US service sector slows as businesses facing higher costs

US Feb ADP private payroll data and ISM non-manufacturing PMI, both missed estimates. The risk sentiment has turned negative overnight. US bond yields have inched higher across the curve with 2y up 2bps at 0.14% and 10y at 1.48%. The Nasdaq underperformed the Dow and the S&P, ending 2.7% lower.

Fed member Evans said that further monetary policy stimulus may not be needed if the US parliament manages to pass the USD 1.9tn stimulus package.

The US Dollar has strengthened overnight across the board on an uptick in US yields. The focus will be on Fed Chair Powell's speech today evening to see if he acknowledges if downside risks to the economy have receded or whether he reiterates that the US is still from its employment and inflation objectives.

The UK government tabled an expansionary budget, extending tax holidays and continuing to support measures to the economy. Fiscal consolidation has been put on hold as of now. The UK economy is likely to reach pre-pandemic levels by mid-2022, earlier than previously forecast.

The Rupee strengthened yesterday on inflows and exporter selling on a break below 73.15. Nationalized banks were absent from bids as a result of which USD/INR plumbed lows of around 72.70.

Also in focus will be the US jobless claims and the outcome of the OPEC+ meet.

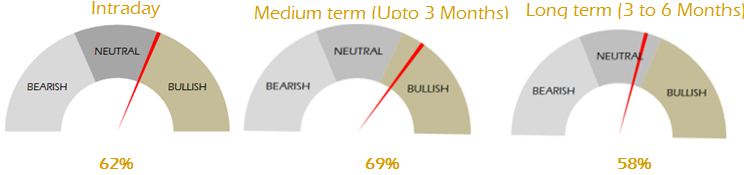

Strategy: Exporters are advised to cover a part of their near-term exposure on upticks towards 73.50. Importers are advised to cover through forwards on dips towards 72.50. The 3M range for USDINR is 72.50 – 74.40 and the 6M range is 73.00 – 76.00.

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.