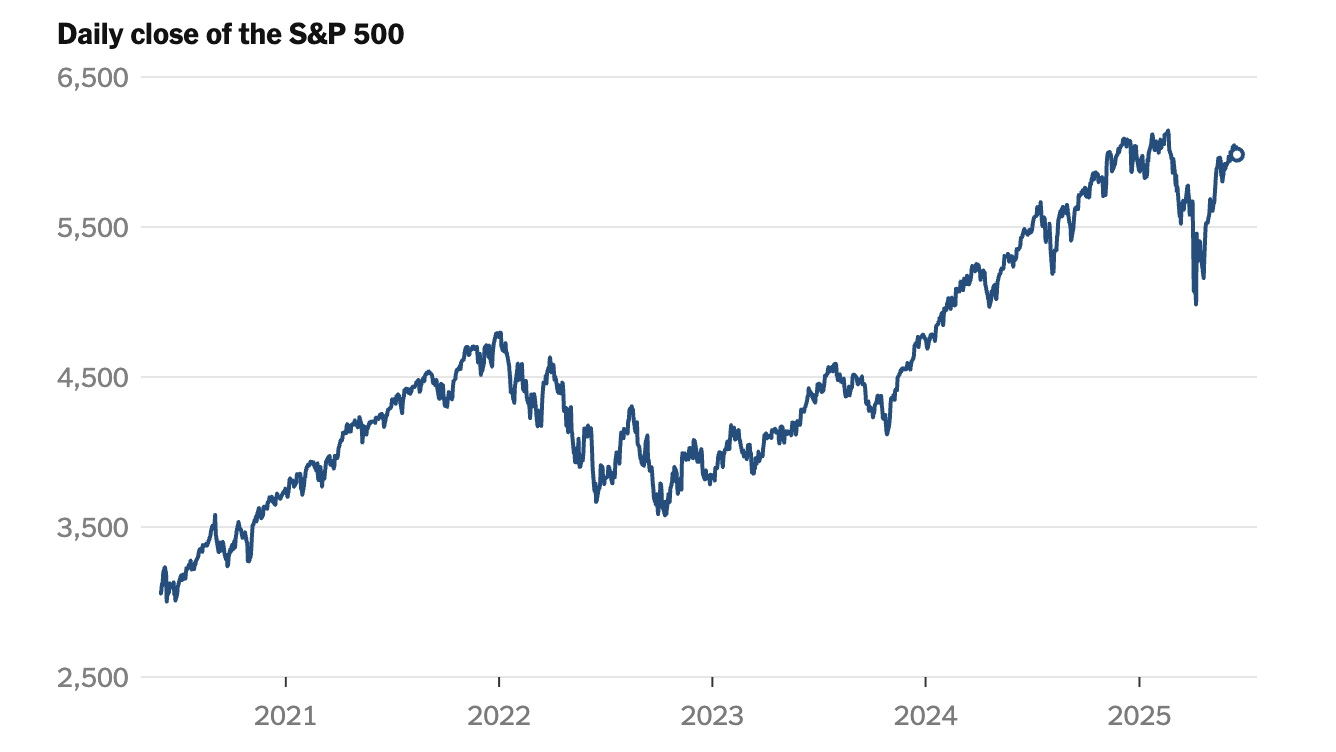

US markets rally as the S&P 500 eyes record high

Not long ago, it looked like global investors were finally cooling on their Wall Street obsession. After years of throwing cash at U.S. stocks, they started to look elsewhere. Between December and April, equity funds outside the U.S. hoovered up a record $2.5 billion - most of it in just three months.

Blame it on Trump’s tariff revival, or perhaps just good old Big Tech fatigue. Either way, the so-called smart money seemed to be giving America a breather.

But fast-forward a few weeks, and, surprise twist, the S&P 500 is striding back towards record highs, and foreign investors are piling in like they never left. So, what’s flipped the script?

