Weekend Note and The Week Ahead: Covid-19, and the “cleanest dirty shirt” argument

During a week when the coronavirus threatened to become a pandemic that hammers global growth.With reportedly 6 % of the world population under quarantine, and probably more as China continues to adjust the reporting goal posts. Yet the US market continues to whistle while walking through the graveyard with the S&P 500 Index advancing four out of five days, posting three records along the way. Investors took solace in robust economic data, better-than-expected earnings reports, and the fact a quorum of the global central banks have the markets back, which we will highlight in the Asia Week Ahead section.

A question that's cropping up a lot right now is: Why are equities up and bonds up too? The S&P 500, the Nasdaq, and the Dow Jones Industrial Average are all trading around record highs while the 10-year US Treasuries yield is at 1.58%, from 1.9% at the start of the year.

The US Federal Reserve, in an attempt to avoid another meltdown in the repo market as seen in September 2019, overcooked things when it injected billions of dollars of cash into the system to push rates lower. This left banks with sufficient money, which is now being used to buy bonds and equities. Particularly growth stocks which have only been able to gain "because" Treasury yields are so low. And while growth and defensive stocks have been in favor, the S&P500 isn't as risk-on as the index reading might appear. The leaderish is very defensive and narrow around growth names (US tech, basically), but that has not stopped the market frustrating the bears in the past and now feels no different. Depressing the returns available through the duration in risk-free government bonds creates incentives for investors to re-allocate capital to stocks even more so into the resilient US markets.

This is essentially the "cleanest dirty shirt" argument for owning US assets, which is particularly salient at the moment given the likely asymmetric growth impact of the coronavirus shock. At present, the growth impact of the virus remains expected to be more severe in China (and hence in Germany) than in the US. Which, in turn, is providing massive inflows into the US dollar.

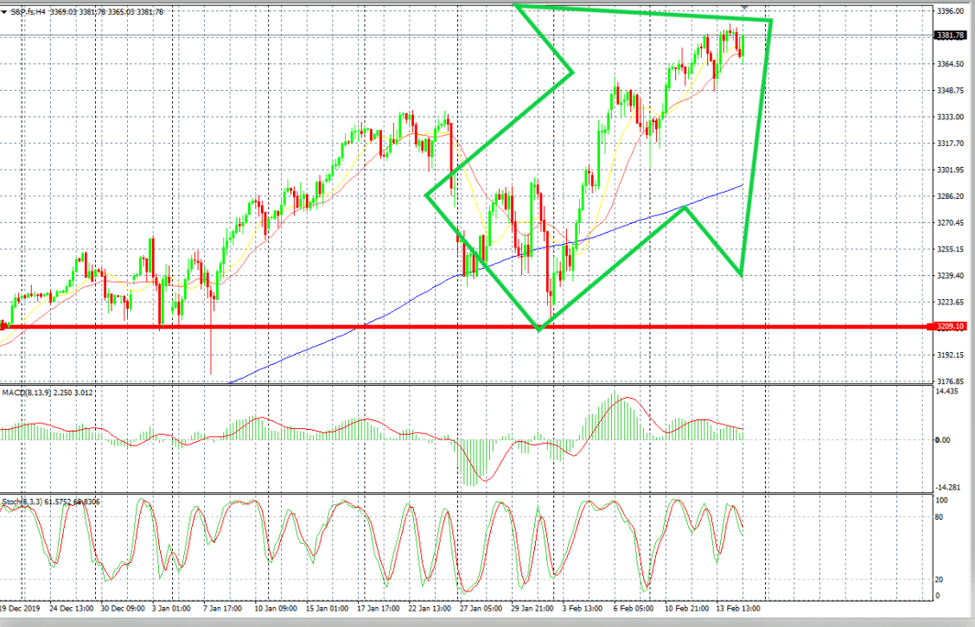

S&P 500 Chart

But despite the Covid-19 hanging like a dark cloud over Asia and will continue to be a market focal point well into March. So far, the US economy has been immune to the flu's nasty effects, and its thought that if there will be an impact, it will be both small and transitory. But the key to the bullish US storyline is that fundamentals are strong, and the economy continues to grow, which basically acts as the key MythBusters debunking the recessionary fear-mongering.

