US Business and Consumer Sentiment: No need for revival

- Consumer and business sentiment have returned to near pre-shutdown levels

- Consumption and business investment surged in February

- Weak Q1 GDP estimates should improve with the quarter

The partial closure of the Federal government for most of January was the biggest news story of that month. The non-stop coverage in old and new media had a short-lived negative effect on consumer and business sentiment.

Its impact however on the decisions made by business managers and consumers was nil. The January shutdown presented no reason for business managers and households not to spend as their needs and interests dictated.

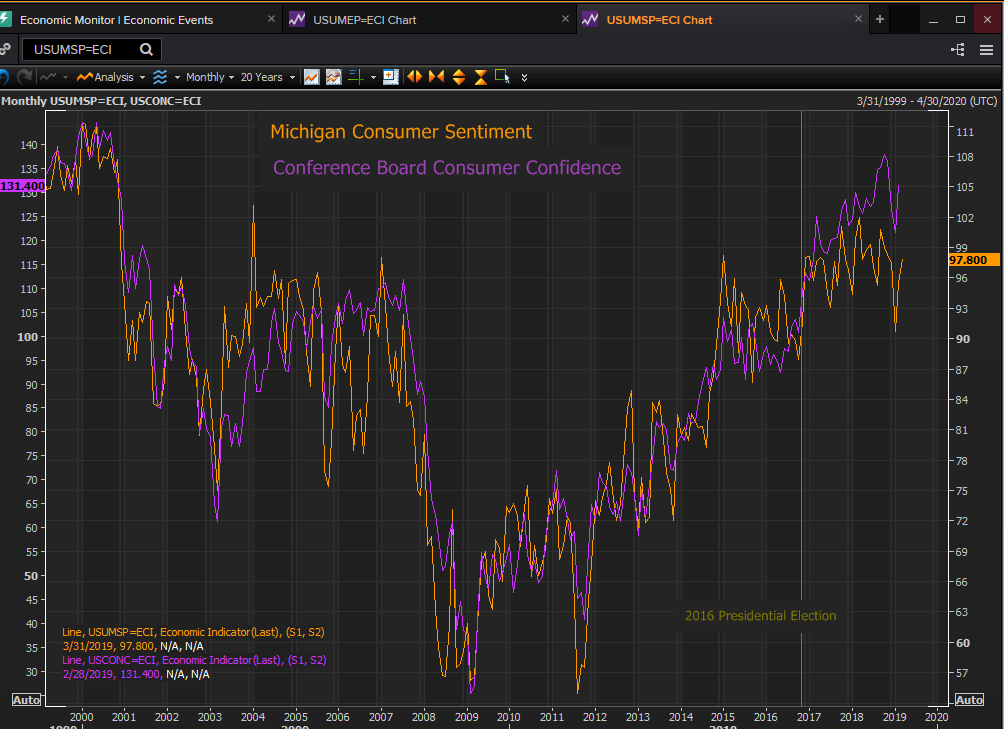

Consumer Sentiment

Consumer attitudes were declining from their peaks before the government closure. The Conference Board eighteen year high of 137.9 was in October. In December it was already more than 10 points lower at 126.6. The bottom in January of 121.7 reversed quickly the next month to 131.4.

The results of the Michigan Survey were nearly the same. September scored 100.8, in December that dropped to 97.5, shutdown month skidded to 90.7 and February rebounded to 97.8 .

Uncertainty over the length of the government shutdown during the survey period in the early part of January likely contributed to the sharp drop in the consumer outlook that month. Yet even in January readings from both surveys remained among the highest in the post-recession decade. If the US consumers were truly worried about the government closure they kept it to themselves.

Reuters

Business Sentiment

Purchasing managers indexes in manufacturing and services from the Institute for Supply Management peaked in the second half of last year and were falling before budget politics hit Washington.

The low on the service side at 56.7 coincided with the shutdown in January but February’s revival to 59.7 brought sentiment to the upper part of the range of the last two years, just below the September high of 60.8.

