2.50%: Why the Kiwi's first hike in three years is a wager on a number nobody can see

The Reserve Bank of New Zealand (RBNZ) raised the Official Cash Rate (OCR) by 25 basis points to 2.50% at 02:00 GMT on Wednesday, its first hike in three years and the moment the bank that cut deeper than any G10 peer last cycle turned to face the other way. The entire cycle now rests on a number the bank openly admits it cannot see: Governor Anna Breman placed neutral somewhere between 2.50% and 3.50%, which means the OCR is either already home or barely a third of the way there.

Markets have decided it is the latter, and have priced nearly the bank's whole multi-year track into the next twelve months. That gap, between what is priced and what the bank has actually signalled, is what the Kiwi trades on from here.

The vote itself shows a committee that talked itself into moving. In May the Monetary Policy Committee (MPC) split three against three, and Breman's vote held the rate at 2.25%, the lowest since July 2022 and a level the central bank has all but conceded was the product of cutting too far. As recently as January, Breman was still talking down the prospect of an early hike and holding open the possibility that the next move would be lower. Barely eight months after the last cut of the easing cycle, the same committee reached consensus to reverse course, approving for good measure the wind-down of the final pandemic-era bond holdings by June 2027.

Feeling for neutral in the dark

Breman framed the move as the start of a gradual shift toward neutral, then spent her press conference conceding the bank is feeling its way toward a rate it cannot observe. The committee's own range for neutral runs 2.50%-3.50%, and members disagreed openly about where in that band reality sits.

External member Prasanna Gai argued the geoeconomic shocks of the past year may have pushed neutral higher by shrinking global productive capacity relative to investment demand, while the meeting record shows Gai and Hayley Gourley seeing inflation risks tilted higher against a Breman, Paul Conway, Karen Silk, and Carl Hansen bloc that judged them balanced.

That band is the whole trade: If neutral sits at the bottom, Wednesday's hike was the destination, and the cycle is done in one or two moves. If Gai is right and neutral has drifted toward the top, the bank has four more hikes just to reach flat, before it even considers restriction. The International Monetary Fund (IMF) has pushed the bank toward neutral for precisely this reason: A central bank parked below neutral has nowhere to cut from when the next shock lands.

The bank that hiked after the peak

Here is the part the wires will not dwell on: By the RBNZ's own numbers, the tightening cycle began after inflation peaked. May's statement projected the peak at 4.3% in the September quarter; Wednesday's revision says it already happened, at 3.9% in the June quarter, easing to 3.3% by September and back to the 2% midpoint by mid-2027. The peak was revised down and backdated, and the committee hiked anyway.

The defence is risk management rather than the data. The bank judged 2.25% was still adding stimulus to an economy it no longer wants stimulated, household inflation expectations have climbed to 3.4%, the highest since 2023, and rule-based work doing the rounds on the sell side pointed to a first hike already overdue in May. The partial reopening of the Strait of Hormuz has dragged fuel and petrochemical prices lower and taken the edge off the near-term numbers, but the committee warned the shock's effects will linger.

Growth offers little cover either way: Gross Domestic Product (GDP) shrank 0.1% in the opening quarter, the recovery lost momentum through the June quarter, and the bank's own nowcast pencils in 0.6% growth for September.

