Week ahead – Fed speakers, RBA decision, UK CPI and preliminary PMIs in focus

-

Strong dollar awaits Fed speakers and PMIs.

-

RBA to cut by 25bps, focus to fall on forward guidance.

-

Sticky UK inflation could mean only one more BoE rate cut.

-

Eurozone PMIs, Canada’s and Japan’s CPI numbers also on tap.

US-China deal boosts investors’ appetite

Risk sentiment improved significantly this week, while the dollar strengthened, after trade negotiations between the US and China ended with unexpectedly substantial progress. The world’s two biggest economies agreed to lower tariffs by 115% for 90 days, which means that during that three-month truce period, China will charge US goods with a 10% rate, while the US will tax its Chinese imports at 30%.

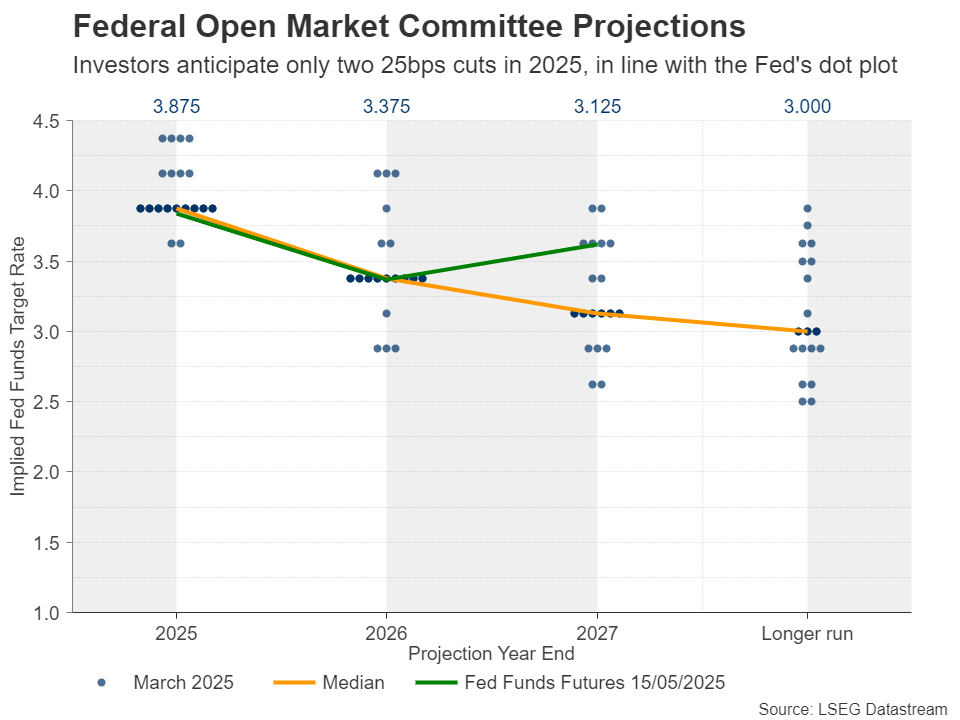

The better-than-expected accord significantly eased recession fears, with investors scaling back their Fed rate cut bets. From penciling in more than 100bps worth of reductions this year just after Trump’s ‘Liberation Day’, they are now expecting only 57, getting closer to the Fed’s latest ‘dot plot’, which pointed to 50bps worth of rate cuts by December.

Fed officials and US PMIs to shed light on Fed’s plans

Following this week’s CPI data, which revealed that underlying price pressures in the US remained sticky in April, next week, traders will monitor the preliminary PMIs for May on Thursday, but they may also pay attention to speeches by several Fed members as they may want to hear whether the Committee remains concerned about economic growth or whether they are more focused on the inflation outlook now the US has found some common ground with China.

Rising PMIs may suggest that sentiment among businesses has improved after the US-Sino deal, but investors may want to hear clear remarks about how the Fed is planning to move forward. Among the speakers will be New York Fed President John Williams, Atlanta Fed President Raphael Bostic, Dallas Fed President Lorie Logan, and San Francisco Fed President Mary Daly. If they remain concerned about the upside risks of inflation, the dollar could extend its gains as traders could price in even fewer rate cuts.

How the stock market may respond is not so crystal clear. We’ve seen equities gaining lately, even as market participants have been scaling back their rate cut expectations, mainly because the latest tariff-related developments have been easing anxiety regarding a recession. However, given that a recession is not so prominent now and a higher-for-longer rate narrative is based on concerns that inflation may prove to be hotter than expected, Wall Street may pull back should Fed officials highlight upside risks to inflation.

