Wall Street’s post-downgrade rebound: Greedflation, grey zones, and the bonfire of the bond desks

Wall Street did what it does best—shrugged off a ratings downgrade with the kind of casual arrogance only a $35 trillion debtor can muster. After Moody’s notched U.S. sovereign credit down late Friday, equity markets opened this week with a brief panic… but not a panic anyone really bought into. The S&P 500 clawed back a full 1.1% intraday drop and came within a hair of breaking into bull market territory—before stalling out just shy of euphoria as retail earnings nerves set in.

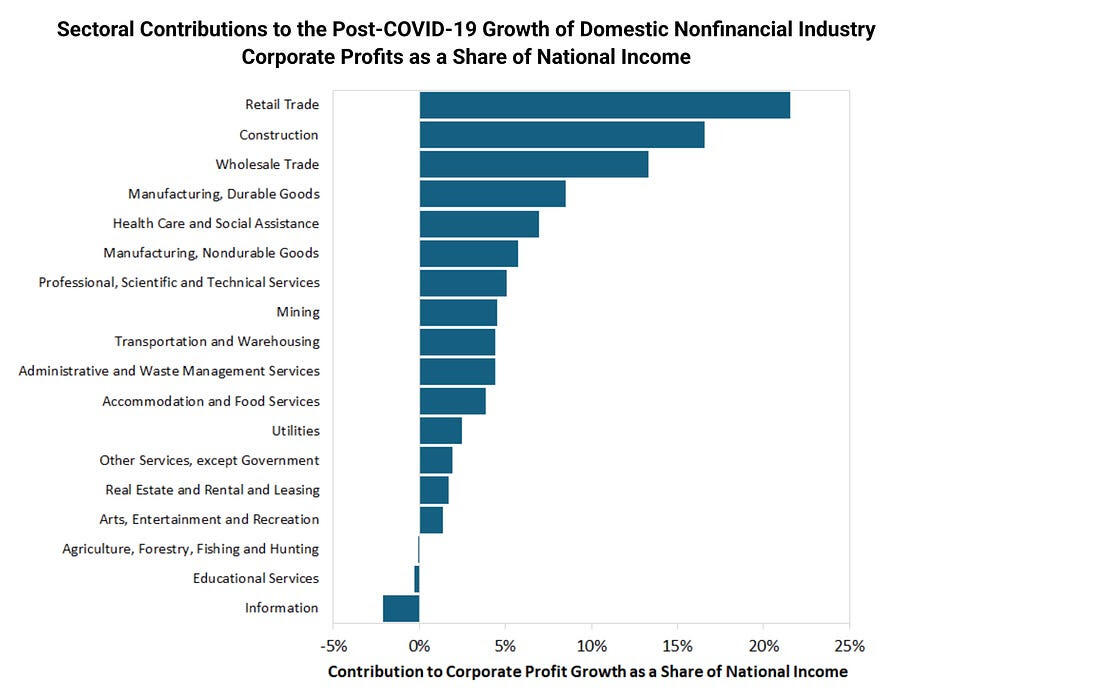

And rightly so. Walmart, America’s barometer for the middle class, lobbed a tariff grenade into the room, warning that prices are going up. Trump wasn’t having it—and he may have a point. The St. Louis Fed’s post-pandemic deep dive named the retail sector the biggest offender in the “Greedflation” Olympics, bloated margins and all. . The message from the White House is clear: big-box retailers have enough margin cushion to “eat the tariffs.” And something tells me that St. Louis Fed PDF is making the rounds at every Fortune 500 C-suite retailer ahead of earnings guidance.

Traders saw the downgrade for what it was: symbolic, not structural. A headline tempest in a teapot. The real tell came when the Treasury market opened and price discovery roared to life. Long bonds, oversold and left for dead during Asia’s grey-zone Monday morning liquidity void, were snapped up the moment real desks clocked in. By the time New York opened, the so-called downgrade fear had morphed into a classic “buy-the-dip” impulse across both bonds and equities.

Let’s be honest: the downgrade itself wasn’t the shock—it was the timing. Who drops this bombshell late Friday, then leaves it to thin Asian markets to mop it up? That’s not a ratings move—it’s a liquidity ambush. Moody’s effectively dumped the news into a ghost session, and predictably, UST futures slid deeper without a net. But when the real players showed up—those “Masters of the Universe” Tom Wolfe immortalized—bids returned, balance sheets opened, and the whole thing looked more like a liquidity mismatch than a crisis.

