Week ahead – Fed and BoC meet amid geopolitical upheaval and Trump’s Fed pick

- Fed to likely go on pause after three straight cuts.

- BoC is also expected to stand pat.

- But will Trump steal the limelight by revealing his Fed chair nomination?

- Eurozone GDP and Australian and Tokyo CPI to be watched too.

Fed to take a backseat in January

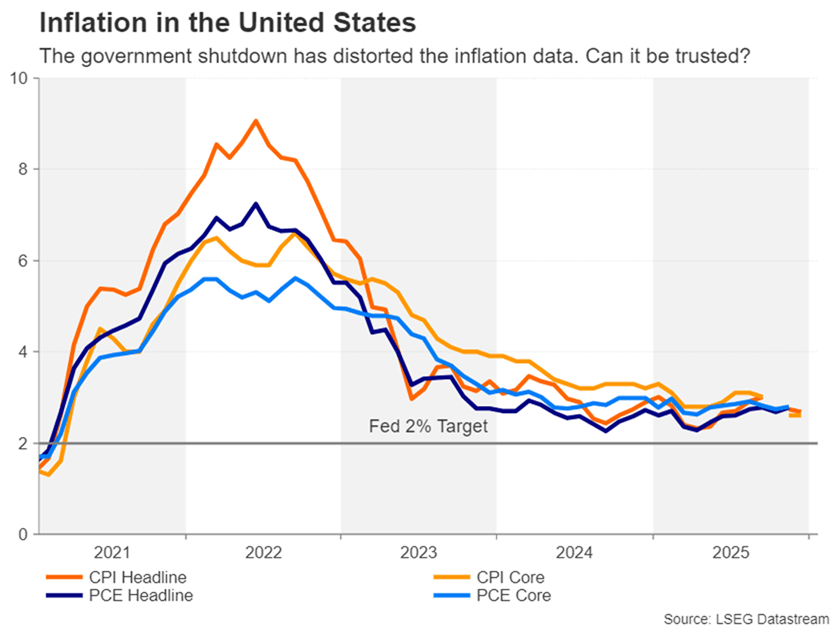

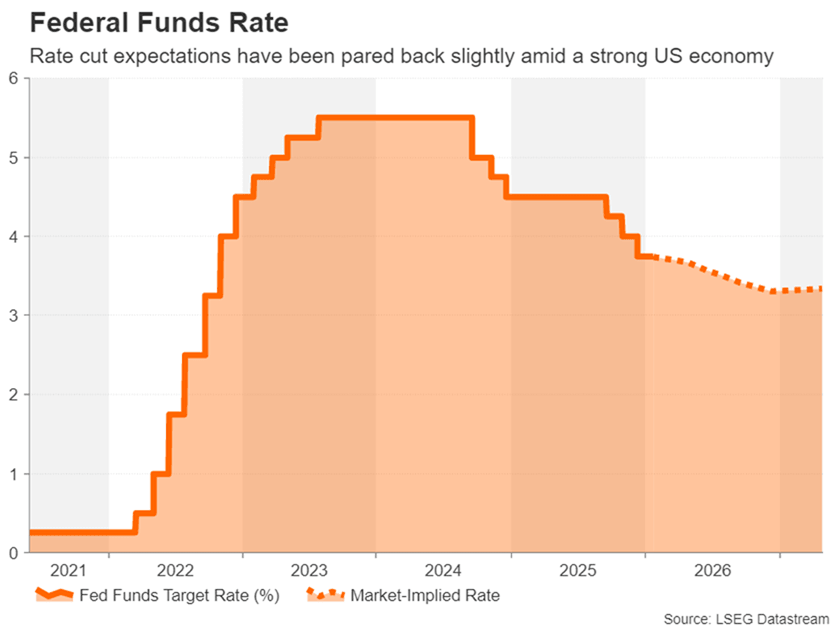

The Federal Reserve will hold its first policy meeting of the year next week, announcing its decision on Wednesday. No change in interest rates is anticipated, as Fed chief Jerome Powell signalled back at the December meeting that after three consecutive 25-bps cuts, the central bank “is well positioned to wait to see how the economy evolves”.

