US CPI data unlikely to ease sticky inflation worries, but will markets care?

-

US CPI inflation expected to have ticked up in March.

-

But markets may shrug it off if core figure inches lower.

-

Data due at 13:30 GMT, Wednesday, will be followed by FOMC minutes at 18:00 GMT.

Will CPI report boost rate cut bets?

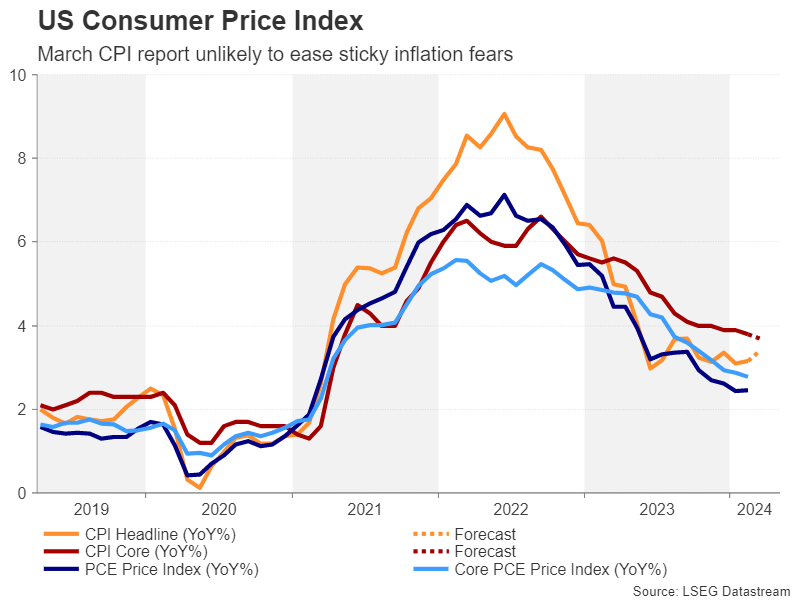

Inflation data according to the CPI and PCE measures have started to diverge lately, clouding the outlook just as the Fed seeks more clarity on where prices are headed. Headline CPI has persisted above 3.0% since last summer, while core CPI has been declining at a snail’s pace.

It’s a somewhat more favourable trend when looking at the personal consumption expenditures (PCE) metric that the Fed prefers to focus on. The headline PCE price index rose marginally to 2.5% in February, but core PCE eased to 2.8%.

But for the consumer price index, there probably wasn’t much of a convergence in March. The yearly headline rate of CPI is expected to have edged up to 3.4% in March from 3.2%, with the month-on-month rate moderating to a 0.3% pace from 0.4%. Core CPI is also expected to have fallen slightly, both on a monthly and annual basis, expected at 0.3% and 3.7% respectively.

June rate cut no longer a done deal

Whilst such figures would not necessarily raise any alarm bells, neither would they calm fears about inflation bottoming out before reaching the Fed’s 2% target. But for the moment, Fed officials remain optimistic that inflation will decline further in the coming months, allowing it to cut rates at some point in the second half of the year. It’s unlikely that the minutes of the March FOMC meeting will sway much from this message.

The expectation that one way or another, rates cuts are coming, and that the US economy will almost certainly avoid a recession is what has negated the disappointment from the fading bets for a June rate cut.

The odds for a 25-basis-point cut in June have been scaled back sharply in recent weeks, and even more so after Friday’s bumper payrolls report. Markets are evenly split on the odds of the Fed beginning its rate cutting cycle in June, compared to it being almost fully priced in a few weeks ago.

Markets hopeful inflation will fall

The US dollar has been in a broad uptrend this year as investors have been repeatedly forced to re-evaluate the timing of Fed easing. Yet, there’s still a tendency to put more weight to the soft indicators than the hot data and this is keeping a lid on dollar gains.

For example, the drop in the ISM services prices paid index more than offset the impact from the jump in manufacturing prices days earlier as well as hawkish commentary from Fed officials during the week. Meanwhile, cooling wage pressures in the March NFP numbers were enough to keep jitters over accelerating jobs growth to a minimum.

A goldilocks economy

To be fair, the notion that the US labour market can continue to grow without fuelling faster pay increases is not entirely unreasonable amid the influx of migrants into the country that is boosting the supply of labour and thus meeting the rise in demand.

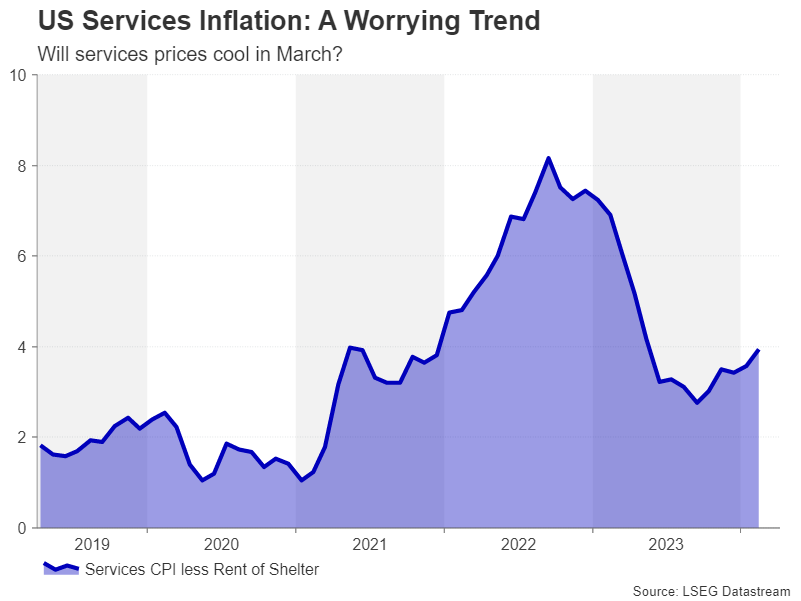

But even if this goldilocks scenario can last, solid consumer demand on the back of the tight labour market will be a hindrance to getting inflation down all the way to 2%, particularly for services inflation. CPI less rental costs edged up to 3.9% in February, having reversed from a low of 2.8% last September. If the decline in the ISM services price gauge translates to a softer reading for the CPI component as well, that could be enough to sustain the current positive sentiment in the markets even if the headline figure ticks higher.

However, if either or both the core and services CPI prints are stronger than forecast in March, the upbeat mood may fade, lifting the dollar, but weighing on Wall Street.

Optimism keeps a check on Dollar gains

The dollar index appears to be forming a double top around the 105.00 region, so this level is likely to be tested again if the CPI numbers are hotter than expected. But holding above the 50- and 200-day moving averages (MA) at 103.94 and 103.81, respectively, is crucial to maintaining the positive bias. So, a surprisingly weak CPI report could pull the dollar index below its MAs, tilting the near-term risks to the downside.

Overall, it’s striking how well risk appetite has held up even as investors have started to price out the third expected rate cut for 2024. The soft-landing narrative seems to be slowly evolving to one of US exceptionalism, whereby the American economy keeps outperforming its peers. It remains to be seen whether the risk rally can survive rate cut hopes being dimmed any further.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics.