Week ahead – US election draws all eyes, Fed, RBA and BoE meet [Video]

-

Traders lock gaze on Tuesday’s US election.

-

Trump and Harris battle neck and neck in final stretch.

-

Fed to decide whether to cut interest rates.

-

RBA and BoE decisions are also on next week’s agenda.

![Week ahead – US election draws all eyes, Fed, RBA and BoE meet [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Events/US Elections/cabinas-de-votacion-gm145914665-5814659_XtraLarge.jpg)

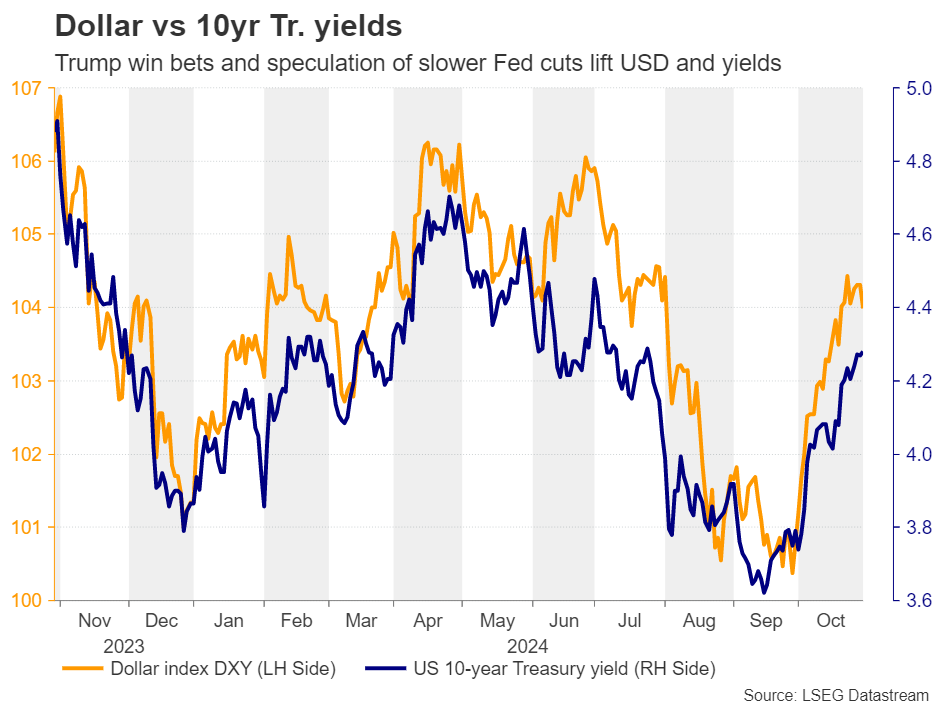

The US dollar flexed its muscles lately on the back of upbeat data suggesting that there is no need for the Fed to deliver another bold 50bps rate cut at the remaining gatherings of the year, but also due to increasing market bets that Donald Trump will return to the White House.

It’s US election time

The day when US citizens will decide whether this will be the case or not has come. While some Americans have already casted their vote, the official election day is on Tuesday, with candidates Donand Trump and Kamala Harris battling neck and neck for the Oval Office. Although Harris entered the race with a decent lead, the gap narrowed significantly over the past days, with the outcome hinging on battleground states.

Trump has pledged to cut taxes and impose import tariffs, especially on Chinese goods, policies that are seen as inflationary. Therefore, a Trump victory may raise speculation for even slower rate reductions by the Fed and thereby drive Treasury yields and the US dollar even higher.

The question is how the stock market will perform. Tax cuts and deregulation may be positive developments for Wall Street, but tariffs and slower rate cuts are not. Thus, even if stocks trade north just after a potential Trump win, a pullback may be on the cards in the not-too-distant future.

With the dollar and Wall Street gaining on increasing bets of a Trump win, a potential Harris victory may have the opposite market impact as her plans do not include massive tax cuts as Trump is promising. Having said that though, whether any policies will be implemented will depend on the composition of the Congress.

What will the Fed do after the election?