Concerns about the labour market necessitated the Fed to resume its easing cycle in September after jobs growth ground to a halt over the summer, even as inflation has stayed stubbornly above the 2% target. But there are signs that the jobs market has stabilized, and although the current “no hire, no fire” conditions are hardly screaming of recovery, the Fed can afford to take some time out to get a better picture of what is happening to inflation, amid a lot of noise in the data caused in part by the government shutdown.

Headline CPI moderated to 2.7% y/y in December, while core CPI was unchanged at 2.6%, reinforcing the view that inflation is now back in a downward trend following the temporary pickup in price pressures generated by Trump’s tariffs. Powell hasn’t shied away from blaming tariffs for the inflation overshoot but sounded quite upbeat in his December post-meeting press conference that it’s likely a "one-time price increase".

Nevertheless, Fed officials remain quite cautious, not just because inflation hasn’t reached 2% since 2021 and their credibility is at stake if they don’t meet their goal soon, but also because they’ve become less worried about the labour market. Far from slowing, the US economy is booming right now, with the Atlanta Fed’s GDPNow model putting growth in the final quarter of 2025 at an impressive 5.4%.

Hence, despite the recent softness in inflation readings, the Fed is unlikely to flag a faster pace of easing in the months ahead on Wednesday. Powell will probably try to justify the ongoing caution by talking up the economy. However, should he open the door to more than one 25-bps rate cut that’s been pencilled in the dot plot for 2026, this will be music to investors’ ears.

The US dollar is still reeling from Trump’s renewed tariffs threats over Greenland so any dovish surprises could trigger fresh selling pressure.

Will Trump finally announce Powell’s successor?

In terms of data, durable goods orders for November will start things off on Monday, followed by the Conference Board’s consumer confidence index on Tuesday, factory orders on Thursday and the Chicago PMI and producer price index on Friday.

It’s possible of course that the biggest highlight next week might not come from either the Fed or the data. President Trump may well try to steal Powell’s thunder by finally announcing who he will nominate to replace him in May. It is thought that the President has narrowed the selection to four candidates: White House economic adviser Kevin Hassett, Fed Governor Christopher Waller, former Fed Governor Kevin Warsh and Rick Rieder, who is BlackRock's chief bond investment manager and a recent addition to the list.

Equity traders would probably be happy with any of those finalists, but bond markets are more likely to be calmer if Waller is picked. The dollar, on the other hand, might not see a significant immediate reaction as investors might wait until there’s more clarity on the policy direction under the new leadership before responding.

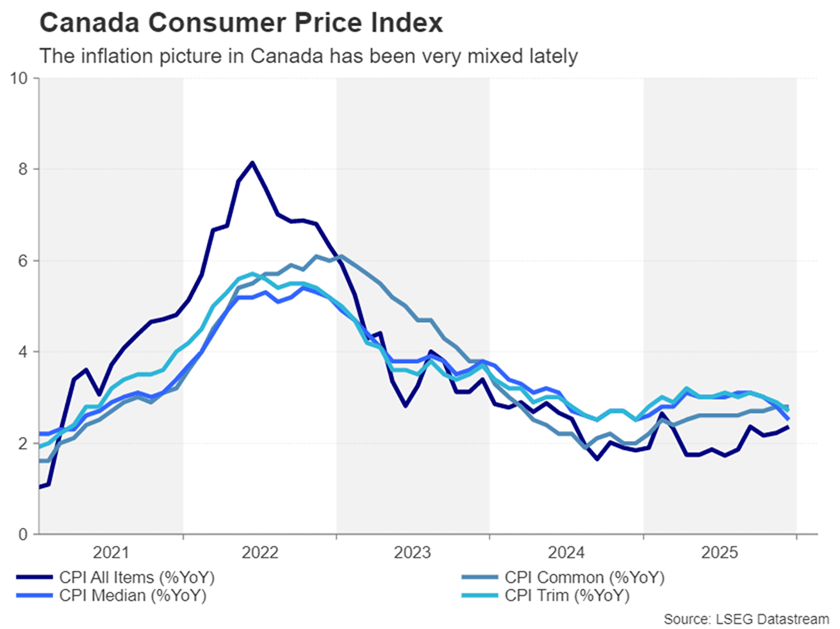

BoC set to stay on hold

With Powell potentially facing more attacks by Trump for not cutting rates next week, Canadian Prime Minister Mark Carney also remains unpopular at the White House. But despite the lack of progress towards lower US tariffs on Canadian exports not covered by the USMCA agreement, the Canadian economy appears to be holding up reasonably well. Employment has been rising since September and GDP growth bounced back in Q3. The next monthly reading is due on Friday.

