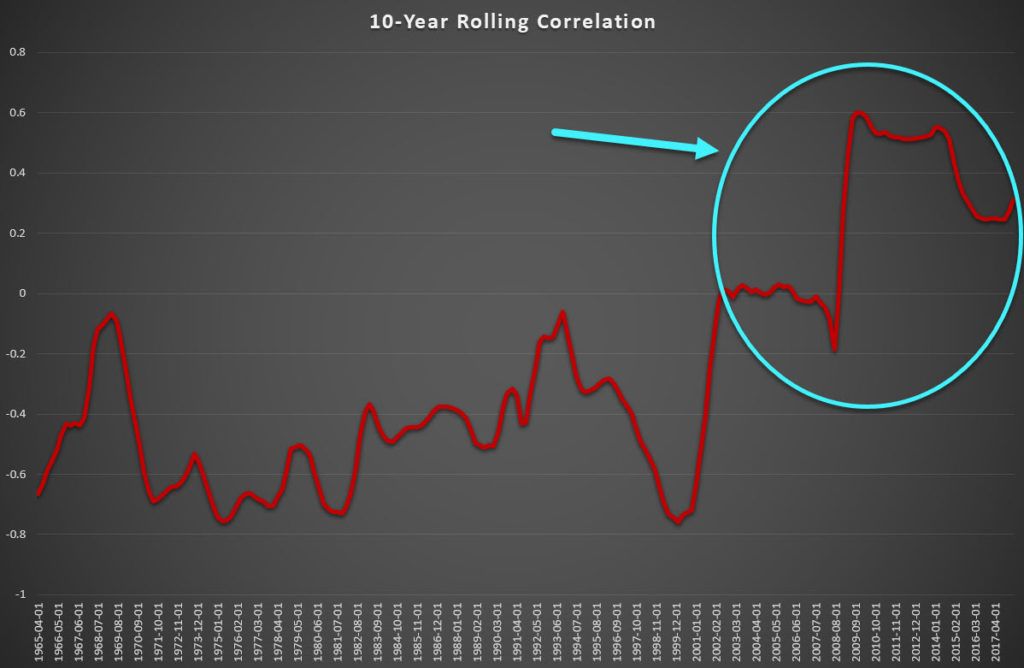

The market reaction could be linked to a more psychological reason: in the aftermath of the 2008 financial crisis, the inflation rate was very closely linked with growth, much more than ever before. Using a 10-year rolling correlation, the following graph suggests that the relationship between growth and inflation has actually changed, moving from negative to positive since the early 2000s and especially since 2009. Why does this happen? Is it just a reaction to inflation stability, good central bank policies and, more so, the economic rebound since the Global Financial Crisis? Most importantly, will this positive relationship persist or will it return to negative in the future?

Truthfully, we cannot answer that question; in addition, nobody can. It is up to the trader to monitor the market and the evolving relationships between variables and try to reach their own conclusions. Economics can provide a good starting point for understanding how markets work, but we also need to understand that this does not necessarily mean that what it dictates holds all of the time. Practical experience, skin in the game, is the only way traders can be successful in adjusting their strategy when market patterns change. In Keynes’s words “When facts change, I change my mind. What do you do?”

Author

With more than 4 years of experience at the Central Bank of Cyprus where he obtained hands-on experience with real-life economics, Dr Nektarios Michail is a supporter of a balanced approach between science and art when it comes to