Fed quantitative tightening: What does it mean for the Dollar, Stocks, Bonds & Gold?

The Fed’s “balance sheet reduction” may have profound implications for the dollar, gold, stocks and bonds. We’ll provide an outlook.

It is said forecasts are difficult, especially when they relate to the future. Investors might want to pay attention nonetheless, not so much because I believe I have a crystal ball, but because investing is about managing risk. And there’s a risk that I’m right.

Quantitative Tightening

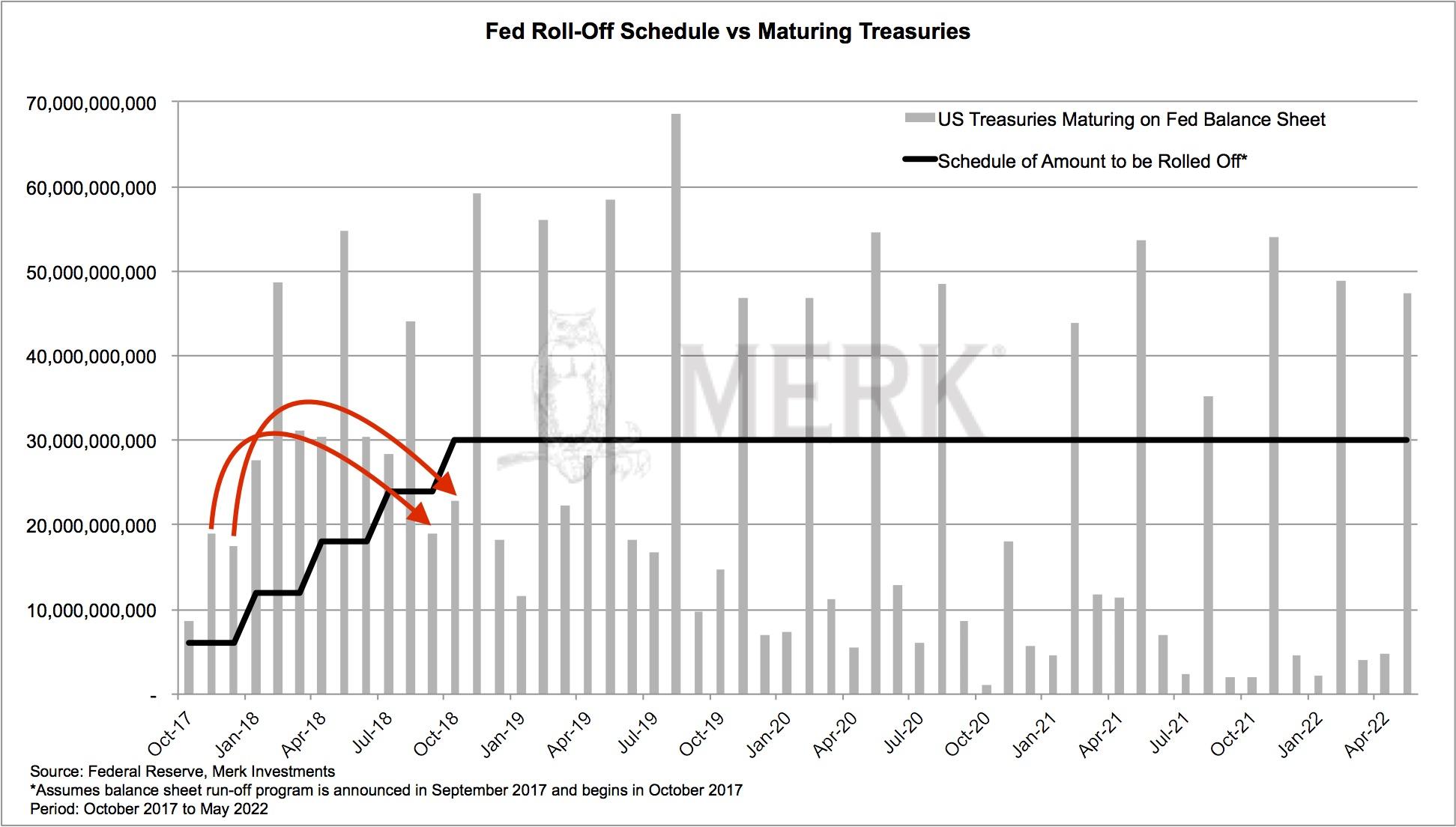

There’s a lot to cover, so let’s start with what is perceived to be the elephant in the room, the Fed. In suggesting that the Fed would soon initiate balance sheet reduction, Fed Chair Janet Yellen indicated it would be like watching paint dry on a wall. Duly observant, numerous pundits agreed. With due respect, that’s a bunch of baloney, but judge for yourself. Unless markets fall apart in the coming weeks, we expect that the formal announcement for the Fed’s balance sheet reduction will be made this September, with a gradual stepping up in the amount the Fed will allow to “run off”, i.e. the amount of maturing bonds it won’t re-invest. The Fed has left many details open to interpretation, but looking at Treasuries alone, at first, $6 billion may be allowed to run off; this is gradually stepped up until $30 billion a month may be allowed to run off. It’s not clear at what duration maturing bonds will be reinvested that are above the threshold, but it is plausible to roll those excesses to “fill the gaps” in subsequent months. Differently said, it’s perfectly possible that the Fed will indeed allow $30 billion in Treasuries to run off once the program is fully deployed:

