US economic outlook: April 2026

Summary

Introducing the Monthly Macro Bullet Points:

Oil shock revives consumer inflation, delays Fed easing

- Geopolitical disruption has turned into a near‑term inflation shock. The ongoing Iran conflict has pushed oil prices higher, lifting headline inflation, eroding real income and spending, and delaying the timing of Fed easing in our forecast.

- March consumer inflation will break disinflation. Higher energy prices will feed quickly into prices at the pump, ending the two‑year disinflation trend. With oil staying elevated and no clear resolution in the Middle East, we expect firmer inflation, with headline PCE peaking at a year-ago pace of 3.7% in Q2 and remaining sticky in a 2.7–3.1% range through year‑end.

- Consumer spending is resilient but looks shaky. While spending has so far absorbed higher gas prices, we expect a more visible hit over the next month as energy costs spill into other categories. Households will increasingly prioritize expenditures on gas and food, crowding out discretionary demand and slowing overall consumption. We now see real personal consumption expenditures rising 2.0% on average this year, softer than previously expected.

- Income growth was already cooling before the energy shock. Real income excluding transfers has slowed over the past year as job growth moderates. Looking through labor strikes and volatile weather, private hiring found some sense of stabilization in the first quarter. But we still expect further softening ahead amid geopolitical uncertainty and AI‑driven efficiency gains, keeping downward pressure on wage growth ahead.

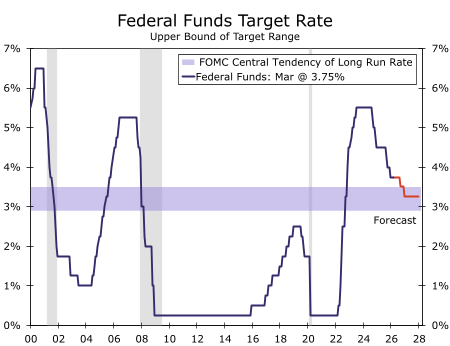

- Policy trade-offs point to prolonged Fed patience. With inflation re‑accelerating and labor markets still gradually cooling, the Fed’s dual mandate is pulling in opposite directions.TheFed will exercise an abundance of patience as a result, and we have pushed out the start of easing but still expect 50 bps of total cuts this year, now penciled in as 25 bps moves at the September and December FOMC meetings.

Source: Federal Reserve Board and Wells Fargo Economics

Author

Wells Fargo Research Team

Wells Fargo

More from Wells Fargo Research Team