US economy in good position to weather Omicron storm

While the Omicron wave is likely to temporarily weaken US growth, the first data releases of 2022 suggest the economy is fundamentally very strong with robust growth and inflation keeping the Federal Reserve on course for rate hikes.

ISM points to a robust manufacturing sector

We have had the first big data US releases to start the year and while they are a little softer than hoped at the headline level the details show an economy that was in great shape in the lead up to the holiday season.

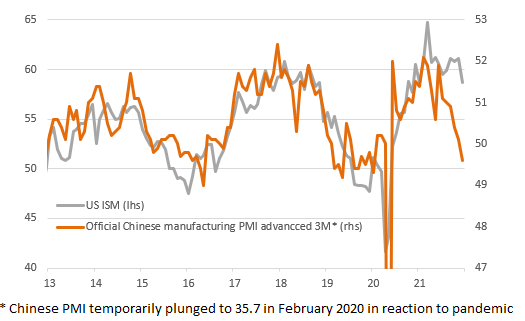

Firstly, the ISM manufacturing index dropped to 58.7 from 61.1 whereas the consensus was for a slightly stronger 60.0 figure with optimism largely centered on good regional indicators. However, the details are certainly stronger than the headline implies since there were only very modest declines in production and orders while employment actually rose to 54.2 from 53.3 and the backlog of orders increased to 62.8 from 61.9 – remember anything above 50 is in expansion territory. There doesn’t appear to be much to worry about from a demand perspective in the economy. Moreover, the chart below shows how well the US is performing relative to China’s PMI.

US manufacturing outperforming China's (ISM & PMI readings)

Source: Macrobond, ING

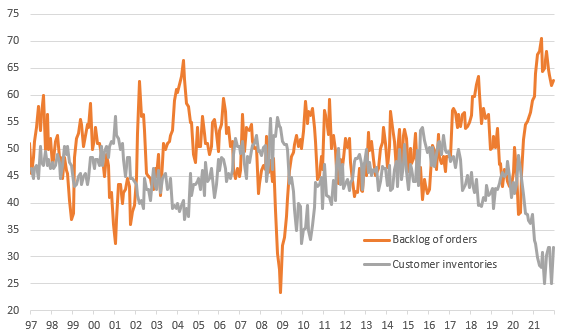

Lower for good reasons

Instead, the headline index was dragged down by a big drop in supplier delivery times (64.9 from 72.2) – which in these current stressed times is actually a good thing as it hints that supply chain bottlenecks might be easing. A modest improvement in customer inventories (although still at very weak levels that are deep in contraction territory at 31.7) backs this up. Certainly a better story than just looking at the headline implies.

Prices paid also fell sharply (68.2 versus 82.4) – a positive – but the issue of strong demand versus a lack of supply means that manufacturers continue to have pricing power. A massive backlog of orders at a time when you know your customers are desperate – as indicated by contracting customer inventories – means that price pressures will remain elevated for some time.

Corporate pricing power persists

Source: Macrobond, ING

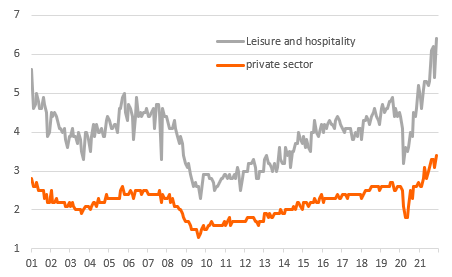

Private sector quit rate hits new high

Meanwhile, the Job Openings and Labor Turnover Survey data show the number of US job openings dipped to 10.53mn from 11.1mn (consensus 11.1mn), but this is still showing a huge number of vacancies in the US with the softness in employment growth clearly down to a lack of available workers rather than any weakness in demand for staff.

Again the details show a stronger economic story with a record 4.5mn people quitting their jobs in November. This is equivalent to 3% of all workers quitting to move to a new employer, which takes us back to match the series high for the 21-year survey. For private-sector workers, it did hit an all-time high of 3.4%.

US quite rates - proportion of workers quitting their jobs to move to a new employer (% of workers)

Source: Macrobond, ING

The Fed is watching and rate hikes are coming

This survey has taken on added importance since the December FOMC. When asked at the December FOMC press conference about the best signals surrounding maximum employment, Chair Powell responded “the quits rate is really one of the very best indicators… because people quit because they feel like they can get a better job and there's, you know, record amounts, historically, high levels of that going on suggesting, again, that you've got a very tight labor market."

The Omicron wave remains an obvious concern and is likely to see some consumer caution, while increased worker absences mean more bottlenecks and supply chain strains. Nonetheless, there is optimism that the health impact and economic disruption may be less intense and lasting than for the Delta wave. Today’s data shows the economy is in a good position to weather it and will keep market expectations for at least three rate hike expectations in place for this year.

Read the original analysis: US economy in good position to weather Omicron storm

Author

James Knightley

ING Economic and Financial Analysis

James Knightley is the Chief International Economist in London. He joined the firm in 1998 and has been covering G7 and Western European economies. He studied economics at Durham University, UK.