Source: LSEG Data & Analytics, The New York Times

Global appetite returns: Risk is back on the menu

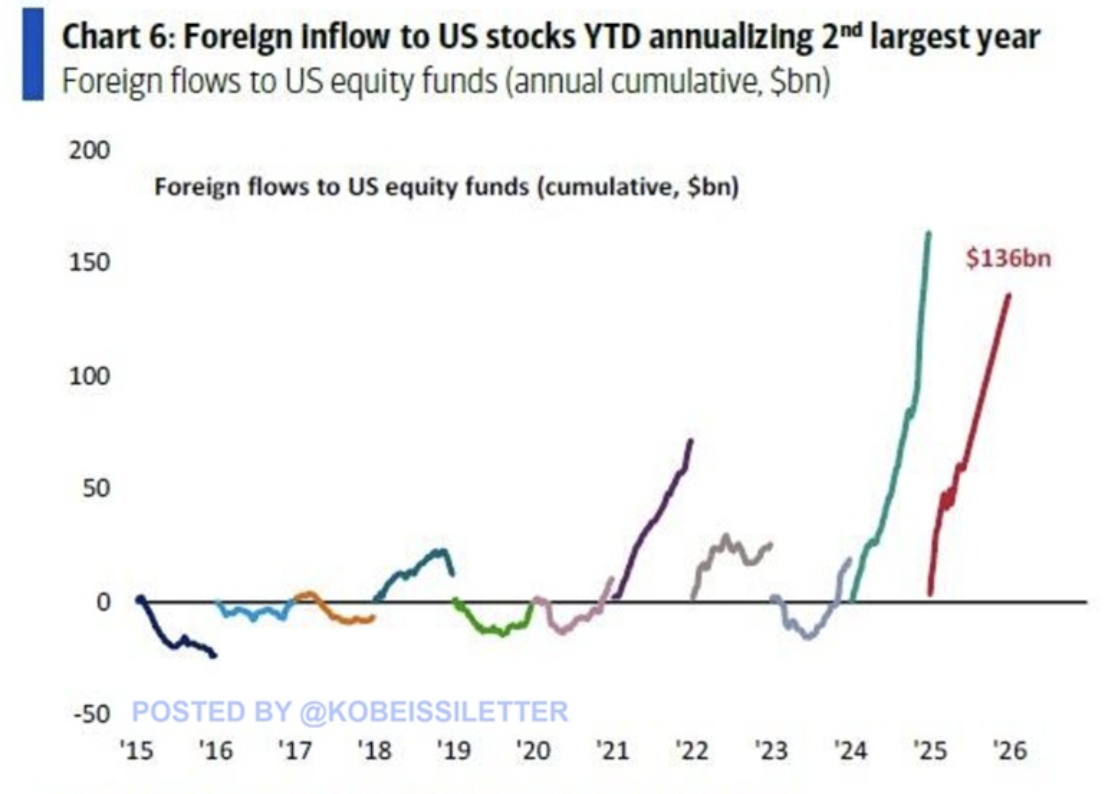

Bank of America reckons overseas buyers are on track to splash out $138 billion on U.S. assets this year - the second-largest total on record. And the lion’s share of that, $136 billion, is heading straight into equities.

Source: BOFA, Kobeissi Letter

Zoom out further, and the picture gets even bolder: since 2020, foreign investors have funnelled a staggering $547 billion into U.S. markets. About $350 billion of that has gone into stocks. For all the chatter about “diversifying away from the U.S.”, Wall Street clearly still has its charm.

So, what’s changed?

It’s not that the U.S. suddenly became flawless - it’s just looking like the least messy option.

While America wrestles with deficits, trade tensions, and political noise, it’s still faring better than much of the world. Europe is dragging its feet, China’s post-COVID recovery is losing puff, and emerging markets are battling inflation and currency swings.

Add in softer-than-expected tariff impacts and cooling inflation, and the U.S. starts to look - well, relatively steady. And when global investors get jittery, they usually fall back on what they know: big, liquid, familiar markets. That means American stocks.

The magnificent 7: Rally on slim shoulders

Here’s the catch - this rebound isn’t a team sport. It’s being driven by a very elite few.

