Week ahead – US inflation data eyed amid Iran peace hopes

- Middle East headlines continue to dominate as hopes of deal grow.

- US CPI and retail sales data to fight for attention as Warsh takes office.

- UK Q1 GDP and BoJ meeting summary also on the agenda.

Markets cheer Trump’s peace push despite threats

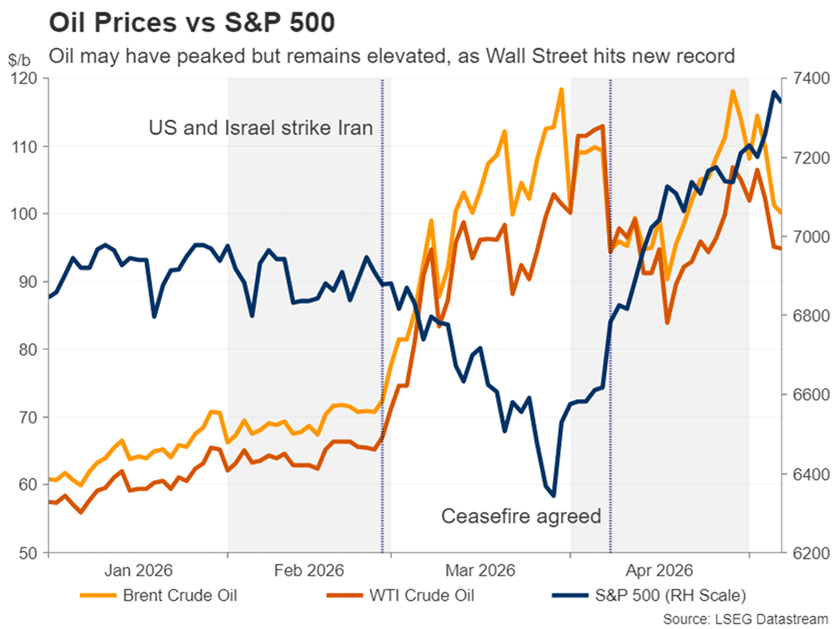

The late April surge in oil prices wasn’t met with the same risk-off reaction as at the onset of the Iran conflict, as the recharged AI rally eclipsed fears of a deepening energy crisis. Yet, the rise in inflation expectations was notable, and even as some of the worst fears have subsided, key metrics such as the US 10-year breakeven rate are above pre-war levels.

Investors are likely taking heart from the fact that inflation expectations globally remain some distance from the peaks seen immediately after Russia’s invasion of Ukraine. But there’s a danger they’re ignoring the real risk of the current energy crunch becoming the most severe in history. Crucially, the latest relief rally is founded mostly on hope rather than an actual deal between the US and Iran.

Although it’s accurate to say that President Trump’s rhetoric is more indicative of a desire to exit from the conflict than to inflame it, Tehran’s leadership structure has become more “fractured” in the President’s own words. Moreover, the Iranians are known to be tough negotiators, so even if the two sides can agree on a framework for a long-term deal that includes curbs on nuclear enrichment, the risk of re-escalation remains extremely high amid the battle over who controls the Strait of Hormuz and Israel’s repeated violations of its ceasefire with Hezbollah.

Even in the best-case scenario that the Hormuz Strait reopens soon, energy shortages could worsen before they get better, as it would likely take months for oil and gas flows from the Middle East to normalize. However, Iran negotiations are likely to take a backseat next week, as President Trump travels to China for a meeting with President Xi Jinping where trade will be top of the agenda.