Moreover, the inflation picture has been somewhat mixed lately, and so the Bank of Canada is almost certain to keep interest rates unchanged on Wednesday when it meets a few hours before the Fed.

Futures markets see around a 40% probability of a rate increase by year end. But should BoC officials keep the option of a cut on the table, the Canadian dollar could reverse some of its recent gains versus the greenback.

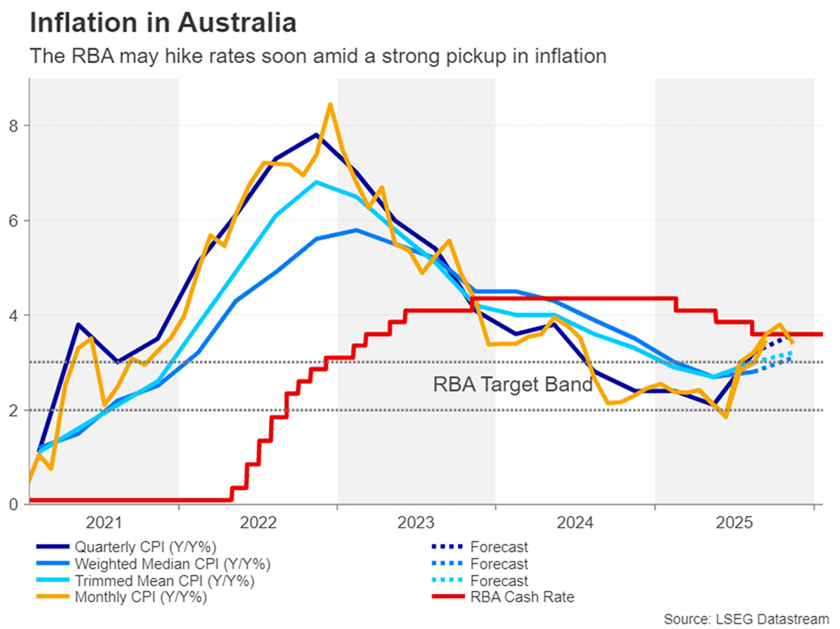

Will Australian CPI data seal the deal for RBA hike?

Meanwhile, in Australia, a rate rise is looking more and more likely, with investors assigning about a 58% probability that the Reserve Bank of Australia will lift the cash rate by 25 basis points when it meets on February 3.

Next week’s CPI release will be crucial in determining which way those odds swing. The quarterly prints are due on Wednesday along with the monthly numbers.

Headline CPI rose to 3.2% y/y in Q3 and is expected to have edged further up in Q4, as the monthly gauge jumped to 3.8% y/y in October before falling back to 3.4% in November.

Any downside surprises could be quite negative for the Australian dollar, which has been rallying over the past week on the growing rate hike bets. However, if the CPI report raises the likelihood of a hike, the aussie could soon set its sights on $0.6900.

