US Retail Sales Preview: Last V-shaped recovery hopes? Three reasons for upbeat figures, S&P 500 may rise

- Economists expect US retail sales figures to have risen in June.

- A comeback characterized the beginning of the month and COVID-19 shy consumers later.

- Fiscal stimulus may have boosted consumption more than expected, thus boosting stocks.

Coronavirus hit the consumer hard – but that happened only mid-way through June, thus only partially reflected in the upcoming Retail Sales report. Will the figures show the recovery or the new downturn?

As cases were rising rapidly in Florida, Texas, California, Arizona, and other states, expenditure began dropping in most America. Shoppers and diners did not wait for restrictions – in Texas' cases that included taverns – but skipped social activities.

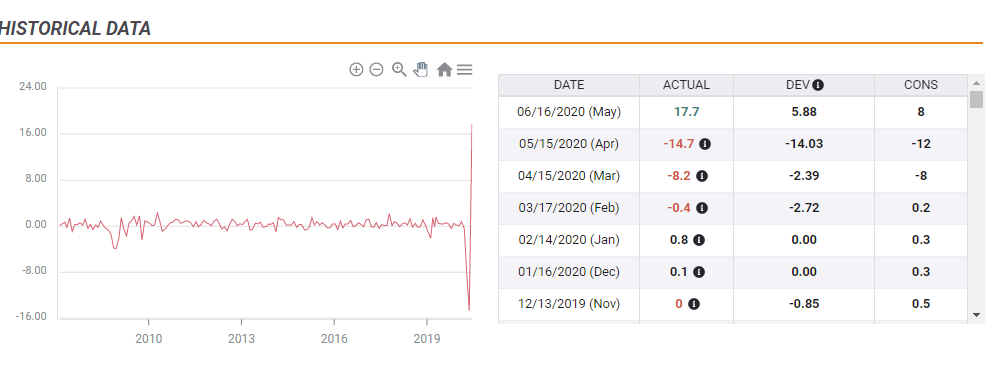

Economists expect the rebound to continue, perhaps reflecting the first half of the month – and supporting the hopes of a V-shaped recovery. Headline sales tumbled by 8.2% in March and 14.7% in April, before rebounding by 17.7% in May. For June, estimates stand at an increase of 5%, sending the total volume closer to the levels that were seen in February.

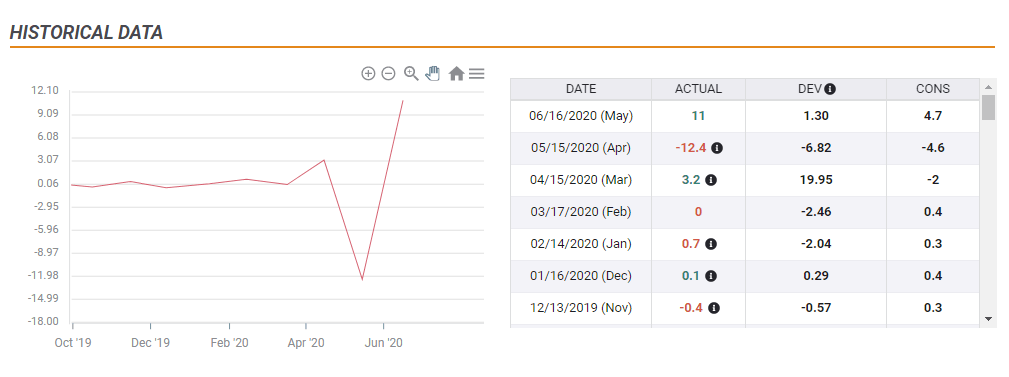

The Retail Sales Control Group – also known as the "core of the core" – has suffered less than the headline, surprisingly rising in March by 3.2%, then tumbling by 12.4% in April and bouncing by 11% in May.

The measure is projected to rise by 3.6% in June. That would put the control group back to pre-pandemic levels.

Are these projections too optimistic? Probably not.

Three reasons to be optimistic

1) Mid-June

Coronavirus cases were under control up to the middle of last month and state accelerated their reopening – encouraging shoppers to buy. The change was not sudden but gradual, and the figures will likely better reflect the increase in expenditure rather than the renewed downturn.

Moreover, it is essential to note that retail sales figures experience substantial revisions – and the slide in the latter part of the month may be reflected only with the modified data, not the initial release.

2) Cases rose in the south, retreated in the north

In mid-July when the data is due, COVID-19 infections are rising in most of America, the mortality rate is on the rise, and hospitals in some cities are filling. However, while several states in the south were experiencing a surge during June, the greater New York area continued seeing an improvement.

Life returned to normal in some places while some were hunkering down, balancing the picture.

3) Fiscal stimulus

Congress approved multi-trillion relief packages, including a $600 per week top-tup for the unemployed and a $1,200 check for every American. Additional funds were sent to large and small firms.

The money could not be spent at once – especially not during the severe lockdowns. Some of the expenditure was deferred from April to May, but more probably occurred in June.

Consumers may have wanted to compensate themselves for the lost time – not only by splashing on home-improvement equipment, but also on eating out, buying clothes, and other activities. While some of the government programs' effect was already seen, it may have likely spilled into June.

Market reaction

Investors are bullish – currently not on the US consumer – but on hopes for a coronavirus vaccine. Reports of progress by both Moderna and AstraZeneca have kept equities bid. It would take horrible retail sales figures to depress investors.

If sales meet expectations, marginally miss them, or surprise with a beat, the S&P 500 will likely rise and the safe-haven dollar could fall.

Only negative retail sales statistics would send stocks down the greenback higher – and that seems highly unlikely.

Weekly US jobless claims are released at the same time, 12:30 GMT. However, initial claims are for the week ending July 10 and continuing claims are for that concluding July 3 – both not consisting of July 12, when the Non-Farm Payrolls surveys are held.

Moreover, consumption is central to the US economy, and the monthly retail sales report will likely overshadow weekly labor statistics.

Conclusion

Overall, the recovery likely extended through June as most of the nation was still reopening during around half of the month and as government support helps. The upbeat market mood implies only a devastating report would dampen the mood, while anything else would be market-positive.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.