Week ahead – US GDP and PCE data to mark a relatively light week

- Accelerating US PCE could weigh on Fed rate cut bets.

- Euro traders eye CPI data from Italy, France and Germany.

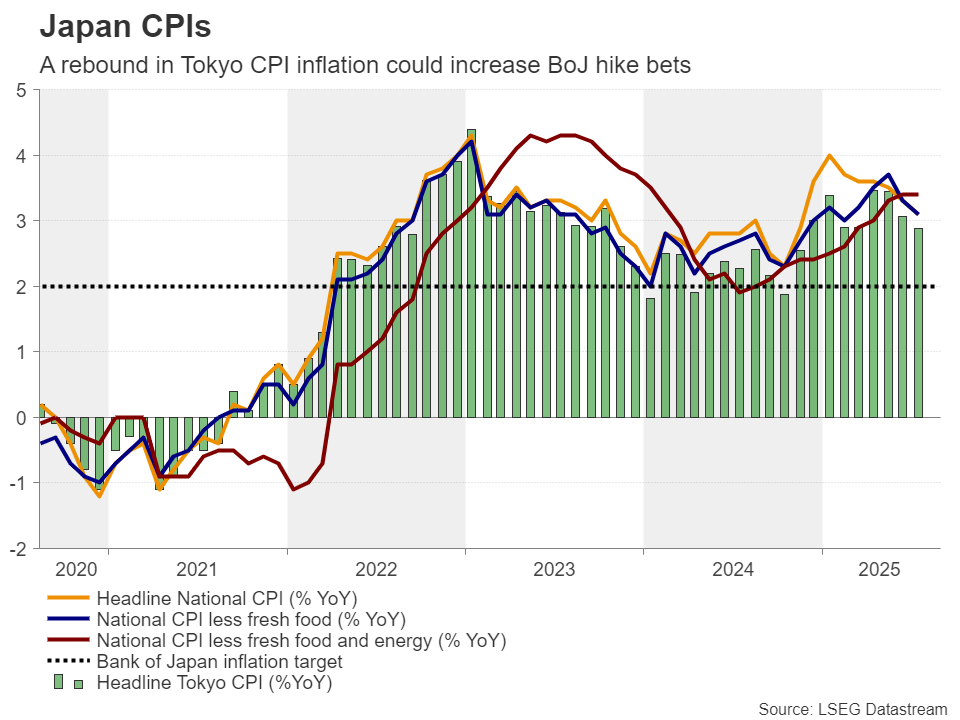

- Tokyo CPIs could impact chances of a BoJ hike by year-end.

- Wounded loonie seeks salvation in GDP numbers.

Dollar gains as investors scale back Fed cut bets

The US dollar gained ground this week, benefiting from investors scaling back their Fed rate cut bets.