Coronavirus has probably caused investors to be underweight, or at least not get involved in this rally. But low rates are keeping the juice in the market led by defensives, and the harmful data that is expected is now so well-flagged that it has become irrelevant. And since stocks are as much a momentum story as anything else while getting juiced by the Fed repo remedy, investors might feel they have little choice but to get on board or risk getting left at the station.

Week Ahead

This week's economic dockets will provide a heavy dose of Fed speak with garnishing's that will provide insights into current-quarter housing and manufacturing activity. With respect to Fed communications, the minutes of the January 29 FOMC meeting (Wednesday) will be a focal point for traders—in particular, discussions around the Fed's policy review.

Last week, we saw a surge in the number of new Covid-19 cases in Hubei due to the adoption of new diagnostic methods; however, outside of the province, the number of new cases continued to trend lower. In response to adverse economic effects of the outbreak throughout the ASEAN region, policymakers are putting together fiscal and credit support, while mulling over further rate cuts. On the data front, Malaysia's Q4 growth surprised to the downside as exports deteriorate. Next week, economists are expecting no changes to Indonesia's policy rate, while Thailand's growth is likely to remain weak at mid-2% in Q4. Looking ahead, risks to growth and rates outlook in Q1 remain tilted to the downside amid the Covid-19 outbreak.

Key Asset Classes

Currency Markets

With the coronavirus hitting and uncertainty mounting, the US dollar indexes have steadily strengthened, but that is not the entire story. Advanced economy currencies' weakness is driving much of the dollar strength. Most of the indexes used to measure "the dollar" are really indexes that measure the Euro with a few other currencies in there for good measure. Meanwhile, emerging market currencies are holding up well.

The relatively indifferent Asia FX reaction to the Hubei news suggests that investors continue to look through the economic impact.

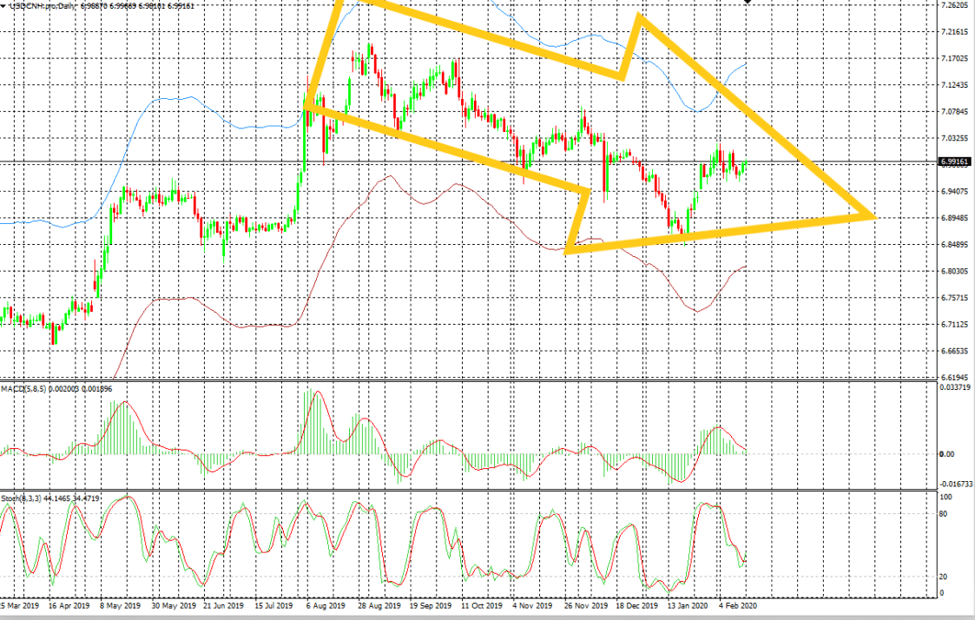

The USD has been enduringly bid, although FX vols are only slightly higher. But the downtrend in USDCNH since September 2019 remains intact, 12-month forward points narrowed further, and an ongoing sell-off in risk reversals over the past week suggests a more limited demand for protection against a CNH sell-off as the PBoC is offering up a convincing backstop. Although the CNH sold off in NY Friday, given the US holiday on Monday, US traders turned commensurably more defensive on Yuan than usual, given the long weekend effect amid concerns over the Covid-19 reporting uncertainties.

USDCNH Chart

Overall the somewhat muted reaction may be attributable to the fact that the number of new cases outside China has failed to rise. However, investors' sanguine response to the economic fallout from the coronavirus will be tested in the coming weeks, so at this stage of the game, Asia FX investors don't want to run to far ahead of the economic realities. Hence, they remain cautious about adding more currency risk before assessing the depth of the economic fallout.

Perhaps a bit of this phenomenon along with the US long weekend effect

There are three main channels for this fallout.

One is the tourism channel. The impact is easily quantifiable, and the initial reaction of the markets has been most punitive for the more vulnerable economies on this metric – THB and SGD. What's harder to assess is the damage via the other two channels – supply chains and demand contraction, and for this, we need to see the empirical data. For that impulse, the release of Korea 20-day exports (February 21) is essential.

G-10 All the focus is on the Euro

Interest rate level differentials between the US and NIRP( EURO) economies remain quite broad in a historical context, and these wide differentials continue to attract capital flows into US assets, as is evident from persistent strength in the general dollar.

Investors also, to a large degree, continue to 'look through' the economic impact of coronavirus, ostensibly driving EUR weakness via long Asia FX and EM carry positions.

But if the recent EURUSD weakness reflects downside risks to global growth from China, rather than a hunt for yield carry, then the EM currencies which have held up well so far could weaken abruptly if China data comes out worse than expected. For EURUSD itself, global growth concerns could overwhelm any short-covering of long EM carry positions. That, in turn, could drive further weakness in EURUSD and return EURUSD-ADXY correlations to pre-summer 2019 levels.

Again, it's the "lose-lose" situation for the Euro that we suggested at the start of the year.

But does the Euro have legs to run?

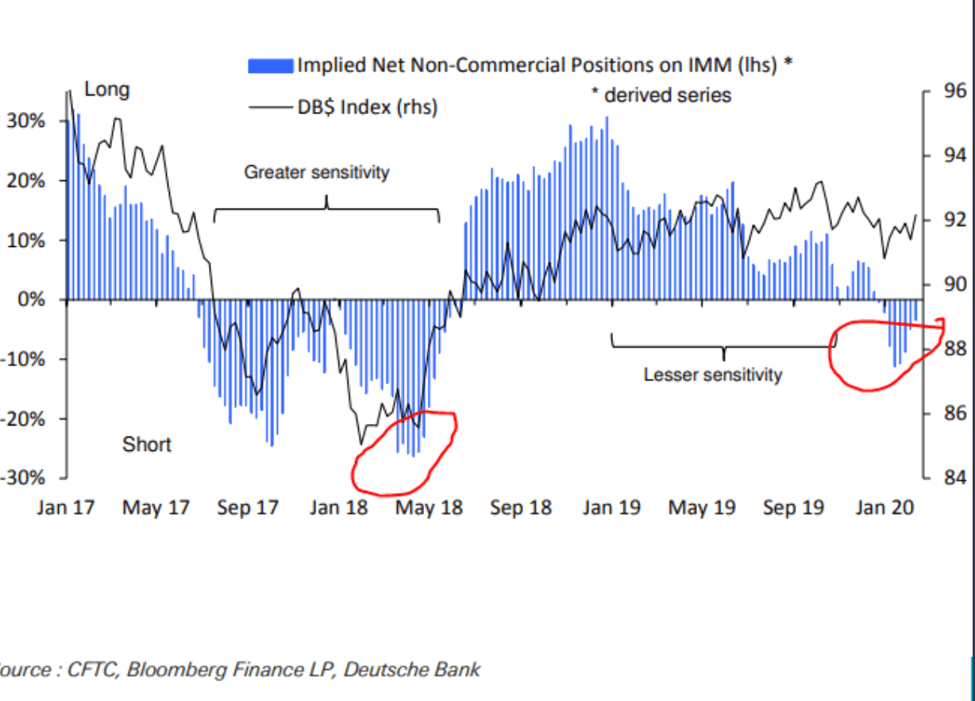

The market got paid out of a fair bit of puts in the past few sessions. The risk reversals are going better bid for puts.1month 25-delta risk reversal is 0.25 vol bid for puts - it was 0.5 bid for calls a week ago. Positions are not stretched vs. 2015 peak of 84% open interest.

Gold

In the battle of the weekend, hedges vs. Covid-19 data surprise, secondary transmission clusters, or if you think China reporting transparency is questionable. The one clear winner was gold as the yellow metal continues to shrug off an enduringly influential USD buoyed by ongoing investor concerns over COVID-19.