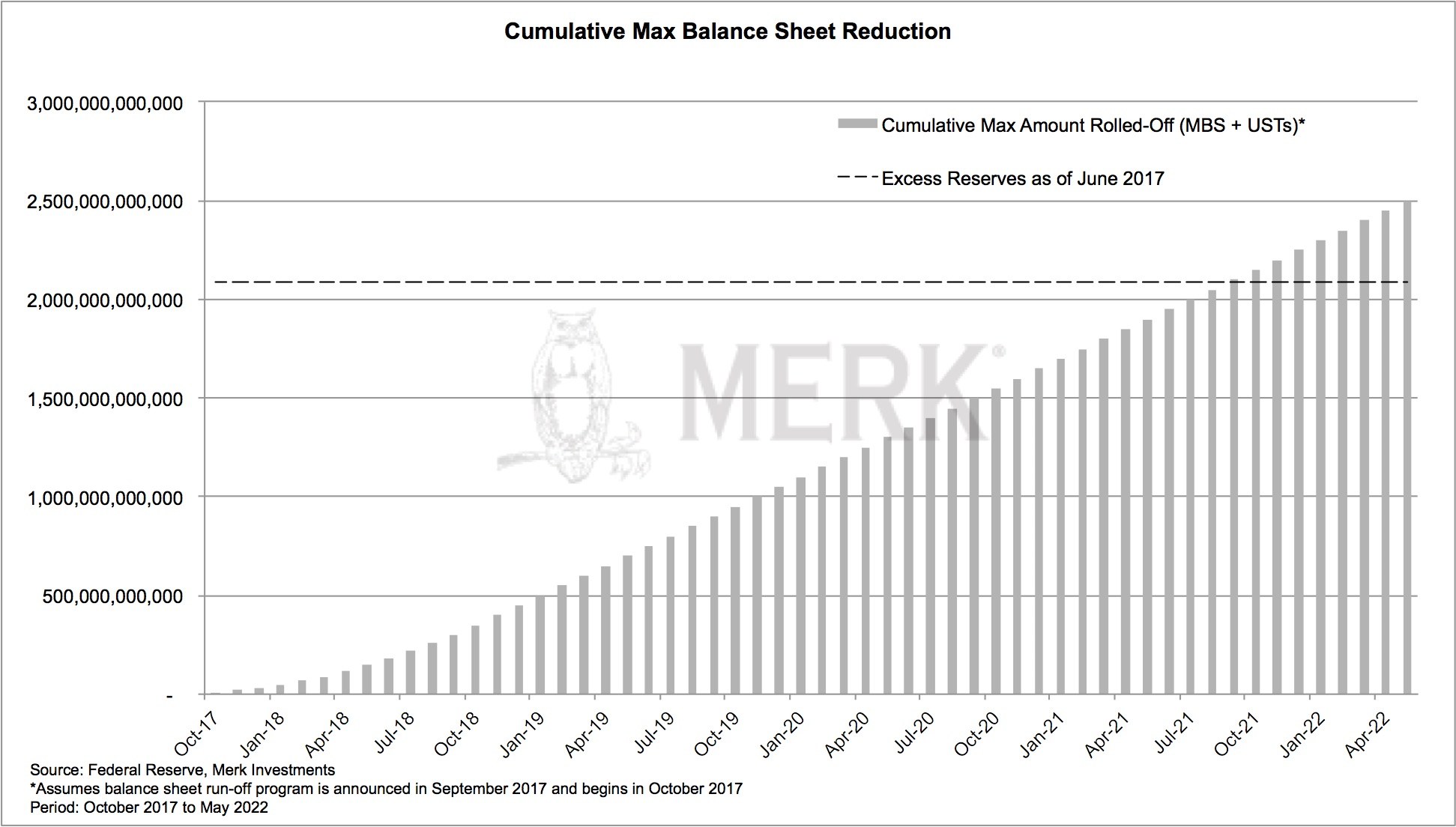

In addition, the Fed will allow mortgage-backed securities to run off (MBS). There’s really no good reason to look at Treasuries and MBS in isolation; as such, the balance sheet reduction would be $50 billion a month if the program were to be fully deployed:

The Fed hasn’t announced how small a balance sheet they want to have; based on our interpretation of discussions of current and former policy makers, this is because the Fed neither knows, nor agrees of where they want to take the balance sheet. It apparently doesn’t stop the Fed from preparing the markets that they embarking on this journey because they believe they have years to make up their mind. Notably, as can be seen from the chart above, they might have until 2021. Basically, the Fed can reduce its balance sheet until excess reserves have been eliminated (this level varies on economic activity; the dashed line represents the current level of excess reserves and the potential maximum reduction holding all else equal). Whether the Fed will try to get excess reserves to zero or some other amount is an open question that not even the Fed appears to be able to answer internally.

A more convincing argument I hear as to why low volatility is structural may be that information nowadays gets absorbed more quickly. On the one hand, we have computers scan the news in milliseconds, often trading without human intervention. And we have more computing power, allowing for a more efficient implementation of any investment process. Market makers in exchange traded funds also help in the execution efficiency of markets, possibly exerting downward pressure on volatility. However, let's not forget that volatility lowered in this fashion may have the same implication as low volatility in the building up of any bubble: it is the perceived risk that is lower, not actual risk. Machines