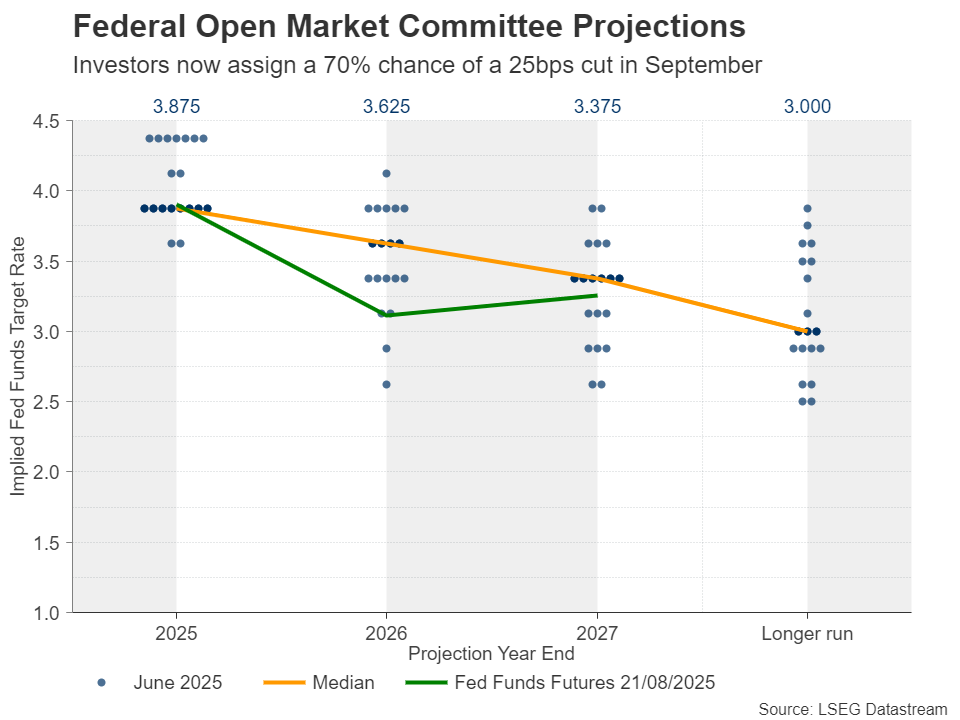

Following the weak NFP report for July, the disappointing ISM non-manufacturing PMI for the same month, and Trump’s reciprocal tariffs, speculation about faster rate cuts by the Fed heightened, perhaps as the aforementioned blend of developments sparked some recession fears. Investors were fully pricing in a September 25bps rate cut, another one thereafter, and went as far as assigning a 30% chance of a third one before the end of the year.

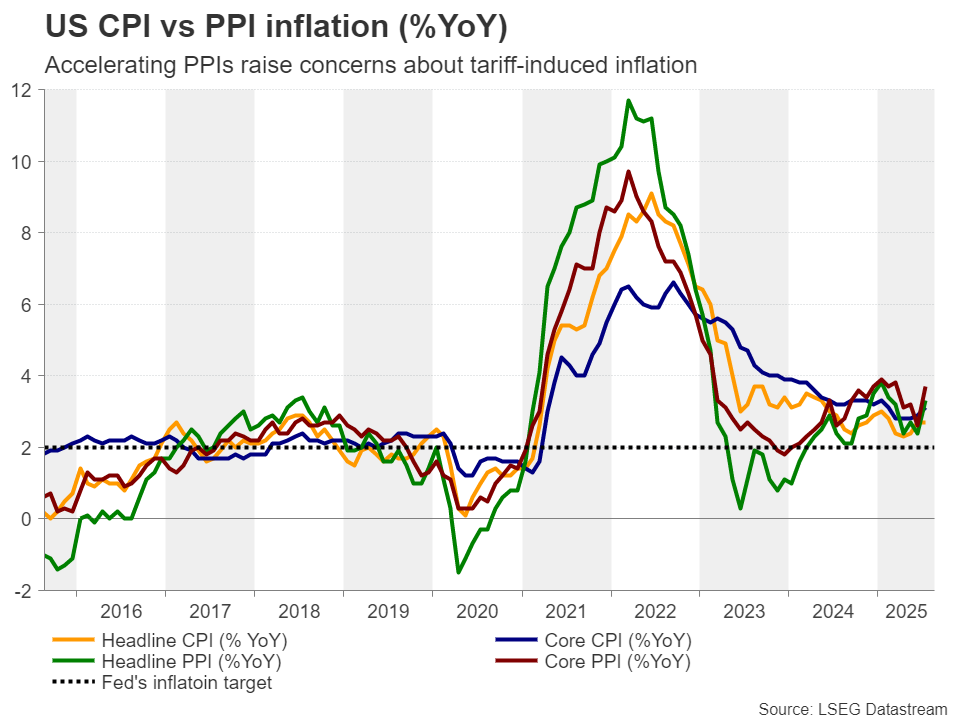

The CPI data for July corroborated that view, showing little evidence of tariff-induced inflation. However, producer prices accelerated sharply, painting a totally different picture and confirming Fed Chair Powell’s view that the impact of Trump’s tariffs on inflation will start appearing during the summer months. Combined with the strong preliminary S&P Global PMIs for August, this prompted investors to price out several basis points worth of rate cuts. They are now assigning a 70% chance of a September reduction.

