US GDP shrinks, as imports surge, but it is not as bad as it seems

US GDP data was weaker than expected for last quarter. The US economy experienced a sharp slowdown, as expected, and growth contracted by 0.3%, vs. a 0.2% decline anticipated by analysts. However, the headline figure only tells us so much, digging a bit deeper into this report gives us a more rounded picture of the US economy.

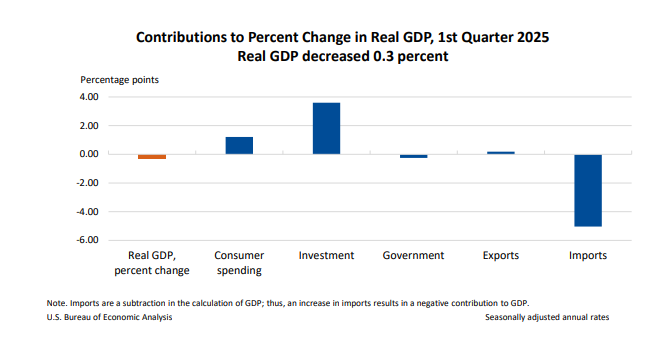

The biggest drag on growth was trade and lower government spending, according to the BEA. A surge in imports weighed on growth to the tune of 4.8%. This is the most on record and it suggests that the impact of US trade tariffs is impacting business behavior, with businesses front loading imports of goods to try and avoid reciprocal tariffs. However, the surge in imports also has some intricacies, which could blunt the negative impact of Q1 GDP. These include:

1, Slower headline GDP may not be a warning sign that a recession is imminent, since many of these imports will make their way into inventories, which can neutralize some of the effect of increased imports.

2, There could be a payback in future quarters from front-loading imports. Thus, we would expect import levels to decline in future, and bloated inventory levels to ease in the coming months.

3, A surge in imports of gold and silver. Gold that investors buy, and sell doesn’t enter the GDP calculation. As the amount of gold that was imported into the US surged in January, this was not included in the final GDP figure, although it is included in the import figures. Thus, the surge in imports is not all down to front loading of goods imports to avoid tariffs, although that did happen last quarter. The 5% drag on growth from imports is likely to be a one off, as gold imports are expected to return to normal down the line. The Atlanta Fed GDPNow model produce a gold adjusted GDP estimate, which they estimated to be -1.5% for Q1, vs. a -2.4% decline if gold imports were included. The Atlanta Fed model was too pessimistic on growth, as it often is, but it does highlight the technicalities of the way that GDP is reported.

The good news:

Not all of the GDP report was bad news. Fixed investment was a decent 1.3% for the quarter, and personal consumption was stronger than expected, rising by 1.8%, vs 1.2% expected. Real final sales to private domestic purchases, which is the sum of consumer spending and gross private fixed investment, increased by 3%, vs. a 2.9% growth rate in Q4. This suggests that the US consumer and investment is holding up in the face of uncertainty and stock market declines, even if it has slowed in recent months.

Will inflation fears persist?

However, inflation fears are now in focus after the price index for gross domestic purchases increased by 3.4% last quarter, compared with 2.2% rise in Q4, and the PCE price index rose by 3.6%, vs. 2.4% in Q4. Does this mean that companies and businesses are already putting up their prices in advance of the tariffs? If yes, then it could be a one-off adjustment. Many officials see tariffs as deflationary, since they can shrink demand over time. Thus, concerns about US inflation rates could be short lived, which may be why the bond market has not had a strong reaction to this report. Although US stock futures are falling on Wednesday, the dollar is maintaining its gains, which is another sign that the headline GDP figure does not paint a full picture about the outlook for the US economy.

Contributions to real GDP in Q1

Source: BEA

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.