are fantastic at certain aspects, be that keeping spreads tight in an exchange traded fund, or scanning Twitter for keywords. Trades initiated in this fashion provide liquidity to the markets, but that liquidity can evaporate rather quickly when the machines go off-line. Let there be a glitch in the markets for whatever reason (say, someone dumps a large number of derivatives in off hours), and today's incarnation of automated traders tend to wait it out. In the meantime, stop loss orders of other market participants may be triggered, possibly causing flash crashes.

If reducing the Fed’s balance sheet at a rate of $50 billion a month is akin to watching paint dry, what then is the ECB’s activity of purchasing €60 billion a month (its current rate)? Either the Fed or the ECB is pulling our leg here. If printing money is quantitative easing (QE), then balance sheet reduction is quantitative tightening (QT). There has been a lot of debate of what sort of impact QE actually has. Skeptics of QE have pointed out that all bonds trade relative to one another, i.e. an MBS might be a substitute to a Treasury bond which in turn might be a substitute to a German bund; applying a given spread, one can take that exercise further to any number of seemingly “safe” bonds, recognizing that safety is not an absolute concept (and from a US regulatory point of view, only US Treasuries are considered “safe” as the US government can always print money to pay it back). It’s in this context that the buying of MBS has been criticized as a useless digression from monetary into fiscal policy. Useless because spreads between MBS and Treasuries haven’t been meaningfully impacted; and a digression into fiscal policy because buying MBS rather than Treasuries is fiscal policy given that credit is allocated to a specific sector (housing) of the economy, something in the domain of Congress, not the Fed.