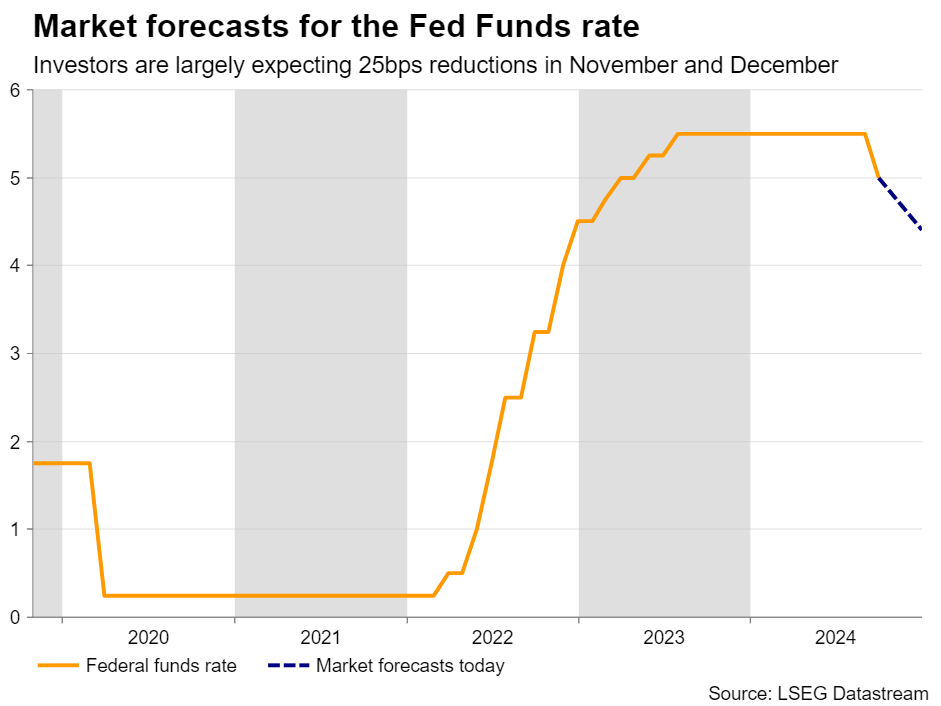

We may get a first idea on how the election outcome may affect the thinking within the Fed just two days later as on Thursday, the Committee announces its monetary policy decision. With the latest US data pointing to improvement and no need for a back-to-back bold rate cut, investors are now penciling in 25bps reductions at both this and the December gatherings.

That said, a 25bps reduction next week may not be a done deal as a hot NFP report later today and a Trump victory on Tuesday could convince more policymakers to agree with Atlanta Fed President Raphael Bostic who said a few weeks ago that he is totally comfortable with skipping a meeting. They could skip it next week or deliver the expected reduction in order not to catch investors off guard and hint at a December pause. After all, according to Fed funds futures, there is a 30% chance for a pause in December if a cut is delivered next week.

Taking into account the current market pricing, both cases argue for further gains in the US dollar. For the greenback to come under strong selling interest, Fed policymakers need to sound worrisome about the state of the US economy and signal that aggressive easing is needed for the months to come. Such a scenario seems unlikely though.

RBA and BoE also on next week’s agenda

The Fed gathering is not the only monetary policy decision on next week’s agenda. The ball will get rolling during the Asian session on Tuesday morning with the RBA, while on Thursday, ahead of the Fed, it will be the BoE’s turn to decide on interest rates.

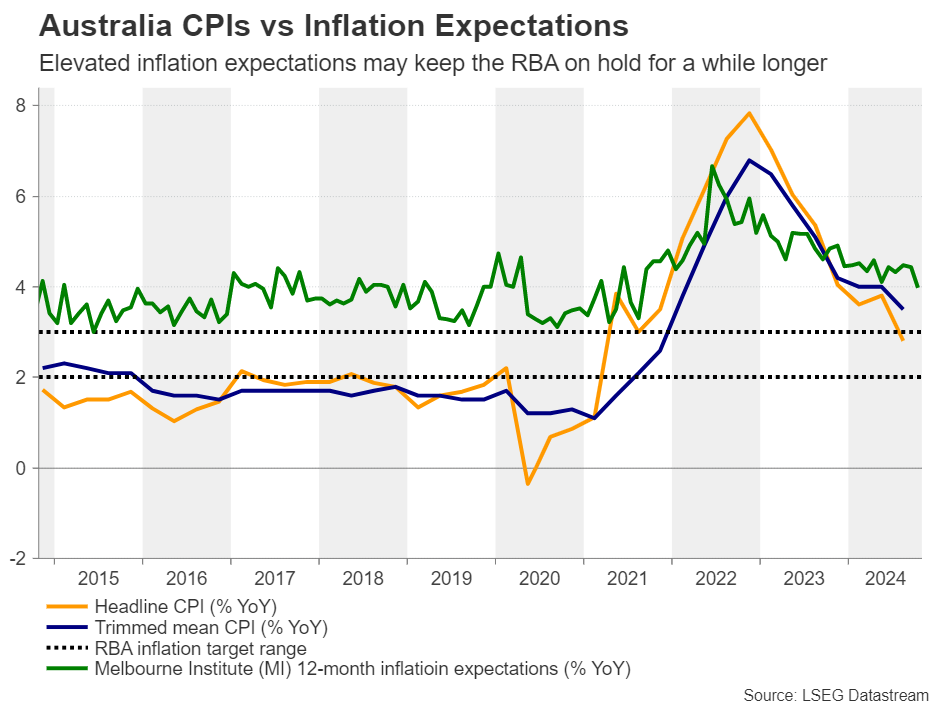

RBA could remain on hold for a while longer

At their latest decision in September, RBA officials kept interest rates untouched, noting that underlying inflation remains too high and that their projections show that it will be some time before it is sustainably within the Bank’s target range. The Board noted that they will continue to rely on data and that they will do whatever is necessary to achieve price stability.

