The Dollar demise question: What’s different this time?

How did we get here?

The dollar’s dominance has had rock-solid foundations since WWII: the largest economy, the largest importer of goods, the largest financial system, the first military. And for the first 26 years of that era, it was by law the reference point of the international monetary system, the only currency whose price was fixed to gold and against which all others were priced.

No Dollar hedge in this stock market shock

Despite this overwhelmingly dominant position, the US generally chose to exercise its leadership not unilaterally (“America alone”) but through international institutions and agreements that it instigated: the Bretton Woods Institutions, the GATT, the Plaza and Louvre Accords, the G20 among others (“America first”). This meant taking the time to work with allies and others to build consensus around America’s goals. When a global crisis erupted, others looked to US leadership to help coordinate a solution to it, as it did with the Brady plan following the Latin American debt crisis in the 1980s, or the IMF-led rescues following the Russian default Asian and Russian debt crises in 1997-98.

On rare occasions, America chose to cut through consultation and consensus-building and acted alone. In foreign and military affairs, this happened repeatedly over the decades. But in international economics and finance, this happened very rarely. In fact, there is really only one precedent in scale to this year’s abrupt volte-face on trade policy: President Nixon’s 1971 decision to take the dollar off the gold standard and thereby end the Bretton Woods System of exchange rates.

Then, like now, the US’s international partners were shocked and dismayed by both the substance and form of this decision and it took a few years of skilled and intensive international economic diplomacy to repair the damage. Yet, the dollar’s dominant role in the international monetary and financial system not only endured, but arguably strengthened even further, even though it had lost its “de jure” basis and remained only “de facto”.

So what is different this time? Five critical elements:

First, geopolitics: back in the 1970s, the largest reserve holders and financial centers were all firmly part of the US-dominated Western block in the Cold War. This is no longer the case.[1] And the US itself has raised questions about continuing to provide security to hitherto allies.

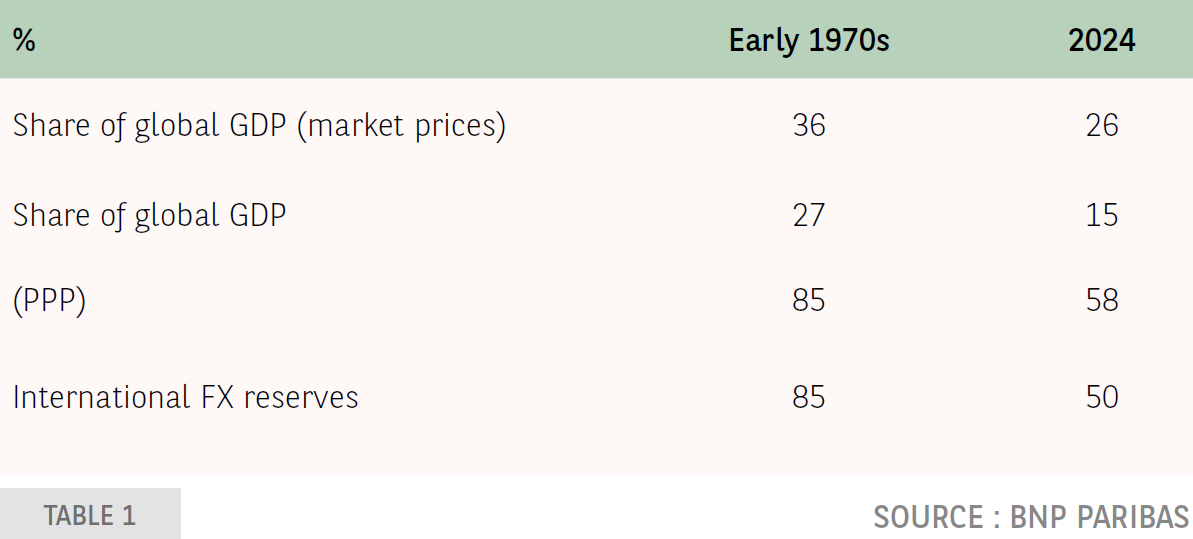

Second, in relative terms, the extent of US economic and financial dominance has declined meaningfully. And while there is still no single credible alternative in the sense of one economy combining all the attributes of the 1970s’ dollar that could aspire to replace it, there are now a number of options for diversification that didn’t exist then, most notably the euro.