After Powell’s speech, focus to turn on GDP and PCE data

The Fed Chief is scheduled to speak today at the Jackson Hole economic symposium, and it seems that the market is bracing for a hawkish outcome. Indeed, not only is the dollar gaining, but Wall Street is in pullback mode.

However, even if he sounds hawkish and does not pre-commit to any action beyond September, market participants may seek further validation from next week’s US data, which includes the second estimate of GDP for Q2 and the PCE inflation data for July, due out on Thursday and Friday, respectively.

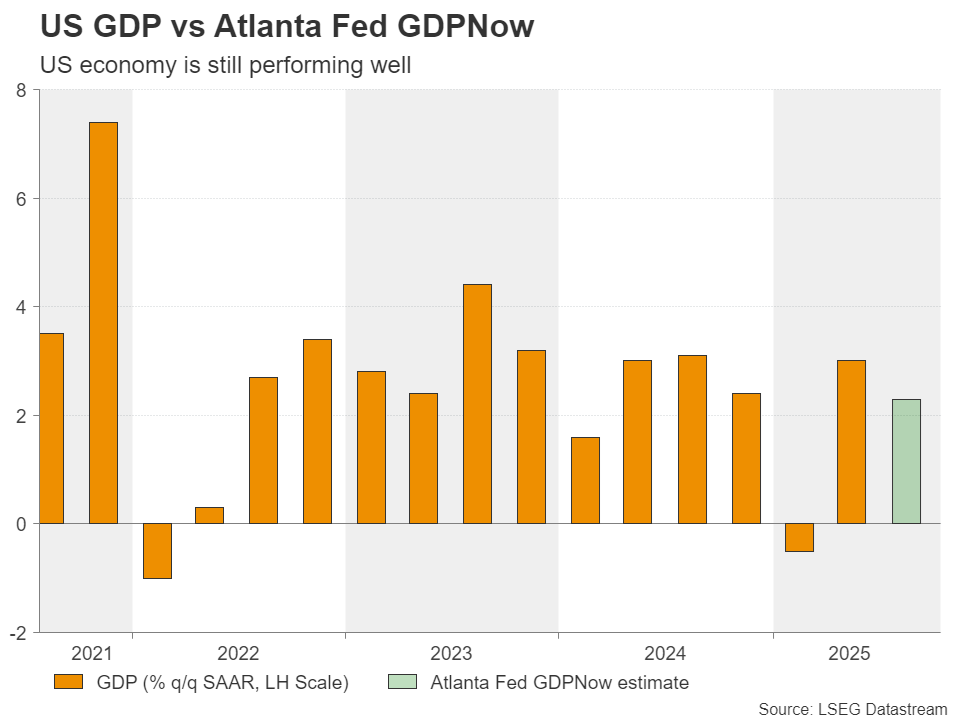

The first estimate of GDP came in at 3.0% q/q SAAR and expectations are for confirmation of that. Combined with the 2.3% forecast of the Atlanta Fed GDPNow model, it adds extra credence to the idea that the Fed should not rush into lowering interest rates, despite US President Trump’s pressure and repeated attacks on Chair Powell. That said, it is worth mentioning that the Atalanta Fed GDPNow estimate will be revised on Tuesday, before the GDP data are out.

As for the PCE numbers, the Fed’s favorite inflation metric is the core PCE index, whose correlation coefficient with the core CPI – taking into account the last 10 years – stands at 0.75. Therefore, given that the core CPI accelerated to 3.1% y/y from 2.9%, the risks for the core PCE index may be tilted to the upside. Therefore, more data suggesting sticky inflation could encourage more market participants to price out a second rate cut beyond September for this year.

This is likely to help the US dollar extend its recovery, while equities could drift lower as a slower pace of rate reductions could translate into lower present values for high-growth firms that are valued by discounting projected free cash flows.

Is the ECB done or are more rate cuts needed?

