US-Iran talks buoy sentiment – Starmer throwing in the towel?

Weekend talks between US Vice President JD Vance and Iranian Foreign Minister Abbas Araghchi are the main driver of market sentiment this morning. Despite a shaky start on Sunday – with reports that Tehran was closing the Strait of Hormuz and President Trump renewing threats to strike Iran – the outcome was better than many had feared.

While specifics remain limited, a technical committee has been established to meet, helping to prevent future misunderstandings and to work towards a more concrete agreement. Lebanon, of course, remains a concern, but with the US and Iran sitting down to talk, this is positive and certainly better than the alternative.

Oil eases off its highs and Asian tech leads equities

On balance, oil benchmarks took the diplomatic thaw as their cue. Brent crude gave up earlier upside, now trading down 1.6% and back at the doorstep of the 200-day SMA and technical support at US$78.50. In equities, Asia-Pacific shares were largely positive overnight, bolstered by tech and semiconductor stocks. European equity index futures, however, are flat this morning, with US indices modestly on the front foot.

US Treasury yields are higher across the curve this morning, following Friday’s closure in observance of Juneteenth National Independence Day. In FX, the USD is moderately bid and continues to trade near levels not seen since May 2025, while the GBP is on the verge of refreshing YTD lows, which brings me to UK politics.

GBP at YTD lows ahead of an expected Starmer exit

PM Keir Starmer is widely expected to announce a timeline for his exit, possibly as early as today. This follows Andy Burnham’s by-election win in Makerfield last week, which secured a seat in Parliament. I think it is pretty much on the table that Burnham will replace Starmer. However, whether this will be a prolonged leadership challenge or whether Starmer will signal a coronation remains the question. This would also mark the 7th UK PM since the Brexit vote in 2016!

From a market perspective, of course, investors are in the dark for now, particularly about his plans for the UK’s fiscal framework and who will replace UK Chancellor Rachel Reeves. For now, the Gilt market has been relatively calm, with sterling on the brink of pencilling in fresh YTD lows.

Canadian inflation numbers on deck today

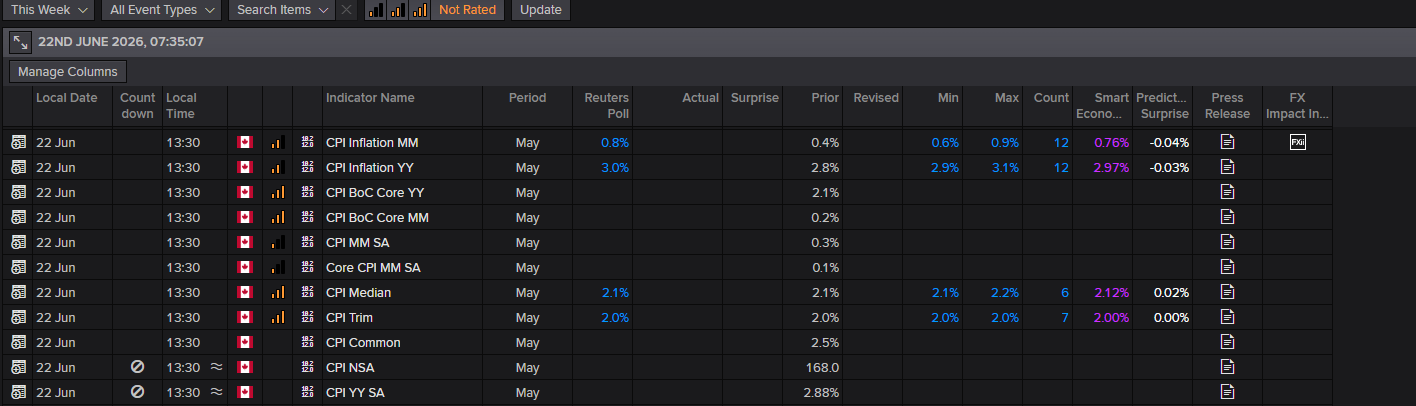

The May Canadian CPI inflation data hits the wires today at 12:30 pm GMT. Markets are pricing in 21 bps of BoC tightening by year-end, and I still think this is a little excessive. Canada’s GDP growth has stagnated, core inflation is around 2%, and the unemployment rate has been ticking upward since 2022 – fluctuating between 6.5% and 7.0% from early 2025. Consequently, a miss in the data could prompt investors to unwind some of the hawkish pricing.

Should the trim/median prints come in below 2% – as you can see from the LSEG calendar below, this would mean a print south of the market’s minimum estimates – even with an uptick in the headline (expected to reach 3% from 2.8% in April), this would align with BoC Governor Macklem’s comments about core inflation ticking down and would likely be enough for the BoC to look through any headline increase.

This, as I noted above, should lead to a dovish repricing in rate markets and may weigh on the CAD. Ultimately, because markets are pricing in a hike, a broad miss across the board will likely be the more targeted trade: CAD shorts.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,