Three and a half hikes the bank never promised

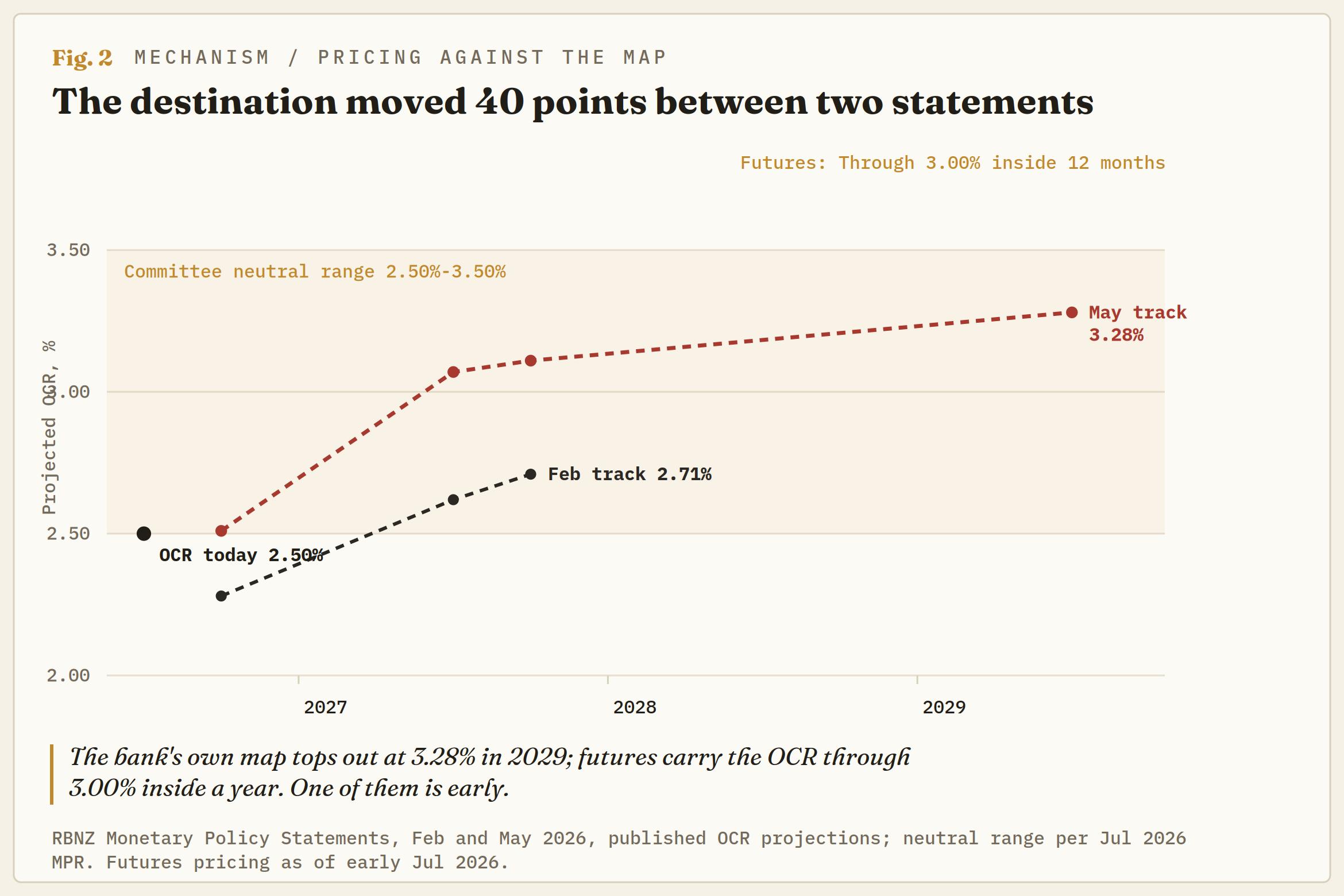

Rates markets price roughly three and a half hikes across the coming year, which carries the OCR through 3.00% by the middle of 2027. The bank's own May projections tell a slower story: An OCR averaging just above 2.50% this quarter, 3.07% by June 2027, and a top of 3.28% that does not arrive until 2029. These rates would surround a central neutral estimate of 3.00%. The market is running at the front edge of the bank's timetable, by up to two years on some desks, all priced against a committee that could not find a majority for a single hike six weeks ago.

Strategists at more than one European house have called that pricing “stretched” for an economy that just printed negative growth, and they argue the eventual unwind of those expectations, not the hikes themselves, is the medium-term Kiwi story. The risk-reward reads the same way: The hawkish case is already in the price, while the dovish case has every one of those priced hikes to feed on. Chasing Kiwi strength on hike headlines is buying the most crowded version of the story.

