Week ahead – Fed, BoC, BoE and BoJ policy decisions enter the spotlight [Video]

-

Fed expected to cut rates, focus to fall on the new ‘dot plot’.

-

BoC seen cutting rates by 25bps due to weak economic data.

-

BoE to remain on hold, voting may shake the Pound.

-

Amid political uncertainty, the BoJ is expected to stand pat.

![Week ahead – Fed, BoC, BoE and BoJ policy decisions enter the spotlight [Video]](https://editorial.fxsstatic.com/images/i/Federal-Reserve-Building_2_XtraLarge.png)

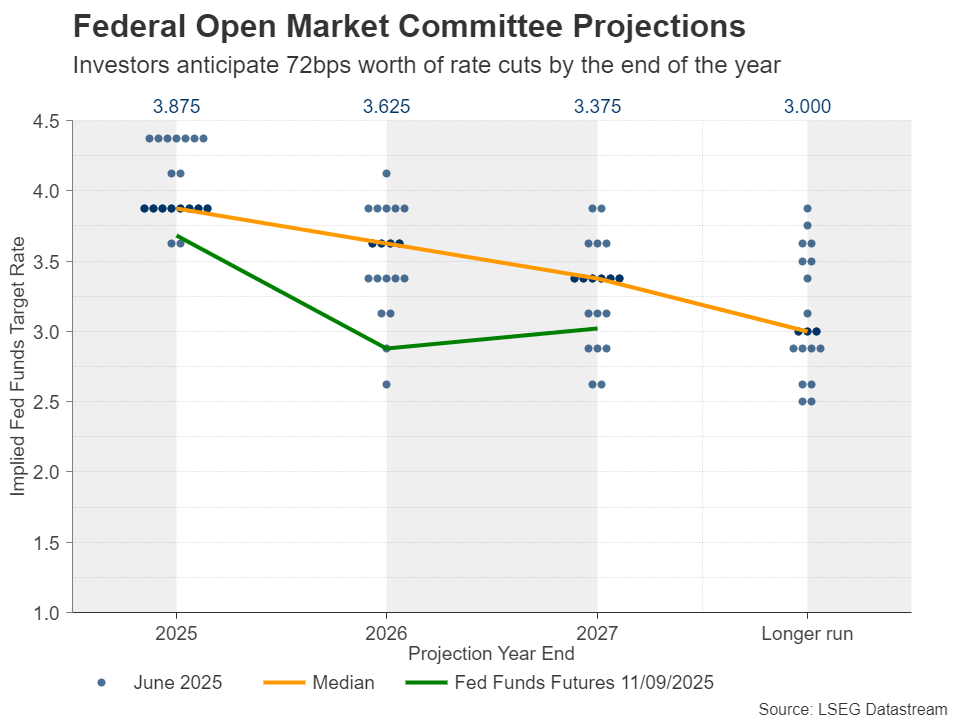

Investors see three rate cuts this year

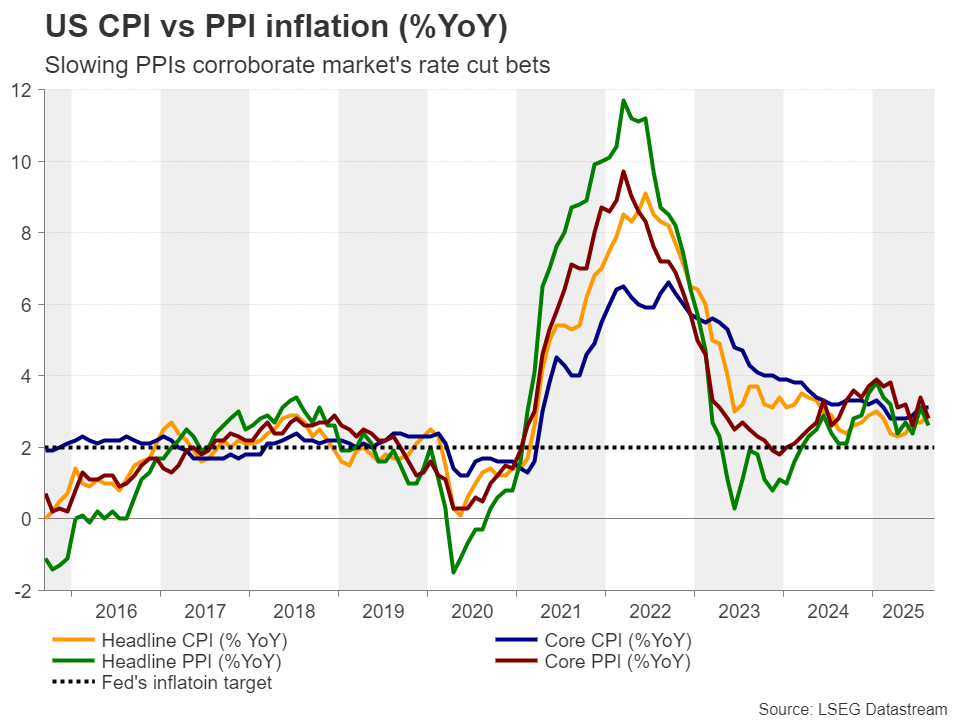

The US dollar entered this week on a soft footing as the disappointing jobs report for August prompted market participants to increase their rate cut bets. That said, it recovered ground on Tuesday and Wednesday, even after data revealed a marked slowdown in producer prices. It was sold again on Thursday due to weaker-than-expected initial jobless claims, despite slightly hotter than expected CPI numbers.

Investors remained convinced that more than two quarter-point rate cuts are warranted by the end of the year. According to Fed fund futures, around 72bps worth of reductions are baked into the cake, with the first 25bps cut expected to be delivered at Wednesday’s meeting. There is even a 7% chance of a double 50bps cut. However, a more likely scenario according to market pricing is for the Fed to cut by 25bps at each of the three remaining meetings.

Although the weakness in the labor market has increased speculation about aggressive Fed easing policy, the strong 3.0% growth estimate for Q3 according to the Atlanta Fed GDPNow model makes the Fed’s job more complicated than the market believes.

Will the Fed match the market’s dovishness?

A 25bps reduction on its own is unlikely to trigger market volatility. If this is the decision, market participants are likely to quickly turn their attention to Fed Chair Powell’s press conference and the updated macroeconomic projections, especially the new “dot plot”.

Back in June, the median dot for this year pointed to 50bps worth of additional reductions, but with seven members favouring keeping rates untouched. So, it will take a major shift for policymakers to even match the market’s dovish expectations. However, if indeed they appear convinced that more rate cuts are needed, the US dollar is likely to come under renewed selling pressure.

What may also attract special attention as we approach the end of 2025 is the median dot for 2026. In June, policymakers saw one additional reduction to the two projected for this year, which comes in huge contrast to the market’s view of another three. However, with US President Trump pushing for replacements within the Board of Governors, and the selection of regional Fed presidents scheduled for early next year, the 2026 projections may be subject to substantial revisions moving forward.