Will the RBA sound less dovish than expected

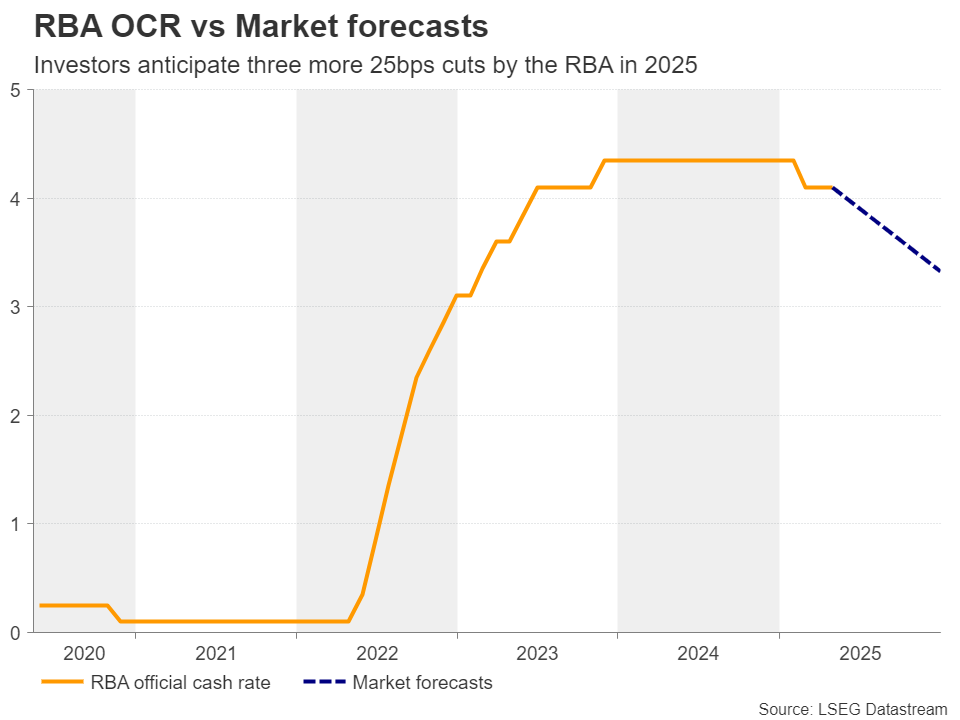

On Tuesday, the Reserve Bank of Australia (RBA) will hold its first monetary policy decision after Trump’s ‘Liberation Day’, as its prior meeting took place just the day before. Back then, the Bank kept interest rates unchanged, with Governor Bullock saying that no reduction was discussed as their top priority was inflation’s return to their target.

Since then, data showed that inflation was stickier than expected in Q1, but the overall uncertainty surrounding the global economic landscape due to Trump’s trade policies has led investors to pencil in around 80bps worth of reductions by the end of the year. For next week’s decision, a quarter-point reduction is nearly fully factored in.

Therefore, a rate cut on its own is unlikely to be a strong driving force for the aussie. Traders may direct their attention to clues and hints about how policymakers are planning to move forward. With underlying inflation metrics near the upper bound of the Bank’s 2-3% target range and taking into account the US-Sino trade deal, policymakers are unlikely to corroborate the ultra-dovish market consensus.

Yes, the Bank will likely keep the door to further reductions open – after all inflation is within the target range – but there is no data justifying 80bps worth of rate cuts by the end of the year. Thus, a less-dovish-than-expected message may allow the aussie to gain some more ground.

Ahead of the RBA decision, aussie traders may cast a glance at China’s data, due out on Monday. Industrial production, fixed asset investment and retail sales, all for April, will be released. That said, given that the data will refer to a period before the latest US-China trade deal, when tariffs were above 100%, investors may not take the numbers at face value and thus, any market impact may be limited and short-lived.