So has Yellen suddenly become a critic of QE by suggesting QT is akin to watching paint dry? I doubt it; much rather, the Fed does what it continuously has been doing since the financial crisis: try to convince the markets with words. If the Fed tells you, rates rather than QT is the primary tool to set rates, it must be true, right? Please just look at the rates, ignore everything else. In the meantime, across the pond at the ECB, Draghi will tell you with a stern look that QE is responsible for everything good that has happened in the Eurozone (and that he isn’t responsible for any bad side effects). You shall be excused if you are scratching your head.

It’s all about risk premia

I am in the camp that believes QE has been all about compressing risk premia, i.e. the spreads between risky and so-called safe assets. With QE, junk bonds trade at less of a premium over bonds; with a #WhateverItTakes attitude, peripheral Eurozone bonds trade at less of a premium over German bunds. And equities trade at higher valuations and lower volatility? Sound familiar? Not too surprisingly then, the market has had some tantrums when the Fed first started talking about tapering; or when the Fed indicated it might start raising rates.

I’m not alone with this theory; the Fed and other central banks appear to have been petrified that stepping back from ultra-accommodative policies would cause a major revolt in the market. But then magic happened: the market presented the Fed rate hikes on a silver platter. And with two rate hikes out of the way this year, the markets are still holding up. As the markets are holding up, central bankers feel like day traders on a winning streak: they must be geniuses!

Borrowing from the picture depicting Yellen on the pressure cooker above, though, I would caution central bankers not to do a victory lap quite yet. In my mind, to stay with the analogy, some steam has been let out of the pressure cooker; and with the Fed ever more falling behind the curve, the illusion may have been created that real interest rates are moving higher, when indeed only nominal interest rates are moving higher. With QT, think about the pressure cooker shrinking while the contents remain the same; if the content of the pressure cooker is a bunch of hot air, it is well possible to further compress it.

What I’m arguing here is that QT will increase risk premia. Before we discuss implications of rising risk premia, let’s consider what’s happening at other central banks.

The real elephants

Above, I write about the Fed being “perceived” elephant. Only the perceived elephant, as the Fed may well have freed the shackles from other elephants, meaning the Fed may have enabled other central banks to step away from their ultra-low monetary policy. Some of those pressure cookers have cracked open now, notably the ECB’s.

The ECB’s program to purchase €60 billion in securities each month is running through the end of this year. As such, the market is expecting that in September, possibly a bit later, the ECB is going to announce what will happen thereafter. It appears Mr. Draghi, possibly emboldened by what’s happening at the Fed (although central bankers would never express it this way; it’s of course domestic considerations they are evaluating), he recently said:

“As the economy continues to recover, a constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments – not in order to tighten the policy stance, but to keep it broadly unchanged.” ECB speech by ECB President Mario Draghi, June 27, 2017

You read this correctly: the ECB will remove accommodation, but it won’t really and it won’t call it tightening. Think: watch paint dry on the wall. He tried to pull a Yellen! You can’t make this stuff up. In some ways, it reminds me of the dot-com bubble, where companies told analysts what to write into their reports, so as to avoid the necessity for analysts to actually do any thinking of their own.

Except the market didn’t take Draghi’s bluff and German Bunds sold off. Less than a year ago, Bunds traded at negative yields; in the aftermath of Draghi’s comments, they surged from roughly 0.25% to over 0.50%. A big jump for those that watch those markets. In contrast, U.S. Treasuries are yielding 2.37% as of this writing.

