What to watch for at the 2025 China Two Sessions

Chinese policymakers are expected to maintain last year's growth target to signal confidence in growth stabilisation, and we expect a greater focus on boosting domestic demand this year.

Two Sessions to set this year’s key economic targets

China’s annual Two Sessions kicks off next week in Beijing, with the Chinese People's Political Consultative Conference (CPPCC) set to open on 4 March and the National People's Congress (NPC) set to open on 5 March. These meetings will take place over a week and will lay out China’s key policy priorities for the year.

The main market focus will be the government work report delivered by Premier Li Qiang at the start of the NPC on 5 March, which will lay out China’s main quantitative targets for economic growth.

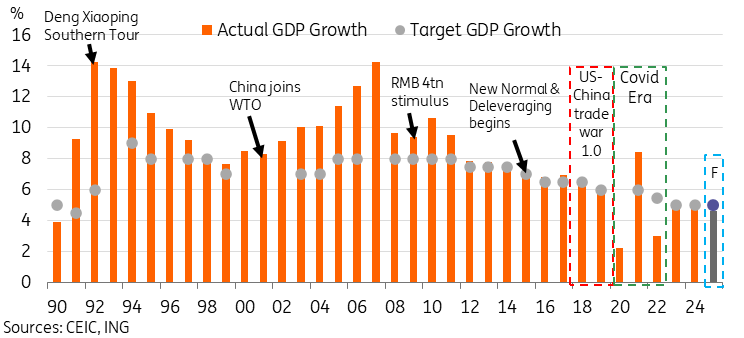

The headline will undoubtedly be China’s GDP growth target, which we expect to remain unchanged at “around 5%” again this year. We believe this target will signal confidence that China can maintain steady growth despite heightened external uncertainties.

Policymakers tend to attach high importance to accomplishing this goal, and since targets were started in 1990, growth has only fallen notably short of target twice, in 1990 and 2022. The strength of fiscal and monetary support tends to align with the year’s growth target, so a stronger target implies we will also see stronger stimulus measures and vice versa.

Provinces have already published their growth targets for the year, and most growth targets have been set between 5-6% growth, with stable or slightly lower targets compared to last year. Overall, the sum of the parts should still be enough for China to set the “around 5%” target.

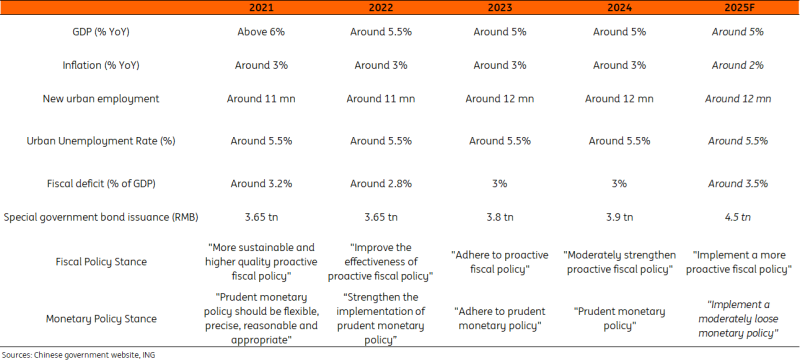

Additionally, we expect the inflation target will be lowered. This shouldn’t have a significant impact on actual policy – historically the inflation target was more relevant when inflation tended to run too hot. With that said, deflationary pressure has led to a significant undershoot of CPI inflation for the last few years, and bringing the 3% target to a more internationally aligned 2% level makes sense.

China rarely fails to achieve its growth target after it is set

A more supportive policy stance is likely to be signalled

The government work report will also feature sections on the year's fiscal and monetary policy direction. We are expecting more supportive language for both.

In terms of fiscal policy, the general term “proactive fiscal policy” has been in place for recent years, though the language around that term tends to change every year. We are expecting a generally positive tone on fiscal policy. We may see a higher fiscal deficit target and local government bond issuance target to signal a stronger fiscal policy push this year.

In terms of monetary policy, we expect a notable shift this year, moving from the “prudent monetary policy” descriptor to “moderately loose monetary policy” for the first major shift since 2011. This change will likely entail further room for rate and RRR cuts this year – we are currently forecasting 30bp of cuts to the 7-day reverse repo rate, and 100bp of cuts to the RRR this year, with the first cut potentially coming as early as March.

Two sessions economic targets

Watch the domestic demand theme closely this year

Last year, China’s ability to complete the growth target was in large part due to stronger-than-expected external demand and the spillover impact on manufacturing, while weak private sector and household confidence were significant headwinds to domestic demand.

This year, the external demand picture looks likely to soften amid rising trade protectionism. As such, if China is to maintain steady growth this year, domestic demand needs to pick up the slack.

In last year’s Two Sessions, expanding domestic demand was the third objective listed in the “2024 Government Work Tasks” section, behind promoting “new quality productive factors” and boosting science and innovation. We expect that expanding domestic demand could move to become the first objective laid out this year, highlighting its greater importance this year.

This year’s policies to support domestic demand are likely to prominently feature the expanded trade-in policy as well as equipment renewal subsidies. The government report will be worth combing over carefully to see if other newer directions to support domestic demand are highlighted.

USD/CNY: Don’t expect changes to the currency stability objective

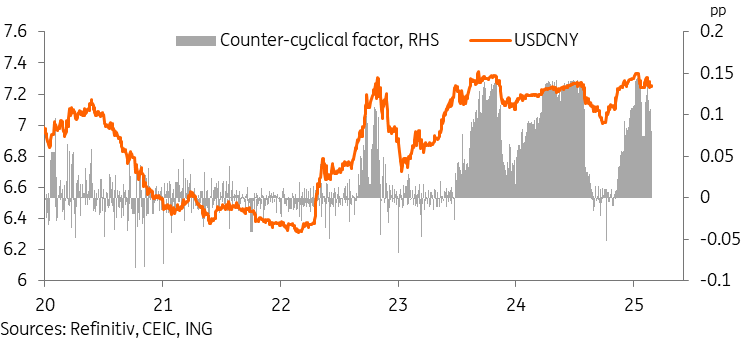

While the renminbi is not typically a major focus of the government work report, there has always been a sentence within the monetary policy section on the stance toward the exchange rate. The language of “maintaining RMB stability at a reasonable level” has been in place for much of the past decade, with the occasional mention of further improving the exchange rate mechanism. We expect policymakers to keep this language in place at this year’s Two Sessions – any unexpected change to this language could naturally have big implications on our USDCNY outlook.

After Trump’s US election victory and the threats of elevated tariffs against China, many in the markets have debated whether or not China will intentionally devalue the CNY to help offset some of the impact of tariffs.

We have been arguing in the past few months that this fear is overblown, as intentional devaluation would likely be ineffective to offset the impact of tariffs as Trump could easily respond with further tariff hikes, which would also throw away all of the benefits gained from currency stability over the past few years, including limiting capital outflows, maintaining domestic purchasing power, and facilitating RMB internationalisation.

Our baseline forecast for USDCNY remains steady at 7.00-7.40 for the year. However, an increase to 7.50 could occur if tariffs are more damaging than anticipated or if monetary policy becomes unexpectedly hawkish. Despite this, we do not foresee China intentionally devaluing its currency.

PBoC efforts to maintain currency stability will likely continue

Read the original analysis: What to watch for at the 2025 China two sessions

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.