The Tasman spring is fully compressed

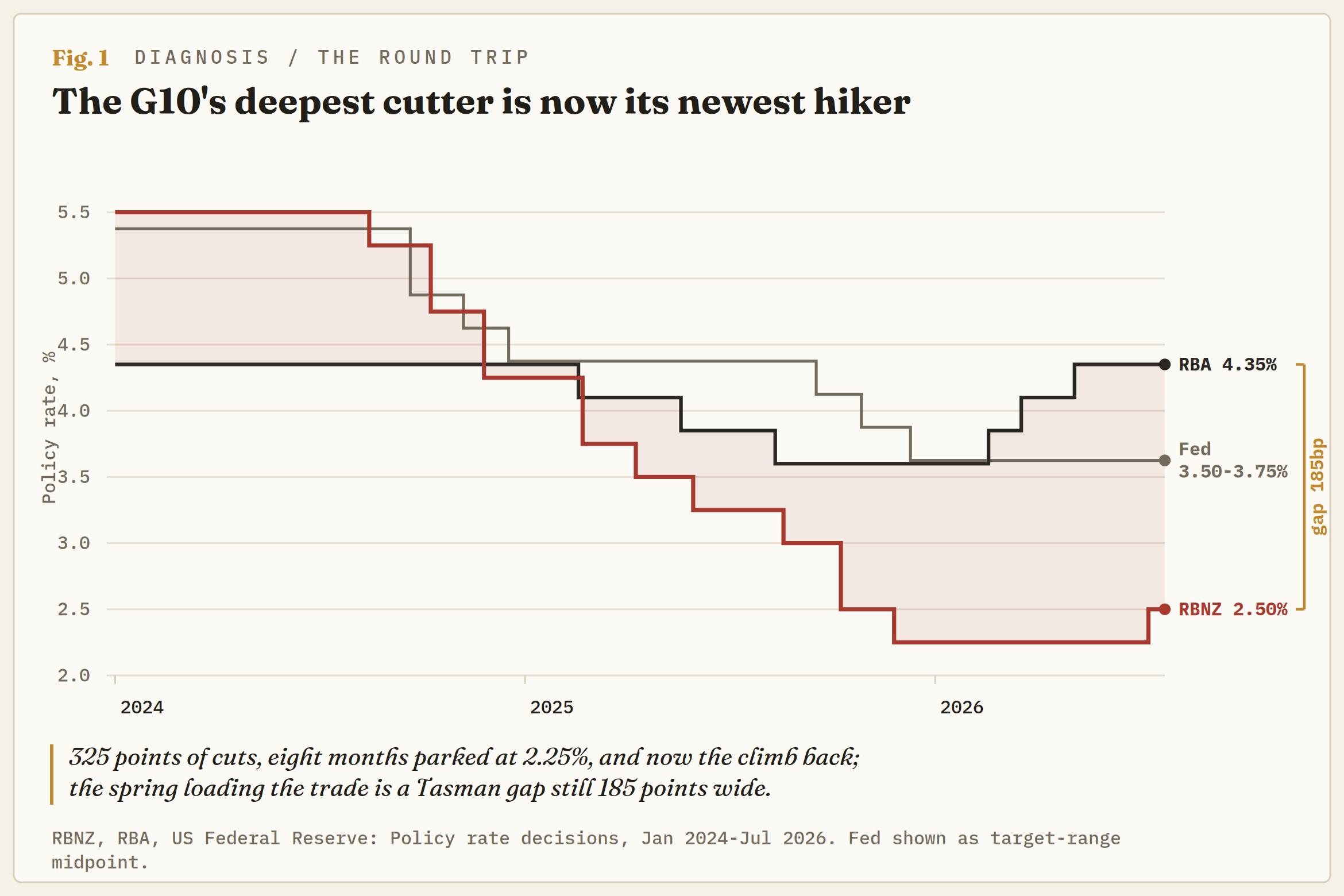

Across the ditch, the Reserve Bank of Australia (RBA) has already done what the RBNZ is only beginning. Three hikes between February and May took the cash rate to 4.35%, the June hold was unanimous, and three of the four Australian majors see no further moves this year with cuts pencilled through 2027 toward 3.60%-3.85%. The trans-Tasman policy gap peaked at 210 basis points going into Wednesday, the widest of the cycle, and has only now begun to close.

The cross wears the damage. The Kiwi opened the year at its weakest against the Aussie Dollar since 2013 and has stretched further since. AUD/NZD has spent the past two months pinned above 1.2000, ground it last held thirteen years ago at levels that price the divergence as permanent.