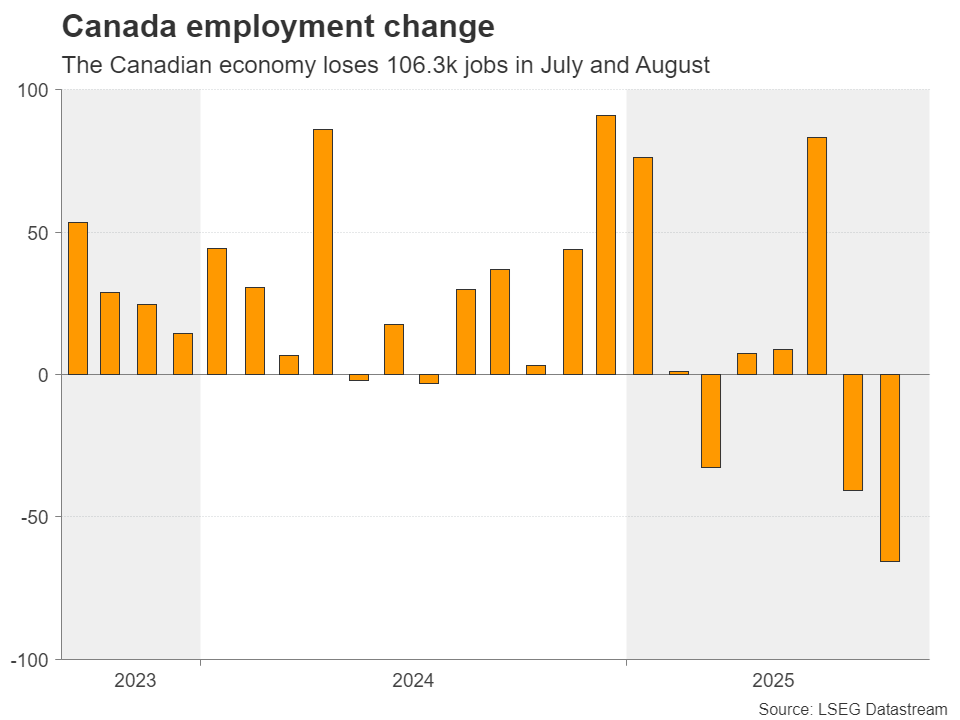

Economic weakness to prompt BoC to cut rates

Ahead of the Fed decision, the Bank of Canada will already have set rates. Back in July, the Bank kept interest rates unchanged at 2.75%, citing resilience in economy and adding that underlying inflation levels were around 2.5% when stripping out volatility and tax changes.

Since then, data revealed that the unemployment rate jumped to 7.1% from 6.9%, with the labor market losing a cumulative of 106.3k jobs in July and August together, while GDP for Q2 pointed to a 0.4% q/q contraction. The CPI rate for July dropped to 1.7% y/y from 1.9%, but the trimmed mean rate held steady unchanged at 3.0%. The August inflation report will be released on Tuesday, a day ahead of the rate decision.

Despite the stickiness in underlying inflation metrics, the economic weakness has led investors to turn dovish, assigning an 85% probability of a quarter-point reduction at this meeting and nearly fully pricing in another one by the end of the year.

If indeed the BoC cuts rates as expected and sounds more dovish than in July due to the deepening economic wounds, the Canadian dollar is likely to tumble, with dollar/loonie extending the decent recovery it started on September 1.

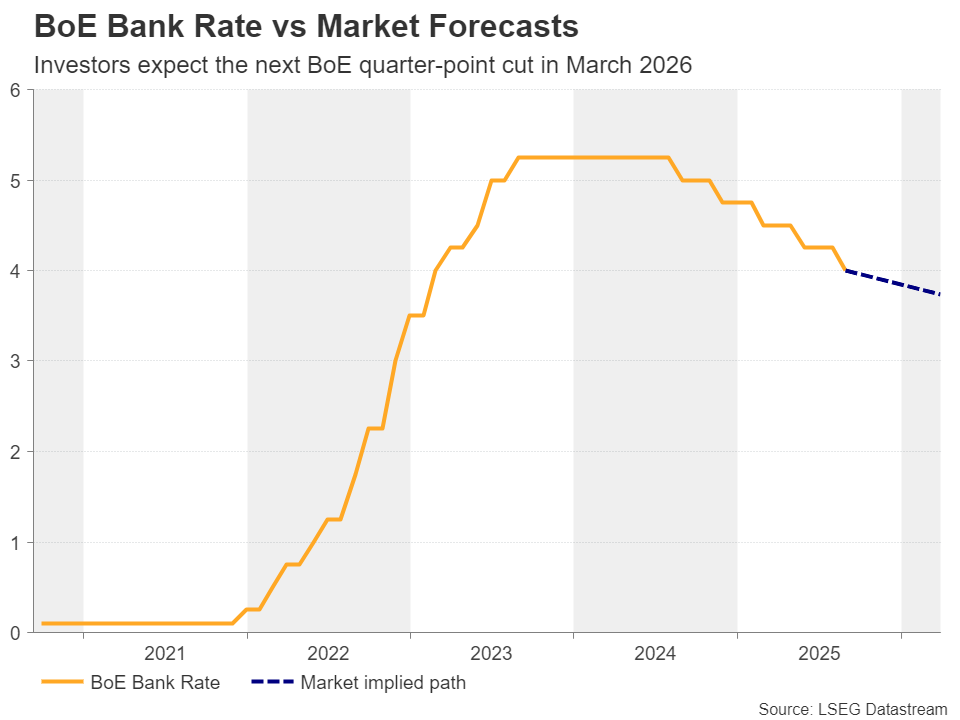

BoE to stay on hold, next rate cut seen in March

On Thursday, the central bank torch will be passed to the BoE, and during the Asian session on Friday, to the BoJ.

Getting the ball rolling with the BoE, British policymakers lowered borrowing costs to 4% in August, the lowest level for more than two years. However, the decision was so close that it took a second round of voting to be sealed.