With the Melbourne Institute (MI) still suggesting that inflation will hover around 4.0% in 12 months, it is hard to envision an RBA policy strategy like other major central banks, which have already begun slashing rates. Indeed, market participants are pencilling only a 20% chance of a 25bps reduction by the end of the year, while such a move is fully priced in for May.

So, investors will dig into the statement to see whether they are correct in predicting that this Bank will remain on hold for a while longer. If their views are confirmed, the aussie may instantly gain some ground, but its latest downtrend against the almighty US dollar is unlikely to be reversed, at least not until investors get convinced that China will proceed with meaningful measures to shore up its economy.

A BoE rate cut seems increasingly likely

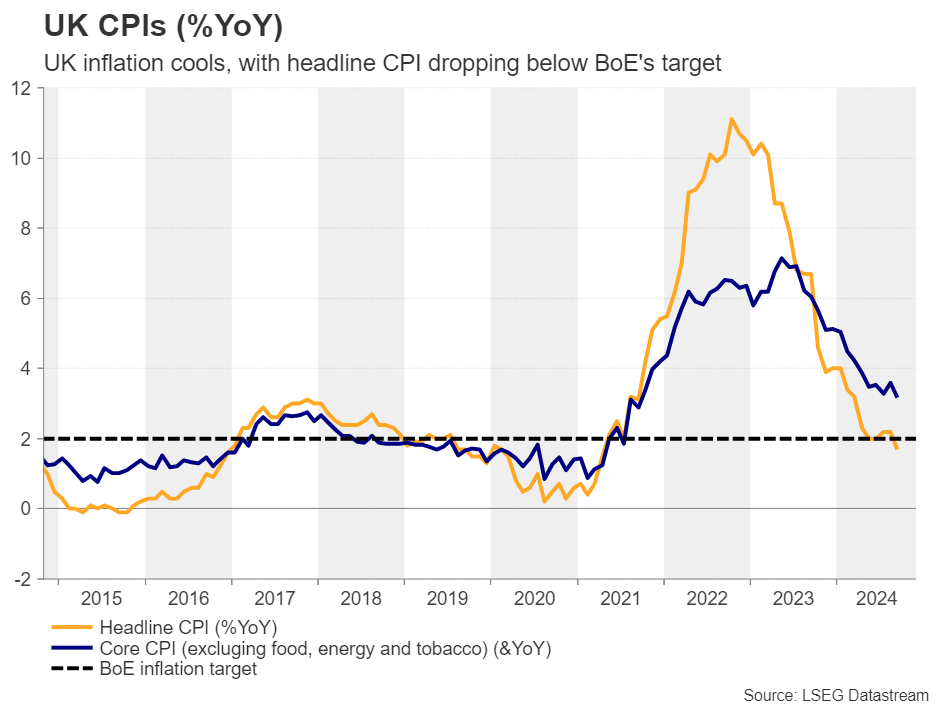

Passing the ball to the BoE, at their September meeting, policymakers of this Bank decided to keep interest rates unchanged at 5.0%, noting that they will be careful about future rate cuts.

Nonetheless, a few weeks after the decision, BoE Governor Bailey said that they may need to be more active with rate cuts if the data continued to suggest progress in inflation, and indeed, the September numbers revealed that the headline CPI slipped to 1.7% y/y from 2.2%, while the core rate dropped to 3.2% y/y from 3.6%.

This prompted market participants to assign a strong 80% probability for a 25bps reduction at next week’s gathering, but the chances of this Bank following with another quarter-point reduction in December rest at around 30%.

Therefore, a rate cut on its own is unlikely to shake the pound much. The spotlight may fall on the voting and policymakers’ communication. If the votes reveal that the decision was a close call and the statement points again to no rush in further reductions, the pound could gain ground. The opposite may be true if it is agreed that more rate cuts are needed in the months to come.

New Zealand and Canadian jobs data

Elsewhere, the New Zealand and Canadian employment reports are due to be released on Tuesday and Friday respectively. The RBNZ is expected to proceed with a back-to-back 50bps reduction on November 27, with investors assigning a decent 15% chance for a bigger 75bps cut. The BoC also cut rates by 50bps last week, but it is now seen slowing back to quarter-point reductions, with a 35% chance pointing to another double cut.

Having that in mind, weak jobs data from these nations could convince more market participants to bet on the bolder action for each of those two central banks.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.