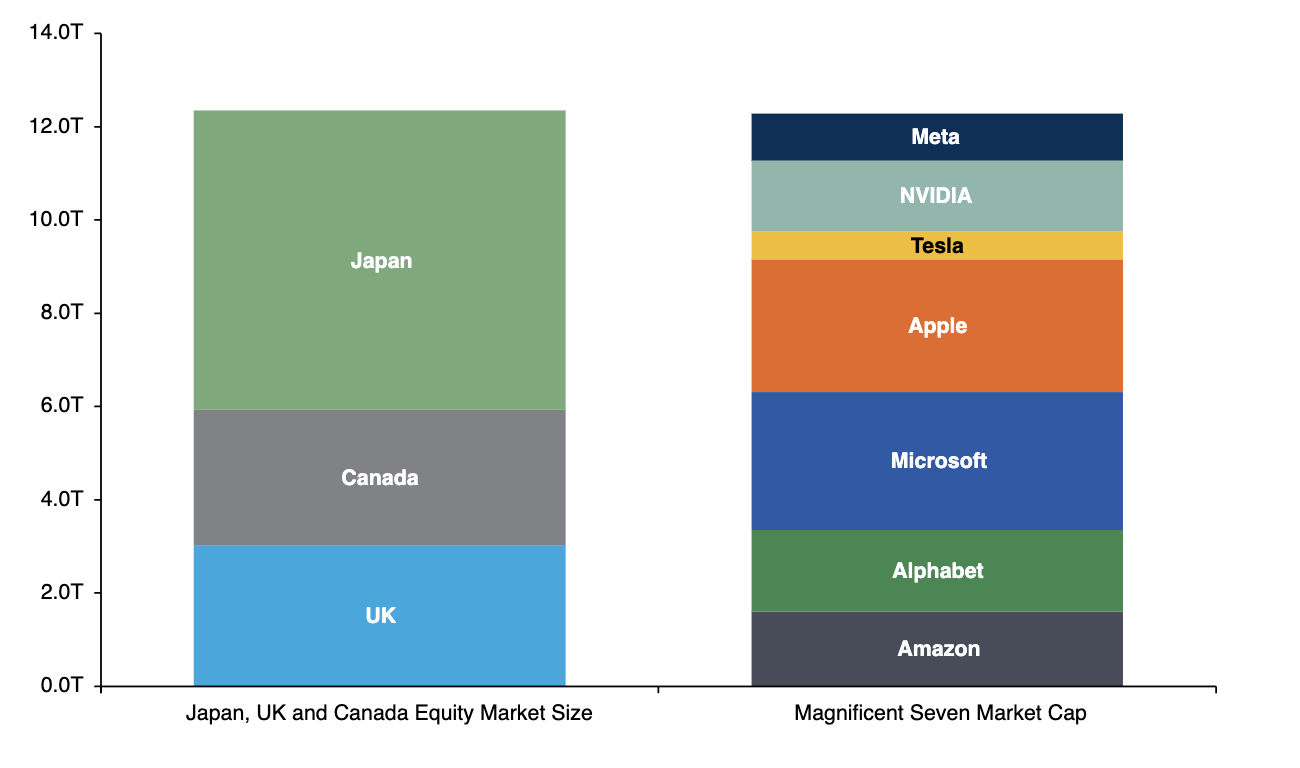

Take out the “Magnificent 7” (Microsoft, Apple, Amazon, Nvidia, Tesla, Meta, and Alphabet) and the rally loses its shine. Without them, the S&P 500’s gains since April would be nearly cut in half. These seven giants have grown so massive, their combined value now rivals the entire stock markets of the U.K., Japan, and Canada. Combined.

Source: Bloomberg

The equal-weighted S&P 500, where each company is given the same importance, remains nearly 5% off its peak. That tells us most U.S. stocks are still trailing behind. It’s the mega caps doing the heavy lifting.

This kind of concentration isn’t new, but it does crank up the risk. If even one of these tech titans stumbles, the entire index could feel the tremors. So really, this isn’t a sweeping vote of confidence in the U.S. economy - it’s a very specific bet on a few juggernauts.

Bond funds take a hit as investors chase growth

The return to equities isn’t just about what’s going in - it’s also about what’s being left behind.

U.S. bond funds have seen $43 billion in outflows recently, according to Morningstar. That’s a clear signal that investors are shifting from defence to attack. With the Fed keeping rates steady and inflation calming down, yields have stopped their climb. So, where to look for returns? Equities, especially tech, are looking tempting again, even with those lofty valuations.

S&P 500 outlook: Is this the real thing or a head fake?

So, is this a real resurgence or just another mirage? According to analysts, it depends on whether you see the glass as half full or strategically positioned beneath a leaky pipe.

On one hand, foreign capital is a powerful tailwind, and history shows that such inflows can fuel sustained rallies. But on the other hand, the market’s gains are disproportionately reliant on a few mega-cap stocks, and structural concerns, debt, geopolitics, and policy whiplash haven’t vanished.

