US Fourth Quarter GDP Final Revision: No surprise for you

- Economic growth forecast for 2018 is expected to be above 3% for the first time since 2006

- Consumer and business sentiment remained strong through the fourth quarter

- Weak December retail sales are already included in Q4 calculations

The Bureau of Economic Analysis (BEA) of the U.S. Department of Commerce will issue its second revision of annualized 4th quarter GDP on Thursday, March 28th at 8:30 am EDT, 12:30 GMT.

Forecast

Gross domestic product is projected to decline to 2.4% in the fourth quarter from its prior estimate of 2.6%. The range of estimates is 1.9% to 2.7%.

The BEA normally issues GDP three times, the initial estimate followed by two revisions. Due to the partial government closure in late December and January, the BEA combined the initial and first estimate. This is the second and final GDP figure for the fourth quarter.

US Economy

Economic growth peaked in the second quarter at 4.2%, dropped to 3.4% in the third and 2.6% in the estimate in the fourth. The decrease has continued into the first quarter of this year with current projections from the Atlanta Fed running at 1.3% and the New York Fed at 1.29%.

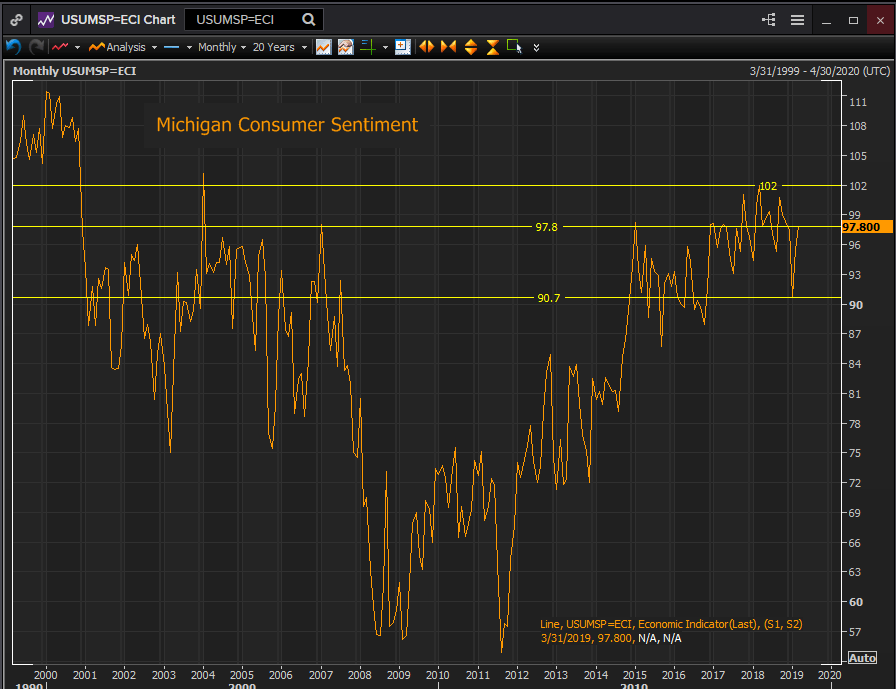

Consumer Sentiment

Consumer and business sentiment indicators declined in the second half of last year but remained strongly positive

The University of Michigan Consumer Sentiment Index peaked at 102.00 in March, had a second and lower top at 100.8 in September and slipped to 97.5 in December. The January plunge to 90.7 seems to have been shutdown-related with the recovery to 97.8 by March 2019 eliminating the January drop.

