FOMC Preview: The Fed walks the interest rate tightrope

- No change expected in the fed funds or $120 billion in bond purchases.

- First economic and rate projections of 2021 will be a key focus.

- Fed must convince markets that its policies, unchanged in almost a year, are appropriate.

- Stronger economic forecasts will set the stage but Powell will try to rein in expectations.

- Federal Reserve has downplayed the economic threat of rising US Treasury yields.

- If Powell remains unconcerned on rates, the dollar and yields will rise

The contrast to the situation at the Federal Reserve meeting three months ago could not be greater.

“The world's fifth-biggest economy is heading back toward a shutdown as it grapples with its fastest increase in COVID-19 infections since the pandemic began," said the breathless Bloomberg story on December 3. The title was “California Warns of Lockdowns in Most of the State Within Days.”

By the December 16 Fed meeting California Governor Gavin Newsom had ordered most of the state closed.

Initial Jobless claims soared from 716,000 on November 27 to 892,000 two weeks later and would peak at 926,000 in the New Year. National payrolls were collapsing from 264,000 in November to -306,000 in December. Retail Sales sank 1.3% in November and 1% in December. The 10-year Treasury yield closed at 0.920% and the 2-year was at 0.119% after the Fed meeting.

When Federal Reserve governors reaffirmed the policies of the prior 10 months, a 0.25% upper fed funds target, and $120 billion a month in bond purchases, nothing in the economic or political landscape could gainsay their decision.

The economy seemed to need all the support the central bank could provide. Even the improved projections for GDP, to -2.4% in 2020 from -3.7%, and 0.2% higher in 2021 and 2022 to 4.2% and 3.2%, appeared wishful, based on the retreat of the pandemic which at that moment was expanding rapidly.

Economic reversal

Three months later the economic and pandemic situations have not only reversed but the next several quarters are set for a remarkable revival.

COVID-19 diagnoses in the United States have dropped almost 90%, hospitalizations and ICU usage are not far behind. Upwards of 20% of the US population has received at least one vaccine with more than two million people being inoculated each week.

Payrolls have turned on a dime, adding 545,000 jobs in January and February, more than twice as many as forecast. Unemployment Claims were down to 712,000 in the first week of March and are slated to drop below the old pandemic low of 711,000 in the next release.

Retail Sales jumped 7.6% in January and the Control Group rocketed 8.7%. Except for the bust and boom around the lockdowns, these are the largest monthly gains in more than a generation.

Even the subsequent declines in February of 3% for sales and 3.5% for control are less important than they seem. With a new stimulus payment of $1400 for most individuals already in the pipeline, more than double the $600 stipend that prompted the January surge, and the psychological relief from the end of the pandemic informing purchasing, consumption and the economy are headed for several very robust months.

The Atlanta Fed GDPNow model suggests that the economy will expand at a 5.9% annualized rate in the first quarter while Goldman Sachs recently raised its 2021 forecast to 7%.

These are, as the phrase goes, good problems for a central bank to have.

Markets

Markets have noticed and responded.