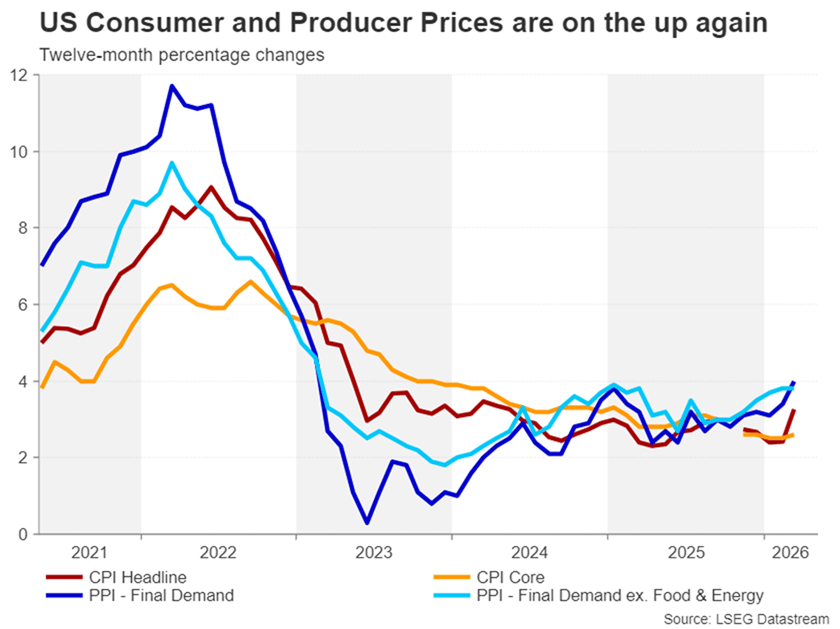

Will the US CPI report matter?

Nevertheless, investors have scaled back some of their rate hike bets for the major central banks in line with the pullback in oil prices, with expectations for the Federal Reserve once again switching from hikes to cuts. The fluid situation in the Middle East means that the market reaction to the upcoming releases out of the United States, namely Tuesday’s CPI report, will be determined by whether there is any progress in the peace talks, or if Trump has ordered fresh strikes on Iran.

A major flare-up would increase investors’ sensitivity to upside surprises in the inflation data, while positive negotiations would reduce it, as any pickup would be considered temporary.

Headline CPI jumped to 3.3% y/y in March and likely accelerated further in April. The Cleveland Fed’s Nowcast estimate is a rise to 3.6% y/y, while core CPI is seen staying unchanged at 2.6% y/y.

Producer prices for the same month are due the following day on Wednesday. The PPI report quite often tends to negate some of the effects of a CPI surprise if they’re contradictory. But if both sets of figures are hotter-than-expected, risk appetite is likely to be knocked back as Fed rate cut bets would take a hit, with next week’s busy schedule of Treasury auctions potentially exacerbating any spike in US yields.

Warsh confirmation awaited

Also guiding the Fed policy direction next week will be possible comments by Fed chair nominee Kevin Warsh, who looks set to be finally confirmed by the US Senate on Monday, just days before outgoing chair Jerome Powell’s term is set to expire on May 15.

Investors have largely welcomed Warsh’s nomination, as he’s likely to make the case for the need to cut rates further. But any explicit hints about the types of reforms he has in mind could spook markets.