Treasuries rebounded with gusto. Even the 30-year, which briefly kissed 5% yields, came back like a boomerang. Helping matters? A tactical oil pullback, as Trump teased the potential for immediate Ukraine-Russia talks. Sure, we’ve seen this script before, but even a whiff of ceasefire potential was enough to knock crude lower—and give the Fed’s inflation battle a tailwind for the week.

FX followed the risk-on script. The euro backed off the highs but remained comfortably above 1.1200, underpinned by stable PMIs and political optics in Europe. Meanwhile, the dollar is still patching up its wounds against the yen—hovering just under 145—but with global risk appetite flickering back, haven flows are ebbing in the New York session. The dollar's structural headwind has now turned into a weak cross-breeze.

And here's the kicker: while Moody’s downgrade feels like a big moment, the analysis is now shifting to "non-event" territory. There’s no new fiscal info here—just the inevitable acknowledgment of what every international bond investor already knows. What does matter, though, is the mechanics of Treasury supply. With 23% of U.S. issuance now financed through bills—well above the 15% sweet spot—any hint that Treasury Secretary Bessent will keep pressure off long-duration supply is a stealth bullish tailwind for the bond complex.

The real boon? The push to exempt Treasuries from bank liquidity ratios. That’s a big deal—underappreciated, underpriced, and absolutely bullish for duration demand at the margin.

But there’s a sting in the tail: Trump’s tax cut package. It may have minimal deficit-reducing capacity in its current form. While the headline cost of extending existing cuts looks nasty on paper, the reality is it’s already baked into current issuance patterns. No new pressure on supply there—but no help either. For now, the long end stays twitchy, duration traders remain jumpy, and the only certainty is that volatility’s back on the menu.

This wasn’t a meltdown—it was a misfire. Moody’s downgrade was a headline event dumped into a market void. Once real liquidity returned, cooler heads prevailed. Treasuries found a bid, equities recalibrated, and traders rotated into risk as the downgrade dust settled. But don’t get comfortable. We’re trading inside a narrative blender—tariffs, tax cuts, ratings drama, and retail greed all mixed into a frothy, policy-fueled cocktail. Stay sharp, stay cynical, and don’t underestimate the tail risk of a structurally softer dollar creeping in through the back door.

But don’t assume risk isn’t off the table—U.S. sovereign credit jitters are still simmering, and with the 'X-Date' creeping closer, the clock’s ticking louder.

The view

After last week’s 5% melt-up, U.S. equities took a breather—call it a strategic timeout rather than a reversal. Monday opened with no real data, no major catalysts, and a Moody’s downgrade still echoing across the weekend wires. But let’s be honest: this wasn’t panic—it was portfolio indigestion. The tape felt like traders were forced to chew through stale headlines on a slow Monday menu.

And yet, despite the weekend FUD and doomscrolling, the S&P erased a 0.75% drop like it never happened. Mag7 lagged, but the real story was in the broader tape—S&P 493 holding flat while cash buyers soaked up the dip. The downgrade? A nothingburger with fries. Traders rightly saw it as a backward-looking slap, a ratings agency finally catching up to what the bond market’s been screaming about for months. By the time the U.S. cash session kicked off, it was clear: this wasn’t a crisis, it was a re-entry point.

And then there's the “fear of the right-tail.” Nomura’s right—this is the first time in a while we’re seeing real call skew distortion. Dealers are short upside. Clients are chasing late. Everyone missed the move, and now it’s panic-bid. The pain trade now is higher, faster, dumber, and under-owned.

But don’t get comfortable.

A monster calendar lurks just beneath the surface: looming tariff deadlines, debt ceiling brinkmanship, and a Fed still pricing in two cuts for 2025 and another two in 2026—a soft landing fantasy built on sand. If these tariffs land harder—as Trump hinted in Abu Dhabi and Bessent warned for those refusing to negotiate in good faith—global capital flows won’t just flinch, they’ll bolt. And if the “China model” of hardball negotiations goes viral, we’re staring down a global trade war dressed up as policy reform.

In other words, the path of least resistance is still higher… faster… until it all comes crashing down—rinse, repeat.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.