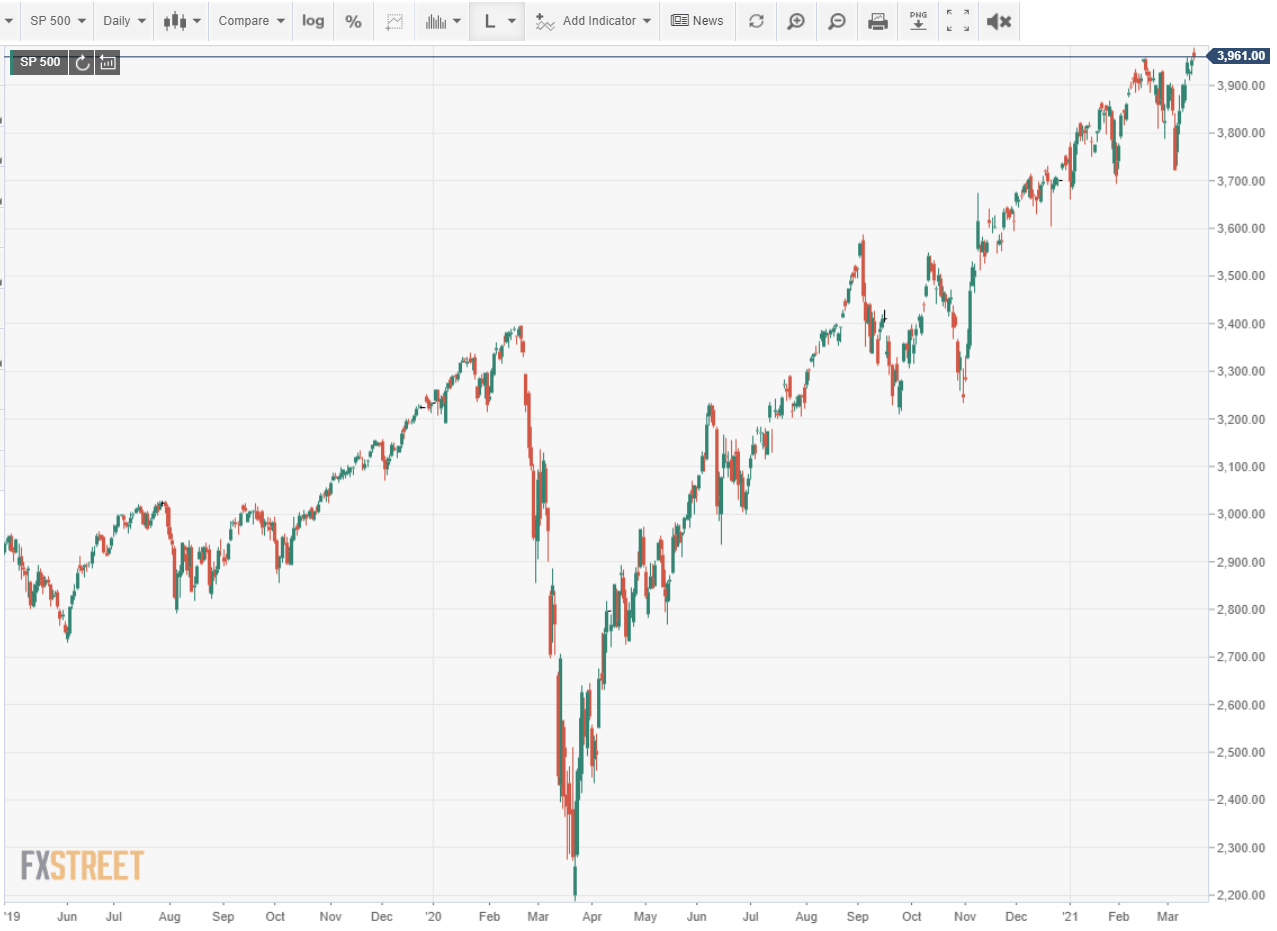

The major equity averages, led by the Dow and S&P 500, are at or near their all-time records.