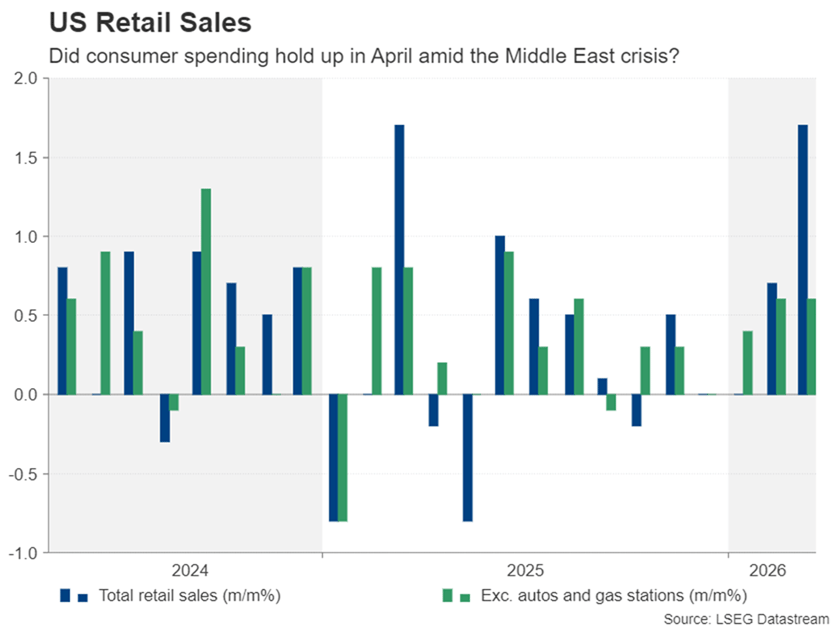

Thursday’s retail sales numbers for April will also be vital, amid some worries about whether US consumer spending will hold up against a backdrop of rising gasoline prices. Other data will include existing home sales on Monday, and the Empire State manufacturing index and industrial production on Friday.

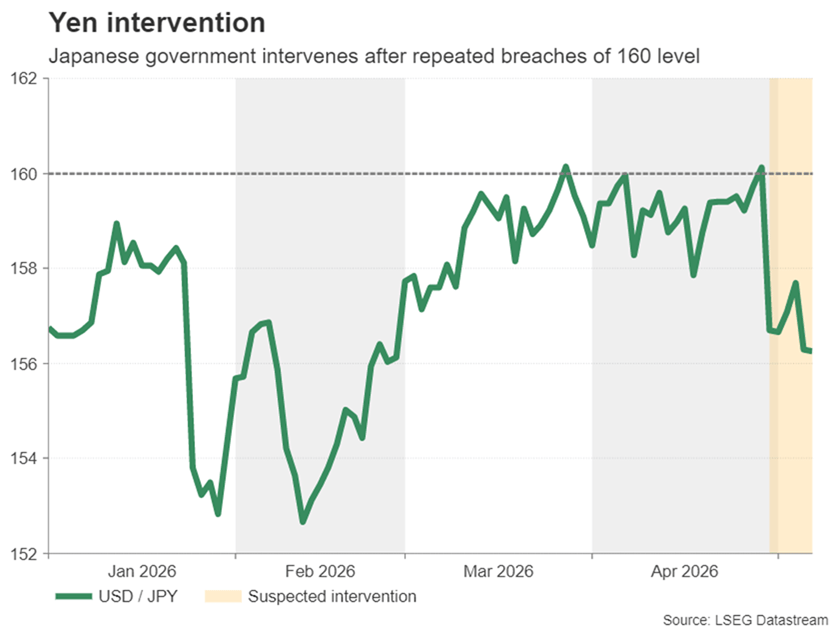

Dollar’s resilience tested by Yen intervention

The US dollar’s losses on the back of the optimism of an end to the Iran conflict have been relatively modest and would have been even less if it wasn’t for the intervention in the yen by Japan’s government. But despite Fed rate hike bets diminishing, a resumption of the dollar’s 2026 uptrend isn’t on the cards either, as Japanese authorities are suspected to have remained active in the FX market following the April 30 intervention.

The yen’s best prospect in the short term is to attempt a dash toward the 152-per dollar area, which twice acted as resistance earlier this year. Such a boost could come from the Bank of Japan’s Summary of Opinions of the April meeting due to be published on Tuesday.

There were three dissents at the meeting, as the hawkish voices grew louder. If the summary reveals that other board members could soon join the calls for an imminent rate hike, the yen could enjoy improved demand other than from central bank buying.

Pound bulls tread carefully

For the pound, whose own rebound against the dollar has been constrained by stagflation risks even as the Bank of England lays the ground for a summer rate increase, the geopolitical developments are being watched closely for the timing and scale of any tightening.

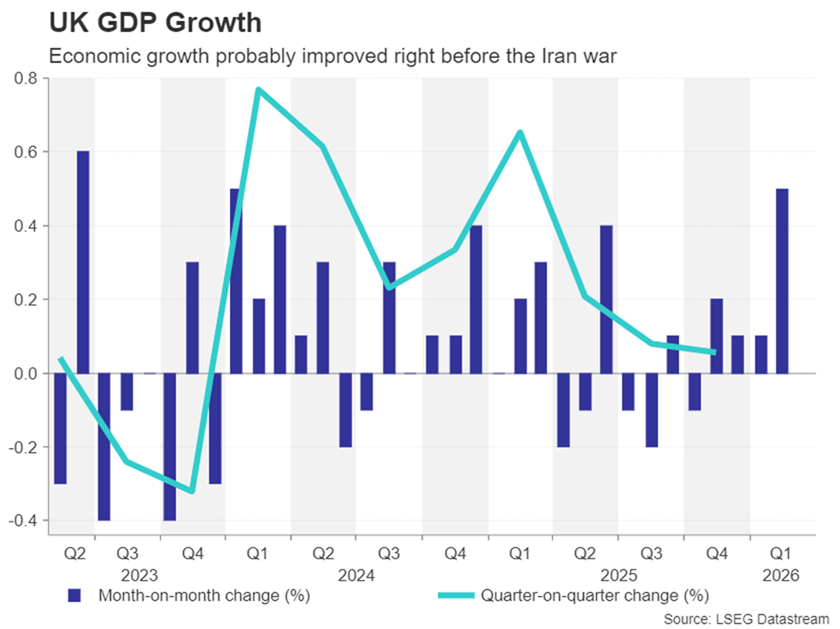

Next week’s initial estimate of Q1 GDP growth will probably play second fiddle to the Iran headlines, but will be important nonetheless, particularly the monthly print for March, to gauge what impact the start of the Iran war had on the British economy.

The data is due on Thursday, along with a breakdown of sectoral growth for the full quarter and March.

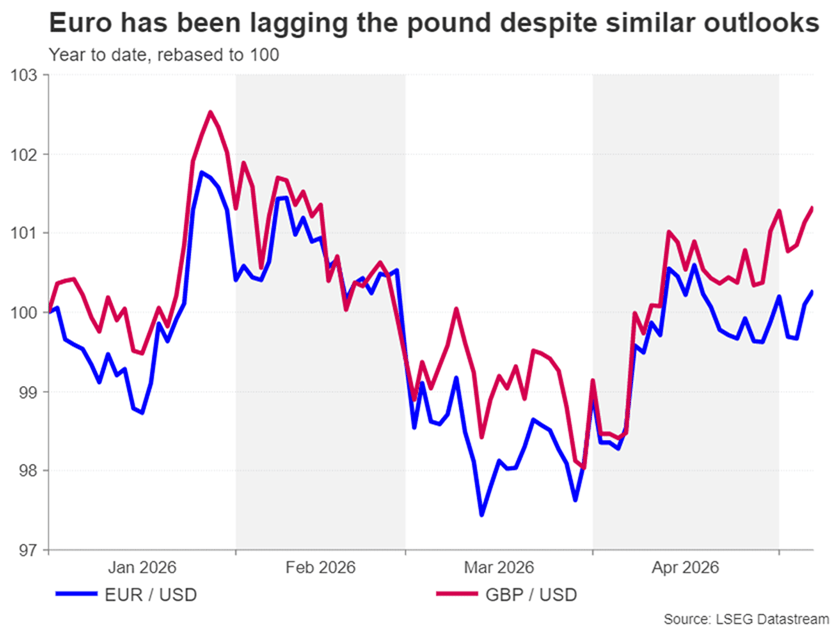

Kiwi shines while Euro lags

It’s a very similar story for the euro, whose recovery has been even slower than the pound’s and remains below its mid-April peak. The pricing out of an almost full 25-bps rate hike from year-end ECB expectations following the easing of tensions in the Middle East is probably behind the euro’s underperformance.

Quarterly employment figures and the second estimate of Q1 GDP growth, both on Wednesday, and Germany’s ZEW economic sentiment gauge on Tuesday are the highlights of the European agenda, though they’re unlikely to sway the euro much.

Elsewhere, China is expected to report a jump in both its CPI and PPI measures on Monday as higher energy prices took hold in April. On Wednesday, quarterly wage growth data will be watched in Australia for clues as on the likelihood of a fourth rate increase by the Reserve Bank of Australia. Meanwhile, in New Zealand, the RBNZ’s survey of quarterly inflation expectations could aid the New Zealand dollar’s impressive one-month-long rally against the greenback if they show an uptick.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.