Historically, the spread between U.S. Treasuries and German Bunds are highly correlated to the exchange rate between the Euro and the U.S. dollar. As German Bunds are falling (yields rise), the euro has had a tendency to rise when U.S. long-term rates don’t move much. Not surprisingly, the euro has rallied quite a bit as part of this ECB induced mini taper tantrum.

To assess where we go from here, consider the following:

-

What happens to Treasuries? Some argue QT will cause Treasuries to fall. My take: no, risk premia will rise. More on assets below, but w.r.t. to Treasuries rising risk premia imply deteriorating financial conditions, a headwind to economic growth. That is, Treasuries may end up not changing all that much, possibly even rise.

-

What happens to Bunds? According to a standard deviation band we monitor, Draghi’s comments caused Bunds to fall by 2 standard deviations versus their historic trend. That’s significant and suggests real news (his speech!) caused the change. But what about going forward? Is all unwinding already priced in? This possibility cannot be ruled out, as Treasuries had their highest yields after the taper tantrum in 2013. My take is that Bernanke announced tapering not because the U.S. economy was in great shape, but because Bernanke’s term was coming to an end, and he wanted to tie up loose ends. In the U.S., we’ve had several faulty starts to reform, most notably expectations priced in upon President Trump’s election which have since fizzled out. In contrast, reform in the Eurozone is real and ongoing, most recently with French President Macron being elected not only on a strong reform platform, but also with the accompanying majority to be able to implement it. I’m not suggesting reform in the Eurozone will be perfect – it never is; but I am suggesting that real rates have room to move higher, especially relative to U.S. rates, as progress is being made.

Other central banks around the world may also be emboldened to take the foot off the accelerator. The biggest potential to catch up may well be in Sweden, where we have said for years that policy is too accommodative.

You can call the weak dollar a deflating Trump trade, but the Fed may well have initiated a far greater force by enabling other central banks to tighten. Well, don't’ count on Japan to follow suit just yet.

Implications for stocks

Stocks are historically correlated to junk bonds, not because they are junk, but because they are both so-called risk assets. Just as their volatility has been compressed with QE, we believe their volatility should rise with QT. We have recently opined as to whether this time is different and volatility will remain low, but the short of it is: don’t count on it.

Outbursts in the tech sector are, in the opinion of yours truly, the canary in the coal mine. The buy-the-dip mentality is wearing thin. Similarly, the end of day buying that had become routine may have turned into end-of day selling on several occasions of late. Does that mean that there isn’t value out there somewhere? Possibly, but don’t come crying to me if you lose money holding stocks in this environment.

Implications for gold

With rates rising, should the price of gold decline? I can see Eurozone based investors getting less enthusiastic about gold as the euro has been rising. That said, rising risk premia may be a positive for the price of gold. Because gold does not have cash flow, there’s also no greater discounting of future cash flows as risk premia rise. In contrast, stocks may well be under pressure as risk premia rise. This is an academic way of saying that gold may be a valuable diversifier should stocks suffer.

Closing thoughts on Fed balance sheet

Advocates of a smaller Fed balance sheet have praised the Fed’s moves to commit themselves to a reduction, making it more difficult to reverse course, especially since they have stated that interest rate policy will be separate from deciding on the size of the balance sheet. With due respect, I can’t get myself to believing in the tooth-fairy anymore. First, let’s keep in mind that we are likely to get a new Fed Chair early next year, meaning lots of options are on the table as to what direction a new Chair would take. More importantly, by not providing more specific parameters as to where the Fed wants to take the balance sheet, I would not be surprised if the Fed were to reverse course sooner rather than later. They won’t blame it on falling stocks, but on deteriorating financial conditions (the latter may well be Fed talk for the former).

Author

Axel Merk

Merk Hard Currency Fund

Axel Merk is the Founder and President of Merk Investments. Merk is an expert on macro trends, hard money, international investing and on building sustainable wealth.