It is not: If the RBNZ delivers even half of what markets have priced in while the RBA sits on its hands, the gap compresses by more than 100 basis points inside a year, and forecasted RBA cuts in 2027 do the rest. This is the cleanest expression of the whole story, because it strips the Federal Reserve (Fed) out of the trade entirely.

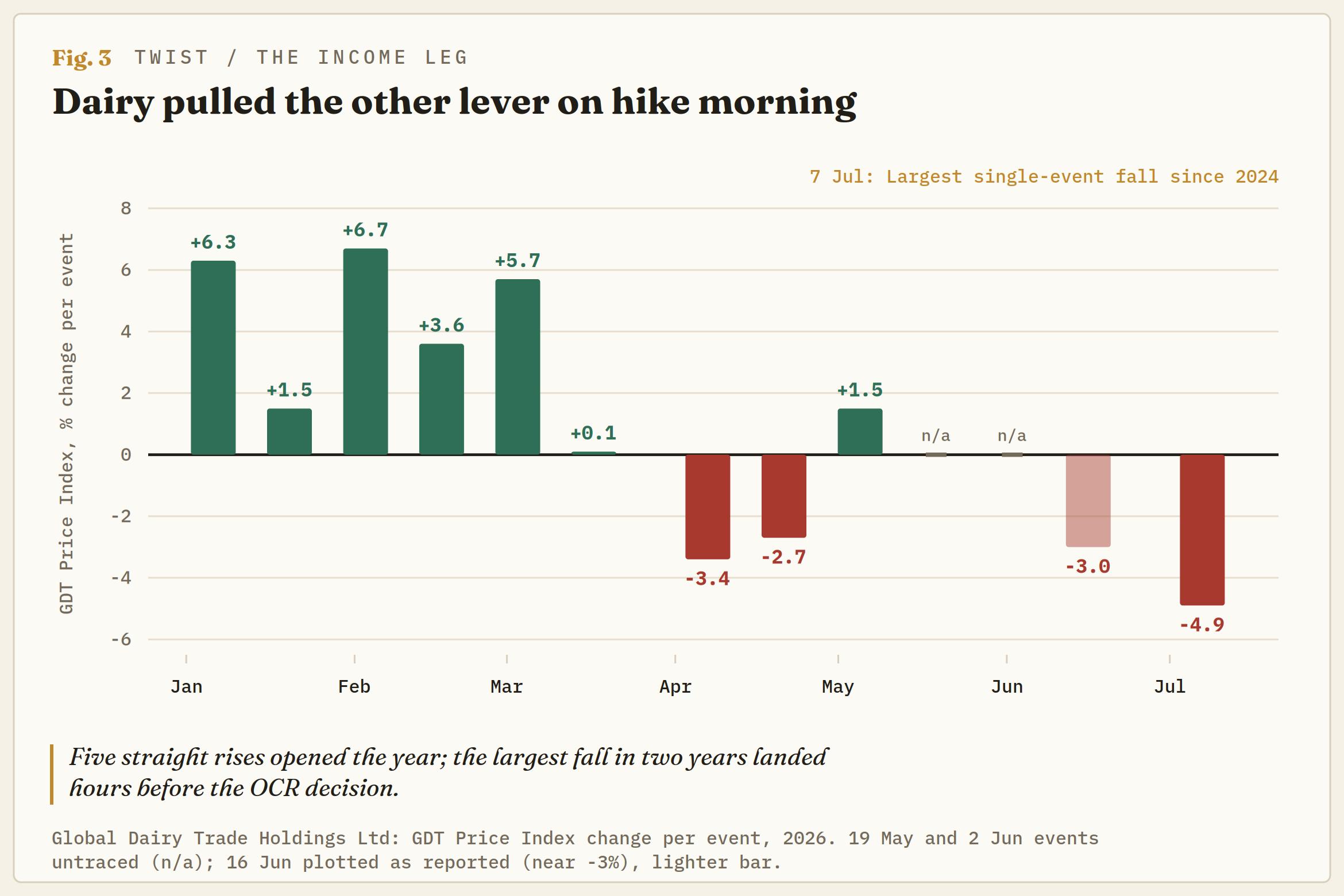

Dairy just pulled the other lever

Hours before the decision, the Global Dairy Trade (GDT) auction handed the Kiwi its counterargument. The index fell almost 5%, the largest drop in two years, following a near 3% fall at the previous event; whole milk powder shed 4.4%, skim milk powder 7%, and cheddar more than 12%. Five consecutive rises opened 2026 and had economists talking farmgate forecasts higher,

The index has been leaking since early April and has now surrendered most of the new year rally, with global milk production growing across every major region except China, where output is down 4.6% YoY.