In its Monetary Policy Report, the Bank projected inflation to peak at 4% in September, twice its target, while last week Governor Bailey said that “There is now considerably more doubt about when and exactly how quickly we can make those further steps."

Now, investors are nearly certain that the Bank will refrain from acting on Thursday. However, due to last month’s close call, the voting pattern could prove market moving for the pound as even one or two officials voting for a rate cut could prompt investors to bring forward their rate cut bets and thereby hurting the British currency. Currently, they are fully pencilling in the next quarter-point reduction to be delivered in March.

It is worth mentioning that ahead of Thursday’s decision, the UK CPI numbers for August will be released on Wednesday, and they could very well impact how policymakers will vote the next day. UK retail sales data are due out on Friday.

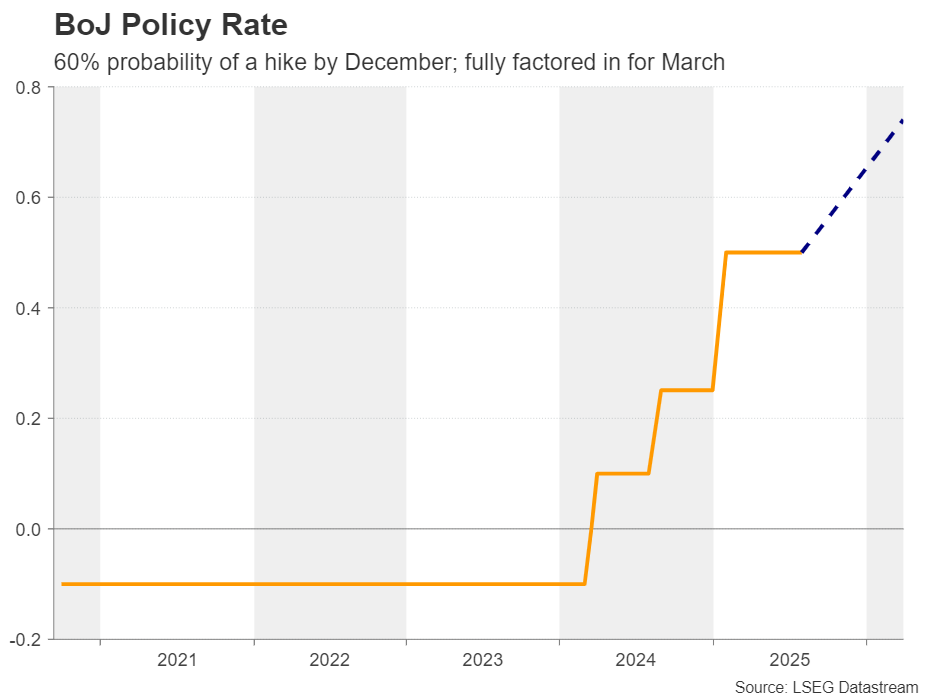

Will the BoJ remain willing to hike before year-end?

Passing the ball to Japan, following the resignation of prime minister Ishiba, there has been speculation that he will be replaced by someone who advocates looser fiscal and monetary policy, and thus the probability of a 25bps rate increase by the BoJ fell to below 50%.

However, investors were quick to recalibrate their BoJ hike bets following a report that the BoJ maintained the view that it may be possible to raise interest rates again this year despite the political turmoil, mainly due to economic conditions developing as expected.

Although the Bank is widely anticipated to refrain from acting next week, investors are now baking into the cake a 60% chance of a hike by the end of the year, while they are fully pricing in a quarter-point increase by March. Thus, all the attention will be on the forward guidance and Governor Ueda’s press conference.

If BoJ policymakers remain committed to take borrowing costs higher, the yen is likely to gain. However, delivering a clear message may be a difficult task. The Liberal Democratic Party (LDP) will hold an election on October 4 for Ishiba’s successor, a choice that could prove influential for monetary policy thereafter. Yes, the BoJ is independent, but alongside the government they issued a statement back in 2013 highlighting the importance of cooperation to fight deflation and spur economic growth.

One of the strongest candidates for taking Ishiba’s place is former economic security minister Sanae Takaichi, who is seen as pro-monetary easing. Therefore, anything suggesting that the BoJ will proceed at a slower pace or even dismiss future rate hikes, could prove quite negative for the Japanese currency.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.