Wall Street sours, Tokyo trembles; Bond vigilantes call the shots

The big tech sugar high wore off overnight, with Wall Street snapping its six-day winning streak in a session that sputtered from soft open to risk-off reversal, dragging the S&P 500 and Nasdaq into the red since the Moody’s downgrade. While the proximate catalyst was a gumbo of headline risk, from Speaker Johnson’s deficit hawkery to Elon’s unfiltered CNBC Doge truth serum, to bond markets across the G4 on edge as debt worries are beginning to vex more broadly—It was Trump’s failed pitch to key House Republicans on SALT caps that truly soured sentiment. The selloff deepened as long-end yields marched higher and confidence in the “Big, Beautiful Bill” thinned out like fiscal credibility itself.

But while the U.S. dealt with partisan gridlock and a sliding dollar, Asia was jolted awake by something far more systemic—a full-blown bond market rebellion in Japan. Tuesday’s 20-year JGB auction was the worst since 1987, with tails blowing out to 1.14%, and 40-year yields exploding to record highs. The BoJ’s carefully constructed bond façade cracked wide open, and investors—especially those holding the $1.13 trillion in U.S. Treasuries Japan owns—took notice. If Tokyo’s bond vigilantes are ringing alarm bells, don’t be shocked if D.C. hears the echoes.

While the last 30 minutes brought out the S&P 500 dip-buyers, they couldn’t drag the tape into the green. U.S. equity futures are limping into Asia, still choking on the growing disconnect between risk asset cheer and bond market dread. The divergence is now widening like a yield curve gone rogue.

We’re not in “out of the woods” territory —this is recalibration mode. Duration risk is going global, fiscal complacency is being repriced in real time, and the illusion of harmony between stocks and rates is starting to fracture. The vibe shift is real—and the bond market’s calling the tune now.

And here’s the kicker: gold caught a monster intraday bid, reversing early weakness and reaffirming its no-counterparty-status crown. The JGB chaos + U.S. downgrade + unresolved deficit narrative was a perfect storm for bullion buyers—and if you were wondering why we told you to load up on last weeks dip, China just answered it. Mainland gold imports surged 73% in April to 127.5 metric tons—the highest in nearly a year—despite record prices. That’s not retail flow. That’s central bank insurance. Quiet. Steady. Relentless.

Add in ongoing geopolitical noise, record gold buying from Asia, and Washington’s slow-moving fiscal implosion, and you’ve got a setup where gold doesn’t just hedge risk—it front-runs it.

Elsewhere in FX, USDJPY continues to grind lower, weighed down by speculation of currency clauses being floated in bilateral U.S.-Asia trade deals. Traders are already positioning ahead of this week’s G7 FX discussions, with whispers that Washington may pressure Tokyo and others to back off currency caps. That doesn’t bode well for the yen—or the fragile long end of the JGB curve.

Meanwhile, EURUSD continues to float higher, supported by steady inflows. The Eurozone current account surplus hit €51B in March, driven by foreign equity inflows and repatriation, bolstering the thesis that capital rotation is alive and well. With U.S. long-end risks festering and macro data softening, the euro’s quietly becoming the cleaner shirt in a very dirty laundry basket.

Today’s watchlist:

-

The $16bn 20-year UST auction at 1 p.m. NY time is must-see TV. If it flops like Japan’s did, expect a repricing tsunami in rates, FX, and gold and stocks will tank.

-

G7 meetings kick off, with FX intervention narratives in play. USDJPY traders, stay nimble.

-

More Fed speak, but its impact is merely secondary and distant noise.

Global markets aren’t panicking—but they are pricing in risk differently now. The tech melt-up is running out of steam, sovereign bond markets are entering a credibility test phase, and gold’s catching a bid not just on fear—but on policy failure. Buckle up—the real price discovery window may open in the bond pits before it hits the index boards.

The view

Investors have long tolerated the theatre of expanding U.S. debt, shrugging off trillion-dollar deficits like background noise in a bull market. But that détente evaporates the moment the bill comes due. Tolerance turns to terror when maturity walls meet rising yields, and suddenly the absurd becomes unsustainable.

Markets are fine with fiscal fantasy—until they’re forced to fund it. Then it’s hell.

Many scratched their heads when, on the first trading day after the Moody’s downgrade, stocks ripped higher—reversing a red premarket and closing solidly green. How could that be? Back in August 2011, when S&P stripped the U.S. of its AAA, the S&P 500 tumbled 7% in days. The difference now?

Simple: Investors have accepted that U.S. debt will balloon at an absurd pace... until there’s hell to pay.

As Deutsche Bank’s Jim Reid bluntly put it, the U.S. debt path is unsustainable and everyone knows it—the only unknown is when it breaks. And Liberation Day may have pulled that reckoning forward. Whether by accident or Trump’s design, America’s “exorbitant privilege” is eroding, and with it, the dollar’s reserve supremacy.

According to DB, this privilege—the ability to borrow at artificially low rates—shaves 70bps off U.S. borrowing costs, letting the government run a debt-to-GDP ratio 25 percentage points higher without feeling the burn. But once the market starts pricing debt at fair value, that math falls apart—fast.

-638833762403104134.jpg)

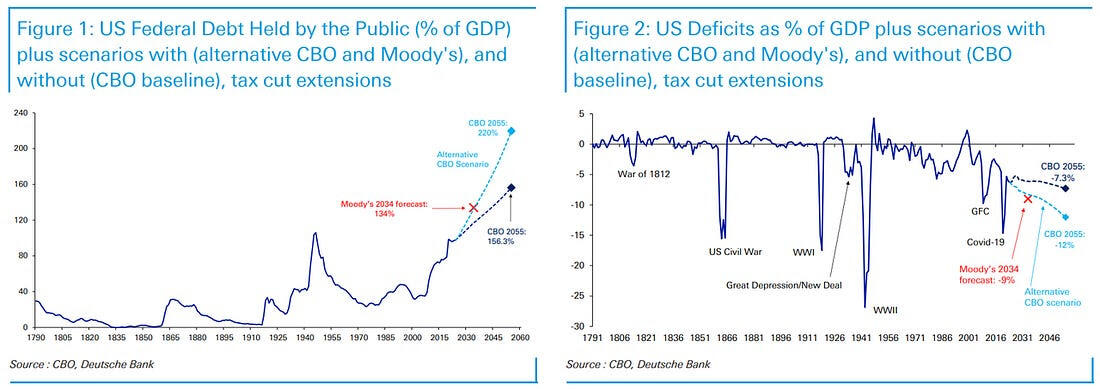

Moody’s downgrade isn’t a shock. But it is another crack in the façade. Their updated projections are brutal:

-

Interest + mandatory spending = 78% of total outlays by 2035 (up from 73% today)

-

Deficit = ~9% of GDP by 2035

-

Debt-to-GDP = 134% by 2035 (from ~98% now)

And if the 2017 tax cuts are extended, alternative CBO scenarios push debt north of 200% of GDP over time. That’s not a slippery slope—that’s a fiscal cliff in slow motion.

So where does “hell to pay” live on the chart? Somewhere along the light blue line—the debt doomsday trajectory. We haven’t hit it yet. But we’re on the ramp.

Until then, markets may grind higher on liquidity, hope, and FOMO—but make no mistake, the endgame has a timestamp. We just don’t know when the fuse runs out.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.