It appears that investors are continuing to seek gold as a quality asset or hedge against the economic impact of the outbreak. And with US markets closed on Monday in observance of Presidents Day, this will leave Asian and European markets, which appear more sensitive to COVID-19, in control of the gold market. So with little chance to buy a dip on Friday after a consensus headline retail sales print. US Covid-19 hedgers we forced to chase gold higher due to the US long weekend effect, which was probably commensurately more bullish for gold than would otherwise be the case.

But putting a broader spin on gold's appeal beyond the current Covid-19 narrative, which will likely be a transitory event and might have a muted impact on central bank policy outside of Asia, I focus on Friday's US retail sales data.

Listening to commentary surrounding the consumer, it always seems to be on the edge of doomsday even beyond the armageddon quacks on twitter. So, with investors very hypersensitive to any measurable negative US consumer data point regardless of how small, it's likely going to drive an overreaction of sorts.

The three-month moving average of US core retail sales has been flat for two months now (0%), and negative for the two months before that. This suggests a trend loss in core consumption is a cause for concern. And while Cherry-picked data points can back-up nearly any position, but the 3-month moving average is a solid detail and is the primary driver of the US Treasury rally on Friday, and likely the catalyst behind the demand gold into the weekend, after all, virus transmission outside of Hubei is falling?

The Fed and Gold

So far, the Fed has been sticking to its consumer-spending-driven growth narrative, so last week's soft retail control figure introduces some doubt into that picture. While it is early in the quarter and retail sales are often revised, the next retail sales release on March 17 takes on added significance as it has the potential to impact the Fed's current policy narrative.

No physical demand

While gold appears to be stuck in no man's land for now mired in the $1560-1590 range, with trading volumes somewhat depressed since the beginning of the year, but clearly, gold is still very much on everyone's tracking systems.

However, given the expanse of the coronavirus in China, gold physical demand is likely to suffer while other regional gold hubs like Hong Kong, Singapore, and Bangkok, whose economies have been ravaged by the tourist impact, physical demand is also likely to hurt. So the current bullish impulse could be thwarted by the lack of physical demand.

But a Fed Policy review screams buy gold.

January 29 FOMC meeting minutes (Wednesday) will be a focal point for gold traders —in particular, discussions around the Fed's policy review. As Chair Powell noted in his post-meeting press conference, the FOMC unanimously agreed that the current stance of policy is appropriate as long as the data are broadly in line with their outlook. However, when queried about average inflation targeting, Powell suggested that under a different framework, it may lead to a different approach to policy.

Interest rate level differentials between the US and NIRP( EURO) economies remain quite extensive in a historical context, and these wide differentials continue to attract capital flows into US assets, as is evident from persistent strength in the broad dollar. But gold institutional traders know the stronger USD is a problem for the FED who may unintentionally walk onto steadily thinner ice. Excessive dollar strength threatens to upend commodities and ultimately cause the Fed to miss inflation targets. Cutting rates will fiend of further dollar strength and will make target inflation more achievable.

In addition, given Chair Powell's discussion of the coronavirus at the press conference, there very well may be information in the minutes about the Board staff's insight into the economic impact of the virus.

The OIS market is currently pricing a 25% chance of a rate cut by the April FOMC Meeting and a 50% chance of a cut for the June meeting. With the coronavirus still a significant source of risk for the markets, but most investors believe market impact from the virus is still several months away and, for the most part leaving other factors unchanged. The issue at hand for the Fed is that inflation is below target, and if it goes unchecked, dollar strength will make this worse.

But with bond and gold markets singing from the same song sheet, even if the Fed delays cutting rates and it could exacerbate downside risk for inflation, so absent a dovish pivot by the Fed, the curve inversion could possibly intensify and will untimely drive gold prices higher. Thus in my view inversion is signaling mounting risks for lower inflation and inflation expectations, not imminent recession

But ultimately, it will take a more aggressive improvement in risk sentiment to chip away at long gold positioning. And with the Fed possibly moving to cut interest rates to defend their inflation targets, gold could be given bigger wings to fly.

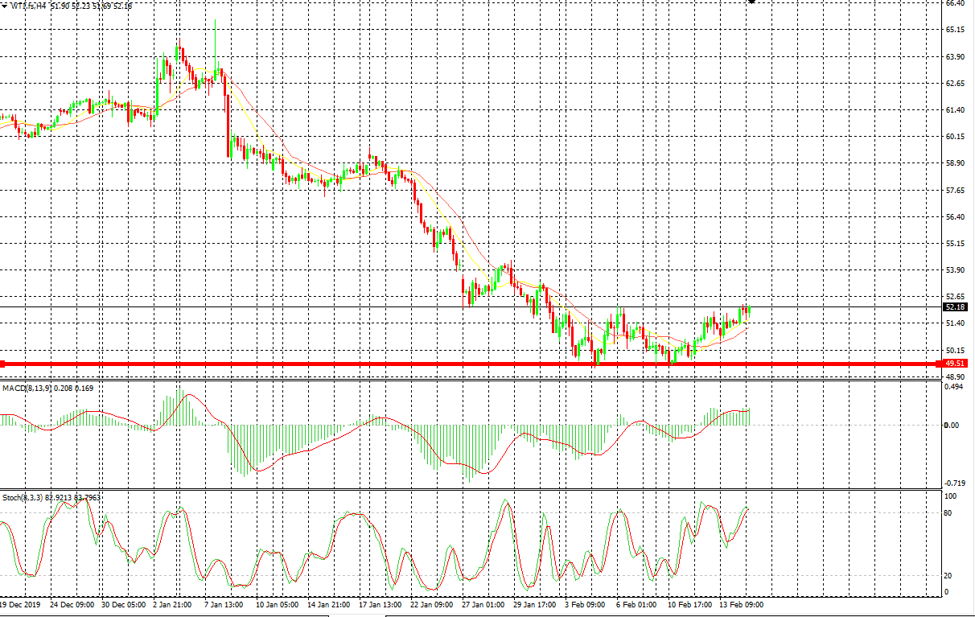

Oil Market: will they or won't they

Oil markets bounced around in relatively tight range on Friday as investors fretted about the Covid-19 demand devastation effect while receiving some encouragement that Saudi Arabia is convincing OPEC and friends to reschedule an emergency meeting. Of course, lip service is more comfortable to deliver than actually to get Russia to sit at the table. Still, if prices fall more profoundly below $ 50.00 WTI, it will probably trigger a meeting, so there remains a psychological floor in place which markets have been bouncing off.

OIl price line in the sand ??

Into weeks end prices remain supported by speculation that the spread of the coronavirus has slowed and as the market continues to focus on advancing towards OPEC+ reaction to the Covid-19 linked demand slowdown, which was confirmed again in the IEA's OMR that cut its projection for 2020 demand by 0.5Mbd with a cut to 1Q20 of 1.3Mbd.

But ultimately, it's all about the waiting game as traders sit on their hands hoping for Russia to play ball before taking on more oil risk.

However, OPEC+ is but a band-aid to stop the bleeding, not necessarily a bullish impulse unless they cut 1 million barrels of daily production out of the equation. Oil market needs China back online, which made for a good read of Bloomberg's Chinese Refiners Go on Buying Spree as Oil Too Cheap to Ignore Friday article but should not be confused with a recovery in China crude demand as run rates remain depressed. But it's much better to have Teapots buying rather than selling stockpiles.

Proposed ASEAN stimulus packages

In addition to probable rate cut to the MLR and LPR cuts in China, the Ministry of Finance advanced RMB848bn of the local government bond quota, while local governments provided various tax and fee relief measures to local companies.

In South Korea, Finance Minister Hong and BoK, Governor Lee held a joint meeting. Without giving details, they pledged emergency measures to minimize economic fallout from the Covid-19 outbreak,

Taiwan is seeking a special budget worth NTD60bn (USD2bn) to support profoundly affected sectors like F&B, tourism, transportation, and agriculture

The Thailand Convention and Exhibition Bureau (TCEB) plans to spend THB200m to support affected sectors, in partnership with the Thai Chamber of Commerce (TCC) and SET-listed companies - with more stimulus measures to follow.

Malaysia to announce a stimulus package early next month, to support growth, which is likely to include targeted spending for affected sectors, including tourism and manufacturing.

Singapore is likely to announce a series of stimulus measures in response to the Covid-19 outbreak, included in the 2020 budget due out on Tuesday.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.