Reuters

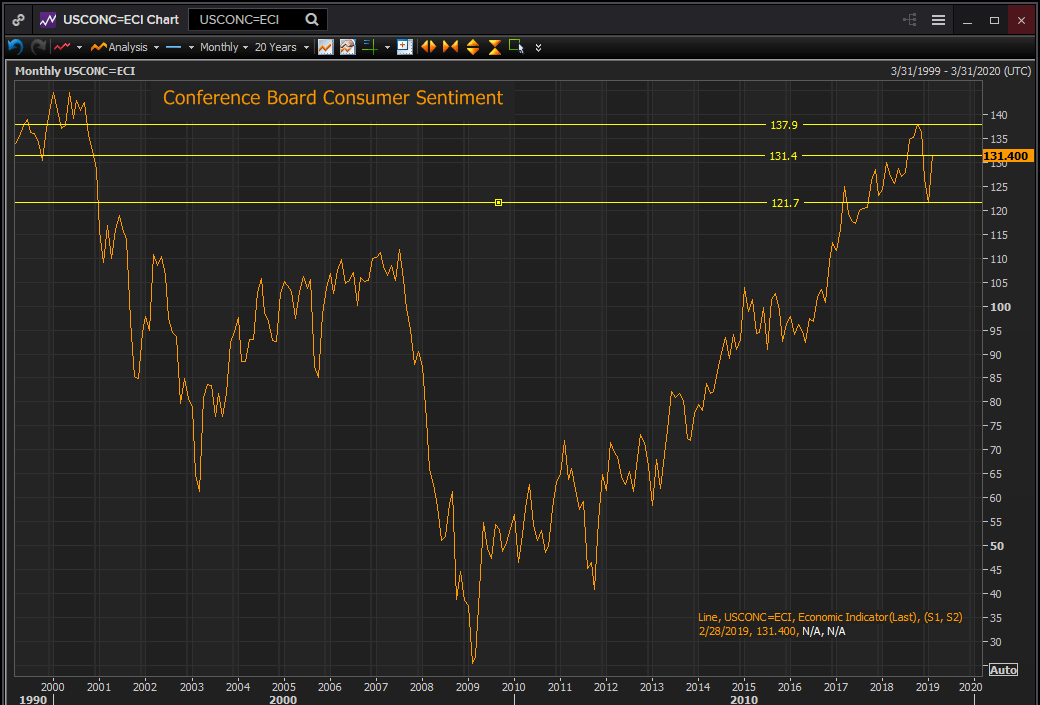

The Conference Board Consumer Sentiment Index reached 137.9 in October, an 18 year high, fell to 126.6 in December, 121.7 in January and then shot back to 131.4 in February.

Reuters

Fourth quarter averages for both consumer indexes were among the highest for the past twenty years. There is no indication in these results that the US consumer was disenchanted with the economy as the last quarter ended. That general satisfaction returned once politics in DC rectified the budget standoff.

Business Sentiment

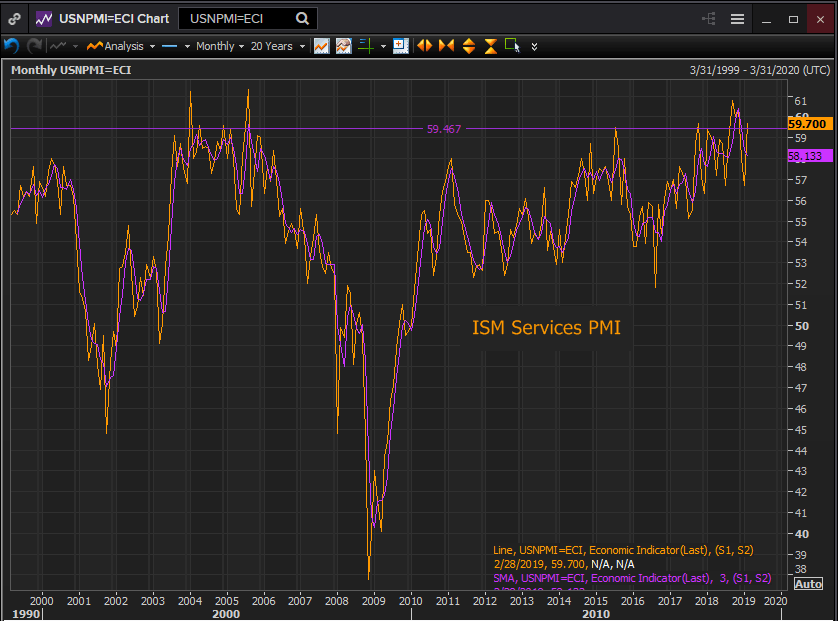

The purchasing manager’s indexes from the Institute for Supply Management showed continued strength in the fourth quarter.

The service sector PMI 3-month moving average for December of 59.467 puts it among the highest quarterly scores for the past two decades.

Reuters

Likewise, the 3-month average for manufacturing PMI of 56.867 is among the higher scores of the past twenty years, even if it is not in the same historical percentile as the service average.

Conclusion

Fourth quarter GDP is unlikely to provide any surprise in its final revision. The weak retail sales figures, though odd, are already incorporated into the BEA figure. Business and consumer sentiment remained buoyant throughout the quarter and such attitudes should not have produced anything unexpected in economic activity.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.