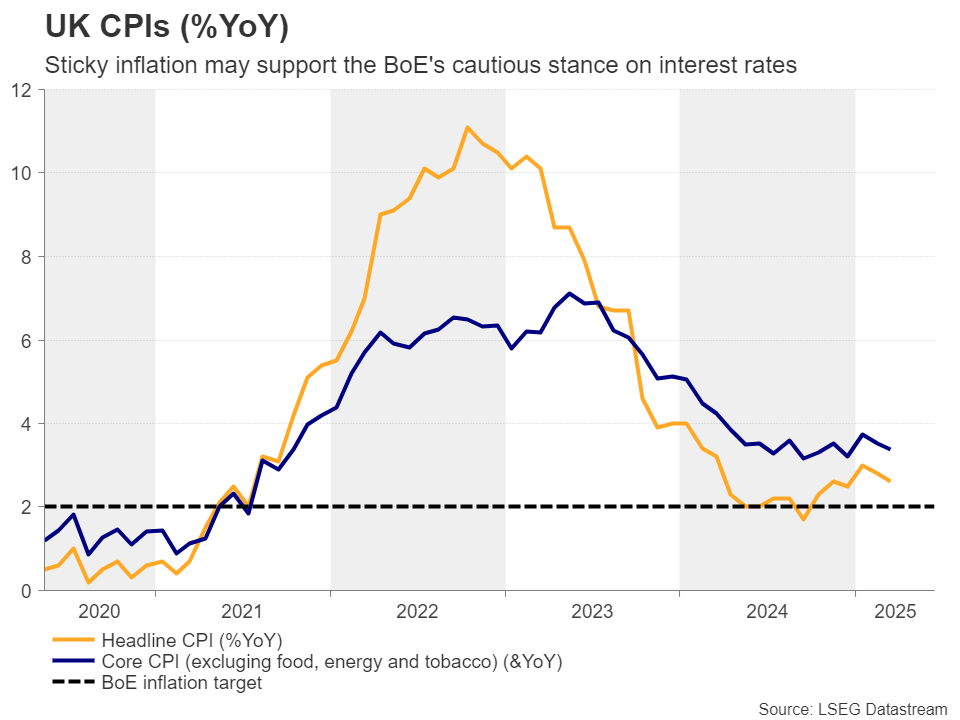

Hot UK CPI could mean only one more BoE cut

In the UK, the CPI data for April, the preliminary PMIs for May, and retail sales for April will come out on Wednesday, Thursday and Friday, respectively. On May 8, BoE officials decided to cut interest rates by 25bps, but the decision was far from unanimous. Five members supported the quarter-point cut, while two voted for a bigger 50bps decrease and another two for keeping rates steady.

The BoE said that tariffs could weigh on economic growth, but the outlook was still unclear. “That’s why we need to stick to a gradual and careful approach to further rate cuts,” Governor Andrew Bailey noted. Coming hot on the heels of the US-UK accord, the less-dovish-than expected outcome prompted investors to reduce the amount of rate cuts expected by the BoE this year from 75 to currently 45 basis points.

So, should the data point to sticky inflation, improving PMIs, and robust retail sales, investors may become more convinced that only a single quarter-point cut remains in the Bank’s chamber, which could propel the pound higher.