Dairy is more than 29% of New Zealand's goods exports by value, which makes GDT the income leg of every Kiwi trade. That leg turned down in the same week the rate leg turned up. If farmgate forecasts start coming down into spring, rural incomes soften precisely as mortgage rates reset higher, and the committee's appetite for the back half of those priced hikes goes with it. This is the kill-switch on the hawkish trade, and it is already flashing.

A floor written in central bank prose

Buried in the statement is the most tradeable sentence of the day. The committee said Wednesday's hike was partly intended to prevent an unwarranted further easing in financial conditions, having noted that lower wholesale rates and a weaker exchange rate had loosened them in recent weeks. Strip the language back and the message is plain: Kiwi weakness is now itself a reason to hike.

A central bank that tightens when its currency falls has handed the market a soft floor. Every leg lower in the Kiwi mechanically raises the odds of the next hike, which caps how far the leg can run. The setup argues for fading extremes rather than chasing breaks, in both directions.

Two chairs, no guidance

The RBNZ says further increases appear likely, but their timing is highly uncertain, and it will not be drawn further. In Washington the posture is the same: Kevin Warsh's Fed has scrapped forward guidance outright, and Warsh became the first chair since the dot plot began in 2012 to withhold his own projection. The June dots still shifted the median to 3.8% by year-end, with nine of the 18 submitted projections showing at least one hike. That dot plot came before a 57K June payrolls print and 74K of downward jobs revisions cut September hiking odds to roughly one in two from two in three.

The Kiwi's rate differential with the US Dollar is, therefore, narrowing from both ends at once. The RBNZ is hiking from below, while Fed hike bets fade from above. With neither chair willing to steer, every Consumer Price Index (CPI) release and payrolls report carries the full weight of repricing on its own. That is a case for owning volatility around the event ladder rather than running naked spot through it.

The trading framework

NZD/USD snapped back to 0.5700 on the decision after carving out a July base just ahead of 0.5600, with the December floor sitting under that handle. The 0.5600 handle is the line in the sand: The bid is intact while it holds on a closing basis, and daily momentum is already curling up from oversold.

Topside, the falling 50 and 200-day Exponential Moving Averages (EMAs) bracket the road back, just below 0.5800 and just shy of 0.5850. That zone decides range versus trend, and a daily close above 0.5850 turns the setup from fade to follow. The lean is to buy dips ahead of 0.5600 into the September meeting while the data validates the path.

On the cross, the lean is short AUD/NZD toward 1.2000 first, the June shakeout area, with the rising 200-day EMA below 1.1850 as the full convergence objective. A daily close above 1.2300, through the top of the two-month range, is the invalidation. A 185-basis-point policy gap against a bank that delivered its first hike this week is as clean as a convergence setup gets, but the position pays away 185 points of carry while you wait, so the trade wants a catalyst rather than a base camp.

The ladder supplies the catalysts. The June-quarter CPI print lands mid-July and is the single biggest input, either confirming the 3.9% peak or breaking the whole framework.

The Federal Open Market Committee (FOMC) meets July 28-29; the RBA decides August 11; New Zealand labour data follows in early August; the RBNZ returns September 2 with a full statement; and the Fed meets again in mid-September. GDT prints every fortnight are the running tell on the income side.

The regime triggers are clean: CPI at or above the peak with dairy prices stabilising keeps the hiking path and both convergence trades alive, while a CPI undershoot alongside a further GDT slide is the signal the three and a half priced hikes start coming out, and the Kiwi with them.

The RBNZ spent 2025 cutting toward a floor it misjudged and will spend the rest of 2026 climbing toward a ceiling it cannot locate. Somewhere between 2.50% and 3.50%, the bank believes, gravity switches off. Markets have bet heavily on the top of that range in the same week the country's biggest export posted its hardest fall in two years. One of them is wrong, and the Kiwi is the instrument that settles it.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.