United States: Money supply slumps

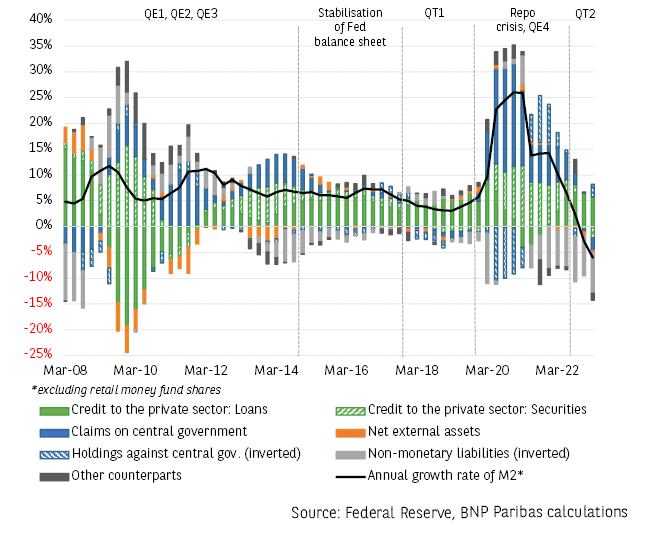

In March 2023, the M2 measure of money supply contracted for the fifth consecutive month in the United States (-4.5% over one year). The identification of the main sources of monetary creation/destruction reveals the impact of the restrictive monetary environment and the resulting trade-offs.

First, the credit channel (green histogram), the traditional engine of deposit creation, has been weakening for several months (tighter lending criteria and lower demand for bank loans). Second, US households are largely subscribing to new issues of Treasury debt and mortgage-backed securities, so that the Fed’s balance sheet reduction (Quantitative Tightening, QT) is destroying some of the bank deposits created by the latest quantitative easing (QE) (blue and hash green histograms). The tightening of monetary policy is also conducive to an expansion of commercial banks’ long-term resources (grey histogram): term deposits and secured loans (advances) from the Federal Home Loan Banks (FHLB). Finally, the Fed’s repurchase agreements with money market funds (Overnight Reverse Repo Facility), in return for generous remuneration, continue to sterilise part of the money previously created (grey histogram). In March, fears about the soundness of some regional banks led to the flight of USD 400 billion in cash from deposit accounts to shares in money market funds, which are better paid. However, 80% of these resources were “lent” by the funds to the Fed or invested in FHLB debt securities, and thus ultimately sterilised or converted into long-term bank debt through advances, thereby reducing the money supply.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.