Eurozone PMIs, Canadian and Japanese CPI inflation

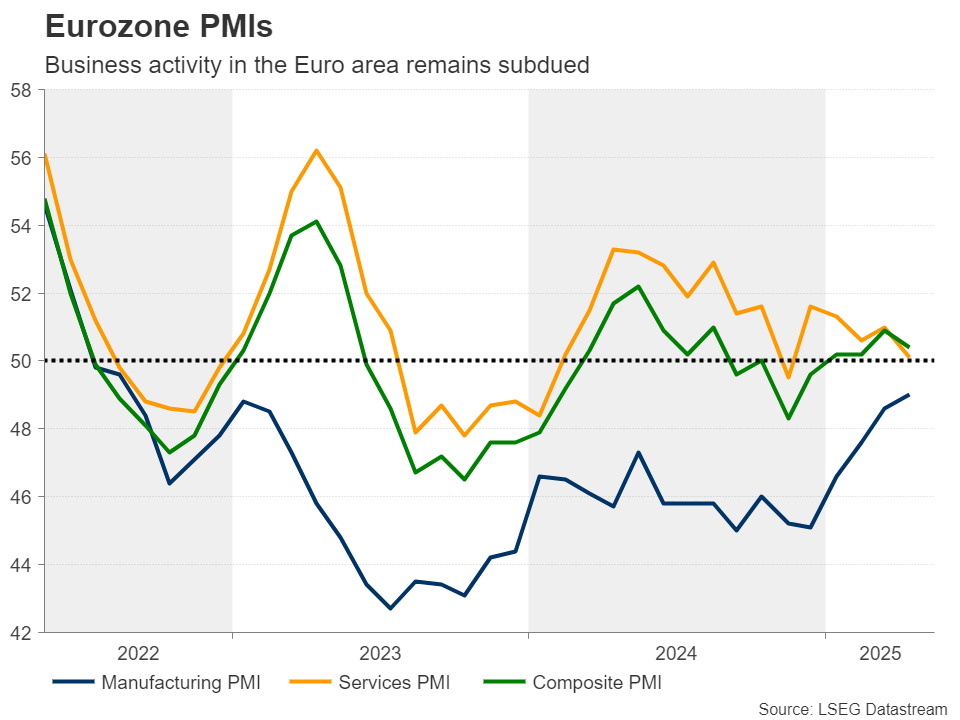

Besides the US and the UK preliminary PMI data, Thursday’s agenda includes the Eurozone numbers as well. After cutting interest rates by 25bps at its previous meeting and warning that economic growth will take a big hit from US tariffs, the ECB is widely anticipated to cut by another 25bps in June, but only one more reduction is priced in for the remainder of the year.

This may be due to the improving global trade environment, especially after the US-Sino deal, and due to recent remarks by ECB member Isabel Schnabel that interest rates should remain close to current levels. Therefore, a round of improving PMIs could corroborate Schnabel's view and add extra support to the euro.

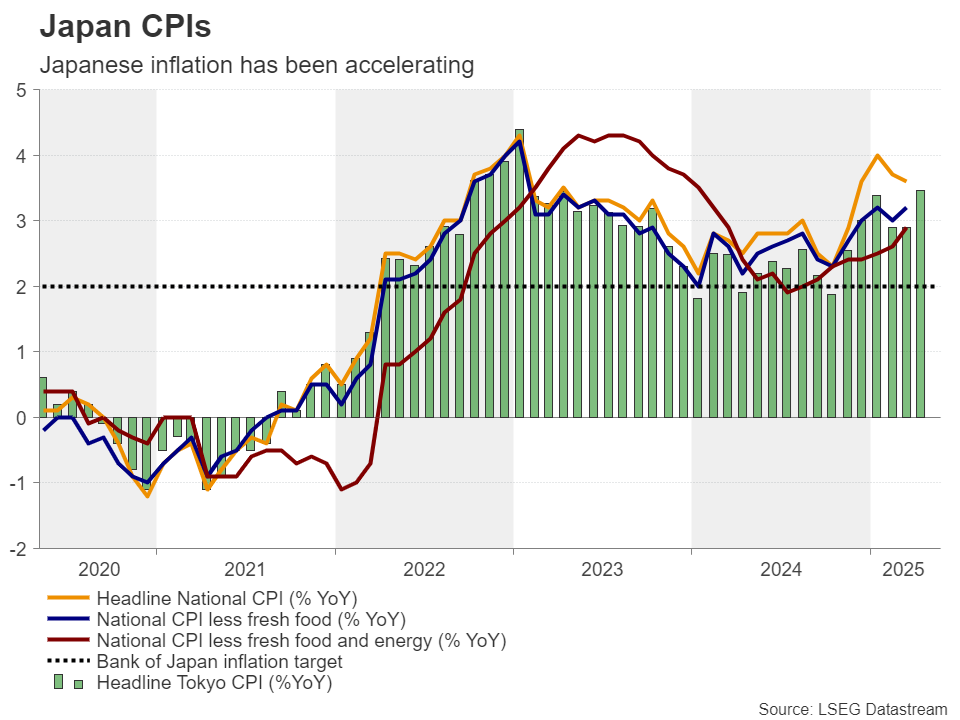

Canada and Japan also release their April CPI reports on Tuesday and Friday, respectively. The Bank of Canada remained on hold back in April, its first pause after seven consecutive cuts, adding that they remain ready to act if needed. With the jobs market losing around 33k jobs in March and failing to recover in April, the unemployment rate rose to 6.9% from 6.7%, prompting market participants to assign a 65% chance of another 25bps reduction at the June gathering. With the CPI already within the Bank’s 1-3% target range, further slowdown in consumer prices could solidify the case of a June rate cut and thereby weigh on the loonie.

As for the BoJ, its latest decision was less dovish than expected but still, investors are assigning a decent 70% chance of another quarter-point hike by the end of the year. Although the economy contracted in the first quarter, the Tokyo CPI figures for April accelerated strongly, suggesting that the National prints could move in a similar fashion and thereby add more credence to the case of another rate hike by the BoJ in 2025.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.