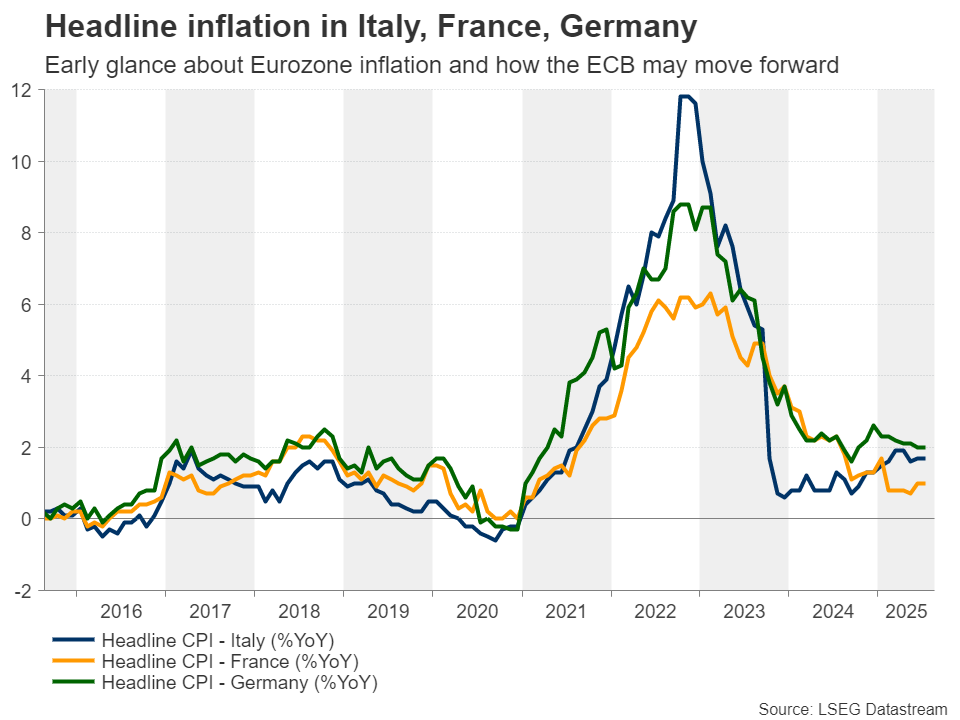

Turning to the Eurozone, the calendar includes the preliminary CPI numbers for August from Italy, France and Germany, set to be released on Friday. At its latest meeting, the ECB kept interest rates unchanged, while President Lagarde appeared more hawkish than expected at the press conference, which combined with the EU-US trade deal, raised speculation of a prolonged pause on interest rates.

Following the better-than-expected preliminary GDP data for Q2, the still-above-target core CPI rate, and the improving flash PMIs for August, investors are pricing in only 10bps worth of rate reductions by the end of the year. This translates into a 45% chance of another quarter-point cut by December. However, the market is not fully pricing in a 25bps cut even in 2026. Investors are just assigning a 72% chance that another cut might be delivered by June next year.

Having all that in mind, should preliminary inflation data from the Eurozone’s largest economies suggest that inflation is not further cooling, there may be no need for additional interest rate reductions should growth-related data continue to point to improvement. Euro traders may assign a smaller probability to another rate cut and the common currency may drift higher.

Tokyo CPIs enter the limelight as BoJ hike chances increase

Yen traders will also have to digest a bunch of Japanese data. During the Asian session on Friday, the Tokyo CPI figures for August will be published, alongside the nation’s unemployment rate, industrial production and retail sales for July.

This week, a former foreign minister who is rumoured to be among candidates for becoming a future prime minister, said that Japan must raise interest rates to strengthen the weak yen that has pushed up inflation and brought pain to households. This pushed the probability of another rate hike by the BoJ before year end higher, currently at 70%. Hence, accelerating Tokyo CPIs could take that probability higher and encourage investors to drive the yen higher, especially if the accompanying data also comes on the bright side.

Soft Canadian GDP to increase likelihood of BoC cut

Canada’s GDP for Q2 is also due to be released as the same time with the US core PCE numbers. The loonie was hurt earlier this week as the softness in Canada’s CPI data bolstered the case for further rate cuts by the BoC. Investors are currently assigning a 33% chance of a quarter-point reduction at the Bank’s upcoming gathering on September 17, with that probability rising to 90% in December. A soft GDP print may solidify the case of another reduction before year-end, thereby allowing some further loonie selling.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.