United States: A declining share of the pie

Third, policy credibility. While in 1971, like now, the macroeconomic imbalances dogging the US were primarily of its own making, back in 1971 there were no concerns about public debt sustainability (debt to GDP ratio was 35%), policy unpredictability or unreliability of trade deals signed, nor concerns about rule of law being overtly challenged by the Executive. Granted, Federal Reserve (Fed) independence got tampered with then too, and indeed holders of Treasuries experienced negative real returns in the ensuing decade. But the lesson has been learned, and in fact President Trump’s attacks on the Chair of the Fed since returning to office have been a key motive of concern for US debt holders, including but not limited to FX reserve holders.

Fourth: dependance. While in the 1970s, the US was still a net creditor to the rest of the world, its Net International Investment Position (NIIP) is now negative by about 90% of GDP, more than double its level of even just 10 years ago. This means the US is now heavily dependent on the proverbial kindness of strangers to finance its economy. Foreigners hold nearly 20% of US equities and 30% of its public debt (respectively an all-time high and 3x the 1971 share).

Fifth: optionality. Most countries nowadays have floating exchange rates. That means they don’t actually need to hold large amounts of reserves, or at least not as large as they do. In principle they could run them down or hold them in any currency they wished as long as it provided reasonable safety and liquidity. Indeed, this explains why some diversification away from the dollar has already been taking place since the turn of the 21st century, albeit at a glacial pace and principally to the benefit of gold and minor reserve currencies like the Nordic Kronas or the Canadian and Australian dollars (see chart 2). The euro’s share meanwhile has been steady around 20%. This stability largely reflects the fact that euro and dollar shares of export invoicing and foreign debt issuance have also been relatively steady over the last 25 years.

Where to from here?

It is important to distinguish between the role of the dollar in the international monetary and financial system and the dollar exchange rate. In both cases, foreigners have agency, but the outcome will be overwhelmingly determined by choices made by US policymakers.

-638820702138740379.png&w=1536&q=95)

International reserves system

The role of the dollar in the system will depend on whether the safe haven properties of the currency are protected or undermined further.

This is a matter of preserving Fed independence, putting public debt back on a sustainable path, ensuring unquestioning respect for the rule of law, and firmly ending speculation about taxing or coercing foreigners for the privilege of holding dollars as reserve assets.

Having let these genies out of their respective bottles, the US government will need time and sustained commitment to lead them back in. Reaffirming commitment to the reserve status of the dollar as US Treasury Secretary Bessent has done recently is helpful but not enough. In the meantime, it’s reasonable to expect an acceleration of the pre-2025 diversification trend.

Given the overwhelming advantage of US debt markets in terms of depth and liquidity, and the interest of reserve holders in keeping the process orderly (to avoid large capital losses and financial stability problems), even this accelerated diversification is likely to be barely noticeable to the naked eye. Even so, accidents can happen, and the US may well already have lost its exorbitant privilege to finance itself cheaply in tough times.

The level of the dollar, on the other hand, will be determined primarily by global investors’ appetite for holding US assets, and US investors’ appetite for owing assets from the rest of the world. This, in turn, will be driven by their respective assessments of the risk-adjusted returns they can expect for both types of assets. For now, the world has turned less optimistic about the US medium-term growth prospects and less pessimistic about those of Europe and other regions, owing to the recent thrust of policies pursued on both sides.

If these policies persist, notably high tariffs and high policy uncertainty in the US, doubling down on trade and long-overdue structural reforms in the EU and around the world, then we may be only at the beginning of a vast, multi-year portfolio rebalancing process that will drag down the value of the dollar. But that is a big if, and the US economy retains formidable advantages over its would-be competitors, notably its scale, capacity to innovate and leadership in all advanced technologies that are essential to raise productivity.

All in all, rumors of the dollar’s death appear to have been greatly exaggerated. But recent US policies have definitely opened up space for its dominance to ebb. How that space is filled is up to the rest of the world.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.