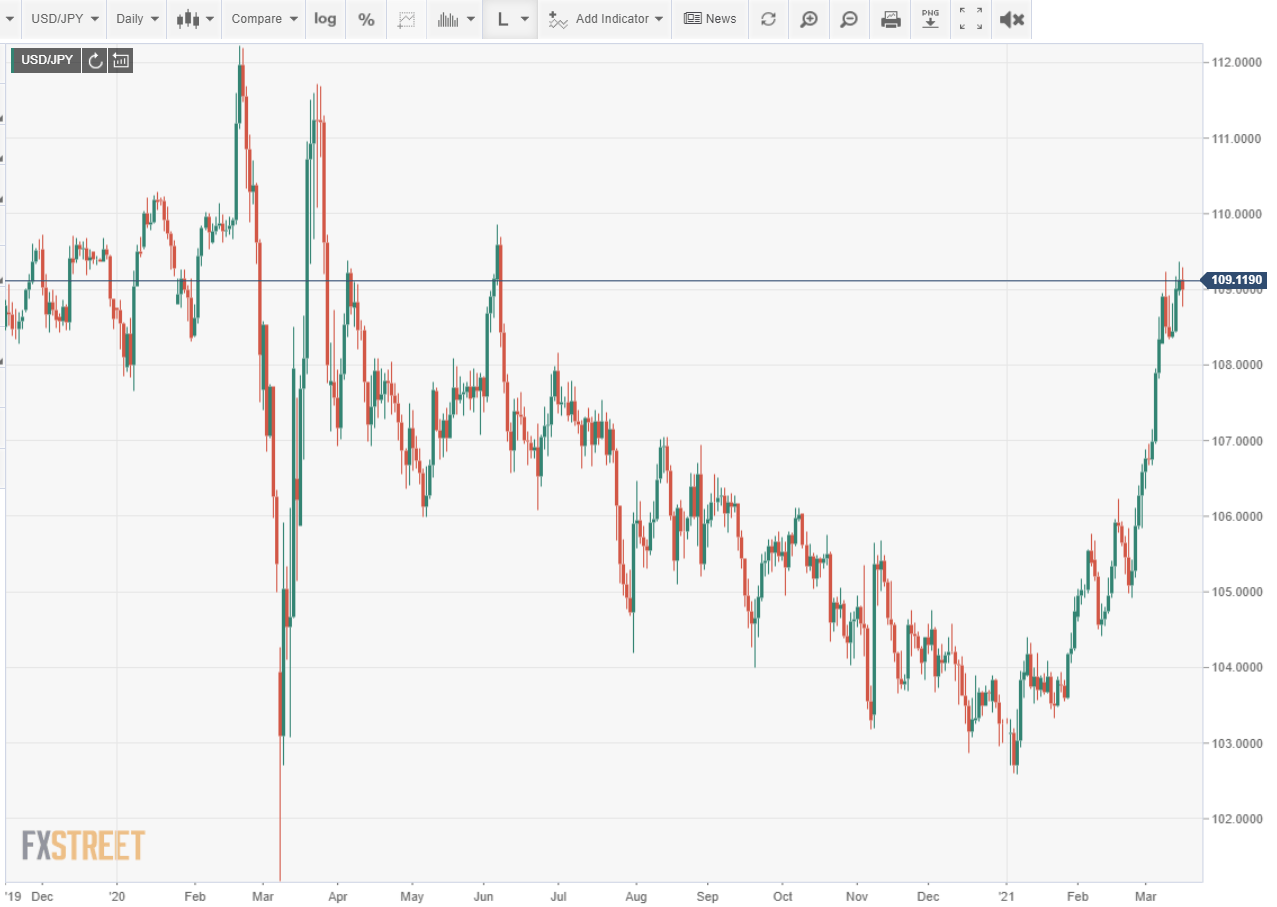

The dollar has recovered a portion of its losses against the euro and more versus the yen, propelled by a sharp surge in interest rates in the middle to long end of the Treasury curve.

The yield on the 10-year bond has gained 71 basis points from 0.92% at the close of the December 16 FOMC to 1.63% on Tuesday. The 30-year or long bond has added 72 points to 2.39%.

US 10-year Treasury yield

CNBC

Federal Reserve Policy

Since the December meeting the economy has been granted the fiscal help Chairman Jerome Powell repeatedly requested. Congress has approved two stimulus packages totaling nearly $3 trillion.

With most of the country reopening, employment recovering and demand ready to rocket with wages, the wave of liquidity rolling through the economy has established the classic conditions for a bout of inflation.

When the January Producer Price Index more than doubled to 1.7%, speculation was intense that consumer prices were next.

Monday March 10, two days before the February CPI release, the 10-year yield hit a pandemic high at 1.613%. The Treasury was auctioning $38 trillion of 10-years bonds on Wednesday afternoon after the CPI report in the morning.

In fact, the February inflation report showed little impact with the headline rate at 1.7% as expected and the core slightly lower at 1.3% from 1.4% in January. The average yield at the auction was 1.523%, about where it was at the beginning.

Despite the rapid rate increases, Chairman Powell has been sanguine about the rise of Treasury rates, saying that he does not think the gains will undermine the current recovery or its prospects through the year. The Fed has given no hint that it might use its monthly purchases to bring down longer-term rates.

Economic projections

The Fed's December projections which posited 4.2% growth this year, a 6.7% unemployment rate in December 2020 and 5% at the end of 2021 are already out of date and should see substantial upward revision.

Chairman Powell noted in Congress two weeks ago that GDP could average 6% for the year and that is a likely estimate for growth with unemployment between 4.3% and 4.8%.

The fed funds rate projection will be unchanged through the end of 2023.

Inflation averaging, the bank's new hands-off approach that permits increases to run above the 2% target for as long a necessary to meet the price goal, has essentially removed the fed funds rate from credit market consideration.

Combined with the $80 billion of Treasury purchases concentrated in the short end of the curve, the 2-year yield has been almost stationary, gaining just three basis points to 1.151% since the December 16 FOMC.

Conclusion

Credit and equity markets think the US economy is headed for a robust recovery. The Federal Reserve does also.

But the governors do not want speculation about the recovery or about the inflationary potential of the stimulus debt, especially in Treasury yields, to impede the actual economy.

The economic and rate estimates of the Projection Materials are the first indication of Fed policy but the majority of the explanation will be in the speech and answers of Chairman Powell at his news conference.

He must convince the markets that the brightening economic picture will not provoke a change in policy and that the bank is vigilant on inflation.

Yes, might be his message, things are getting better, faster than we had imagined, but there is still a great deal of uncertainty, not the least over the pandemic and its potential to again derail the economy.

It will be a tricky piece of rhetoric, but the markets are primed for good news and Mr. Powell has been the bearer of welcome tidings before.

The Race for Employment in 2021: US job market is the key for the US dollar

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.