UK’s surprise GDP contraction not quite as bad as it looks

Unsurprisingly, the ending of free Covid testing in March means April's UK GDP figures look worse than they are. The Bank of England will be focusing more on how bad the consumer story could get in coming months, but the recent announcement of extra government support should help insure against a consumer-led recession.

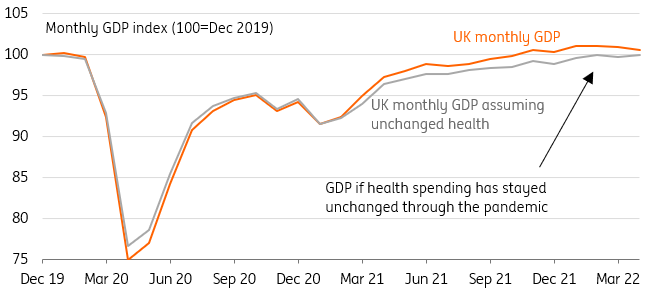

April’s UK GDP figures were always going to look worse than reality. Free Covid-19 testing stopped the previous month and according to the ONS that meant there was a 70% fall in test and trace activity. Pandemic-related health spending shaved a full 0.5 percentage points off GDP growth in April. And if we strip that out, the headline 0.3% decline in monthly GDP should actually have been marginally into growth territory.

In short, just as health-related spending gave the level of GDP an artificial boost last year, helping the economy appear to recover to pre-virus levels more quickly than it actually had, these categories are now making the picture look superficially worse.

UK monthly GDP has been virtually flat once volatile health spending stripped out

Source: Macrobond, ING

Elsewhere, the story is mixed – a rise in new car registrations was offset by falls in manufacturing and construction, and in the case of the former, this was the third consecutive month-on-month fall.

When you throw in the impact of the extra bank holiday a couple of weeks ago, we’re likely to get a negative growth figure for the second quarter overall, probably in the region of -0.5%. That’s a fair bit below the Bank of England’s 2Q forecast, though given the highly artificial nature of the undershoot, it’s questionable how fazed policymakers will actually be.

The bigger question in their minds will be how bad the consumer situation is likely to be through the rest of the year. Confidence is at all-time lows, and we’re starting to see an impact in the retail figures. Then again, the jobs market remains tight and given the widespread labour shortages, we think the bar for firms to make widespread redundancies in the face of lower demand is higher than usual. Assuming employment remains solid, and factoring in the recent government support package, we think a consumer-led recession may be avoided – though ultimately a lot depends on whether we get another leg higher in wholesale energy prices this autumn.

The arrival of extra government support probably means the Bank of England will again unanimously vote to hike rates again this Thursday, though we think the committee overall will come down in favour of another 25bp hike over a faster 50bp move.

Read the original analysis: UK’s surprise GDP contraction not quite as bad as it looks

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.