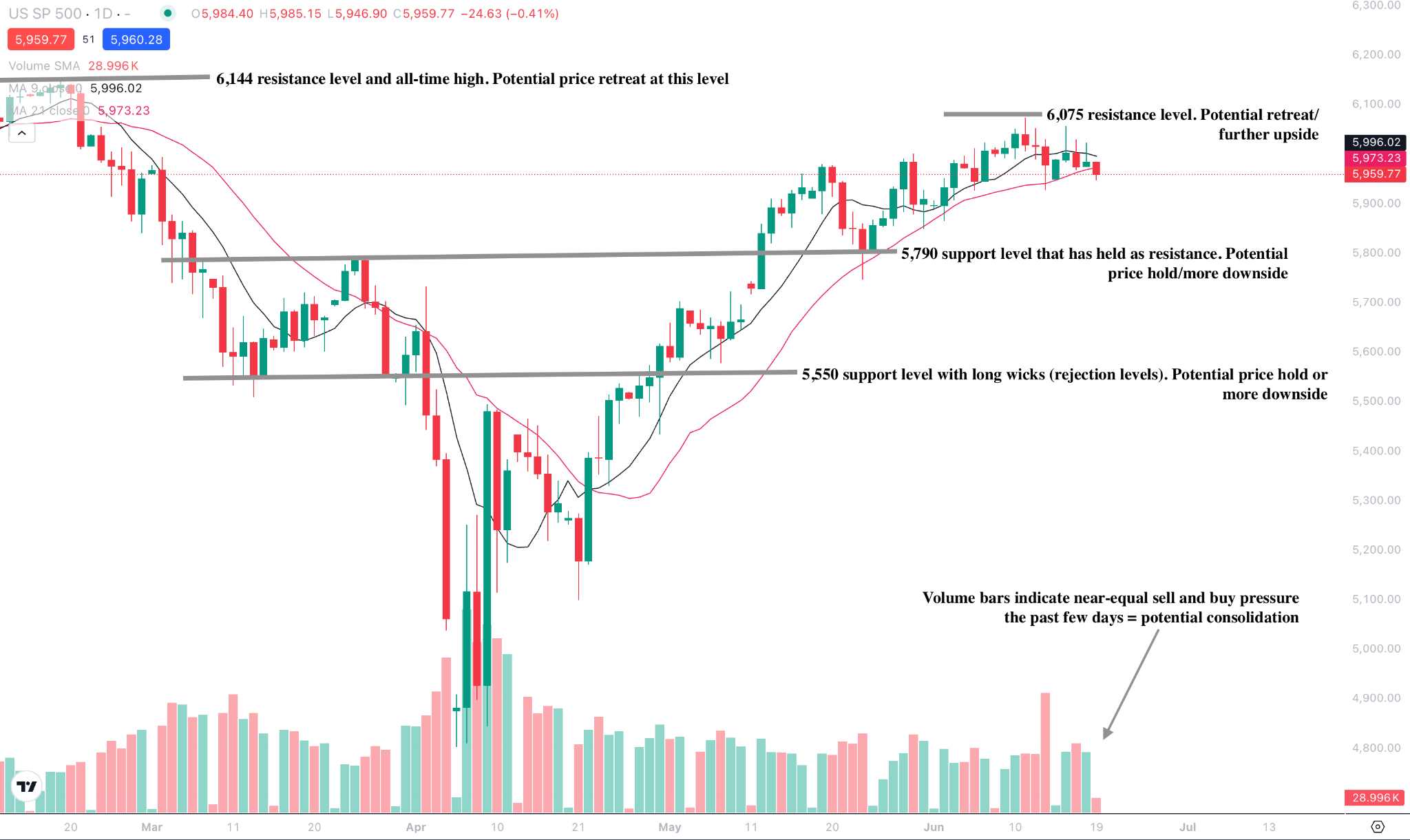

The S&P 500 has seen a significant retreat at the time of this writing. A downside bias is evident on the daily chart, though volume bars show almost even sell-side and buy-side pressures, hinting at potential price consolidation.

Should the S&P 500 see an uptick, prices could encounter resistance at the $6,075 and $6,144 levels. On the other hand, should the S&P 500 see a further slump, prices could be held at the $5,790 and $5,550 support levels.

Source: Deriv MT5

Is the S&P 500 going to break its record? You can speculate on US markets with a Deriv X and a Deriv MT5 account.

Author

Prakash Bhudia

Deriv

Prakash Bhudia, HOD – Product & Growth at Deriv, provides strategic leadership across crucial trading functions, including operations, risk management, and main marketing channels.