The bottom in manufacturing was in December at 54.3 followed by a return to 56.6 in January not far from the November score of 58.8 and followed by a drop to 54.2 in February.

Reuters

Retail Sales

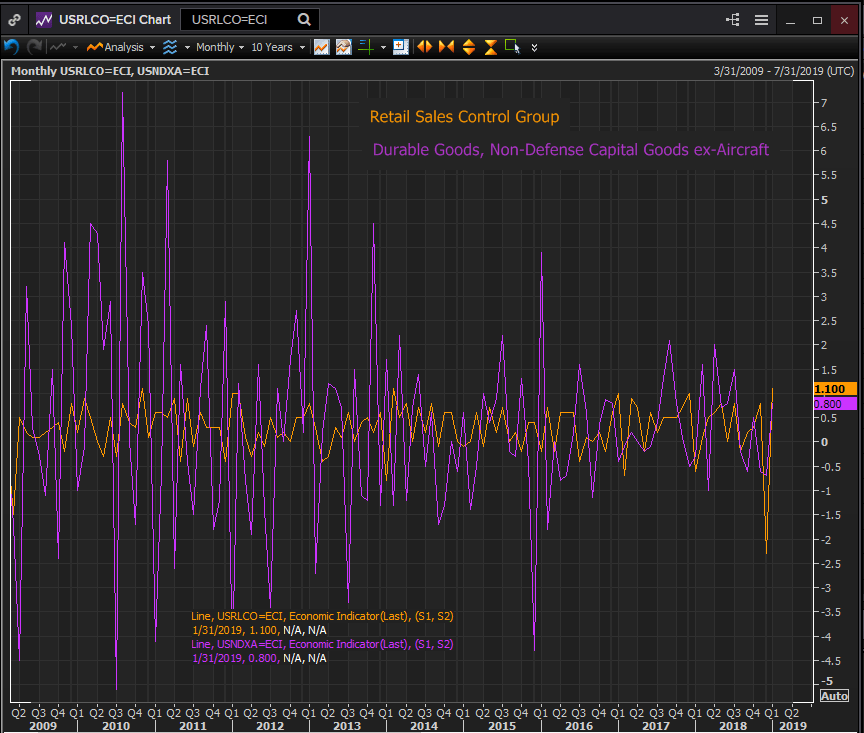

The plunge in the retail sales figures reported by the Census Bureau in December in what was by most private accounts a fine holiday season is still a bit of a mystery. From a strong 0.8% gain in November the control group, which is used by the government to calculate GDP, plunged 2.3% in December a worse fall than at the depth of the financial crisis and recession. The revival in January at 1.1% was the largest gain since February 2014.

Durable Goods Business Investment

The durable goods category, non-defense capital goods ex-aircraft is used as a proxy for business investment spending. It is not a contributor category to the GDP analysis but is an oft-cited substitute for the investment component.

After a strong year from mid-2017 to mid-2018 investment purchases fell in four of five months from August through November last year. The sharp gain of 0.8% in January, the shutdown month was an indicator that despite the prior pullback in expenditures business managers were still actively pursuing expansion in line with their plans for this year.

Reuters

End of the Shutdown Blues

The much hyped consumer and business effect of the shutdown and Washington politics on the economy turned out to be a very minor affair.

Consumer and business sentiment had been slipping from multi-year highs before the closure began. While there may have been some impact in the amount of the January decline, February’s return erased any lingering damage.

Business sentiment involving as it does longer lead times in product cycles started declining earlier in late summer after its best period in a dozen years. The recovery in service sector sentiment brings it back to a level of robust growth. The February fall in the manufacturing index, though still securely in expansion, may indicate building concerns among factory managers for economic growth, it may note concerns over trade, or it may be the back and forth in sentiment within normal economic expansion.

The strongest indicators of continued US growth and the irrelevance of the shutdown to economic activity are the consumer spending and business investment numbers from January.

Consumption saw a sharp recovery from December and business spending reversed two prior negative months. As these trends go so goes the economy.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.