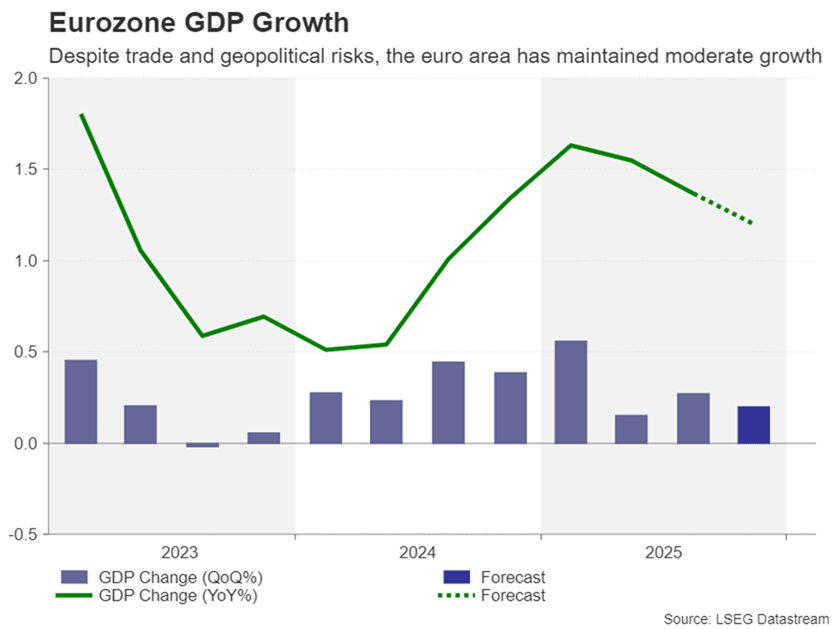

Eurozone data should keep euro supported

The easing of tensions between European capitals and Washington over Greenland’s autonomy has come as a major relief for the markets. But the crisis is far from over as discussions about a framework for a future deal barely scratch the surface on what all sides need to agree on.

The euro has been a surprise benefactor of the geopolitical headlines, as the dollar fell victim to the ‘sell America’ trade. That’s not to say there aren’t any vulnerabilities for the euro while negotiations take place about Greenland’s future.

One such risk is that a flareup of trade tensions between the EU and US would increase the chances of the European Central Bank cutting rates again this year. For now, though, the data is anticipated to continue supporting a neutral ECB.

The first estimate of Q4 GDP in the Eurozone is out on Friday, with forecasts of 0.2% q/q growth, slightly slower than the 0.3% pace of Q3.

Also on investors’ radar will be Germany’s Ifo business survey on Monday and the preliminary CPI figures for January on Friday.

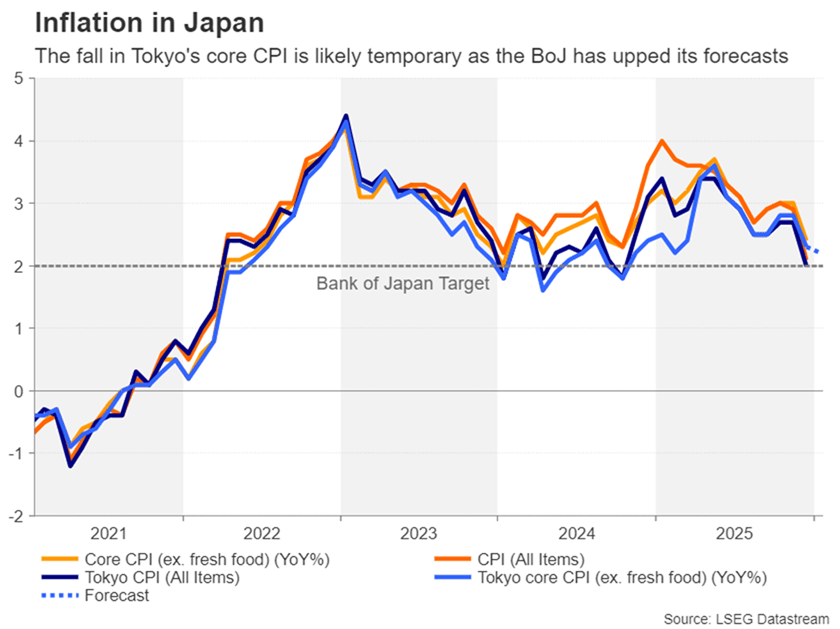

Focus turns to Tokyo CPI after BoJ decision

Finally, there will be more inflation data doing the rounds in Japan over the coming week, where CPI estimates for January are out on Friday for the Tokyo region. Core CPI fell to 2.3% y/y in December in Tokyo, pointing to some cooling in price pressures amid lower energy prices and an easing in food inflation.

Any further decline in January could weigh on the yen, as investors are still more focused on Japan’s mounting debt problem than the Bank of Japan’s increasingly hawkish stance. The BoJ raised its inflation outlook at its policy meeting this week, suggesting it’s ready to hike again soon, but the yen remains unconvinced.

With the yen unable to catch a break, there’s an elevated risk of intervention in FX markets by Japanese authorities in the next few days after a suspected ‘rate check’ on Friday. Authorities tend to conduct a rate check as a means of gauging the market and sending a signal that they are ready to intervene at any moment, so investors need to be on standby.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl