US Tax Reform Stumble, Trump in Asia, Bitcoin

Wednesday's economic calendar won't be turning any heads given the absence of first tier data across the board. Instead, the focus will be on global risk sentiment and broad appetite, or lack thereof for the US Dollar. US tax reform updates and the Trump Asia tour are in focus.

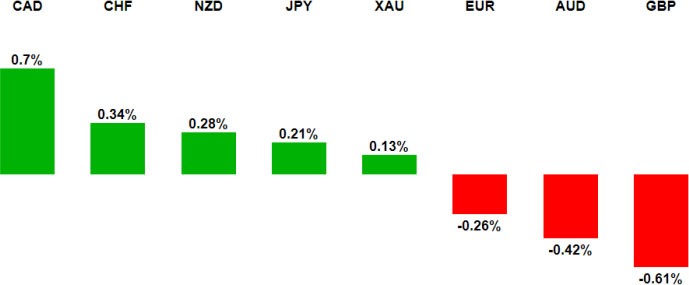

Five day performance v. US dollar

Author

LMAX Group Research Desk

LMAX Group

LMAX Group is a dynamic, visionary and award-winning financial technology company.

More from LMAX Group Research Desk