UK wage growth Preview: Accelerating wages are set to support Sterling

- The average weekly earnings excluding bonuses are expected to accelerate to 2.9% y/y in three months to March while still rising above 2.5% inflation.

- On the other hand, the average weekly earnings including bonuses are decelerating to 2.7% y/y.

- The UK unemployment rate is expected to remain steady at 4.2%, the lowest level since 1975.

- With UK wages rising well above inflation rate the GBP/USD is set to rebound higher after the recent selloff.

The UK average weekly earnings excluding bonuses are expected to accelerate to 2.9% over the year in three months to March while wages including bonuses are seen rising 2.6% over the year, the Office for National Statistics is likely to say on Tuesday. The average weekly earnings both excluding and including bonuses rose 2.8% over the year in the previous period while coming out slightly below expectations in three month period to February.

The unemployment rate is expected to remain steady at 4.2% stuck to the lowest level since 1975. The claimant count is expected to rise 7.5K in April compared with 11.6K in the previous month.

Should market expectations prove correct and the average wage growth excluding bonuses will rise further towards 3.0% annual growth and the unemployment remaining steady, Sterling should be well supported after the recent streak of falling lower.

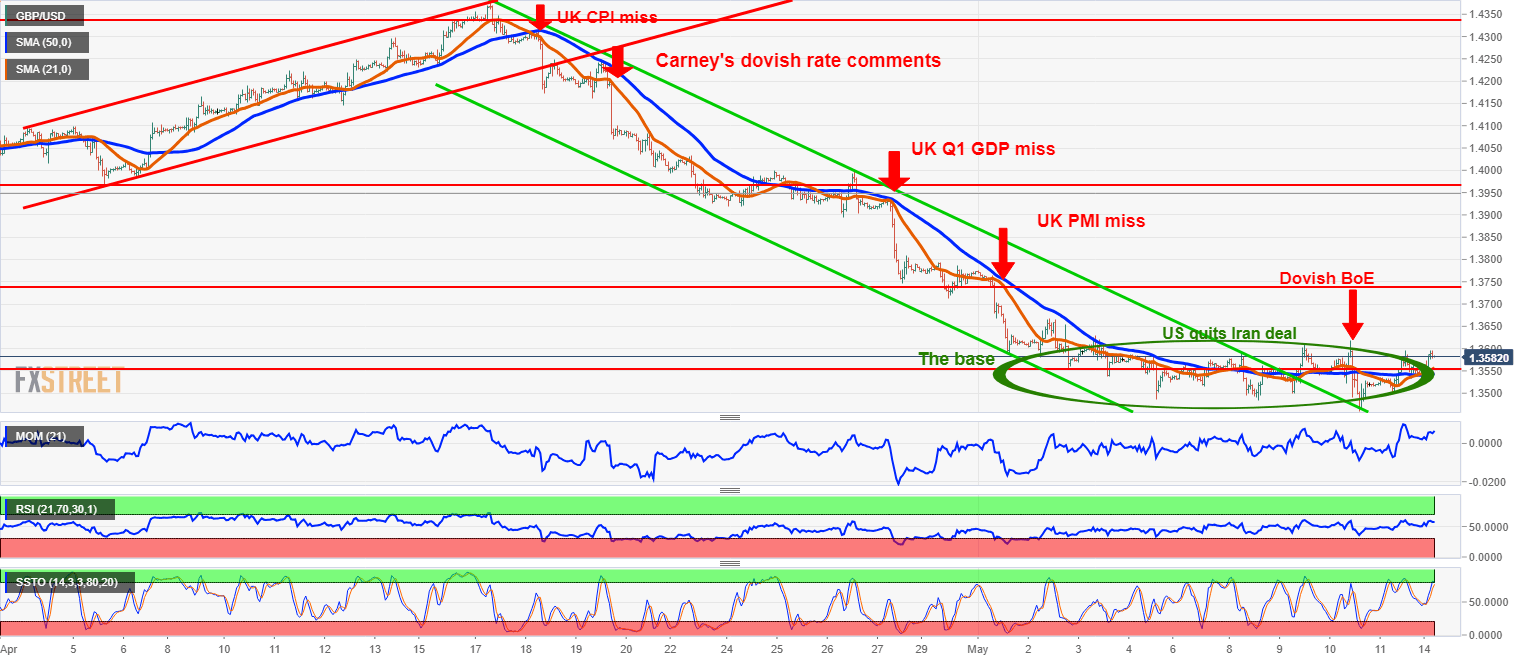

While the previous month’s labor market report for the UK served as an initial reason to sell the GBP/USD with further macroeconomic data releases missing the expectations and the Bank of England Governor Mark Carney’s dovish comments, now the wage growth of well above 2.5% inflation rate is seen as a reason for GBP/USD to rebound.

Regarding the interest rate outlook, the Bank of England Governor Mark Carney noted during the press conference after releasing May Inflation report last Thursday that the 3.0%-3.5% wage growth is still consistent with its outlook for very gradual and limited monetary policy normalization in the environment of persistent Brexit-related uncertainty.

That was also confirmed by the comments of drivers of the UK inflation that are expected to increasingly shift from external factors like the Brexit-related Sterling’s depreciation to more domestically driven factors including tight labor market conditions and rising wages.

Fundamentally, the rising wages a factor that the Bank of England is already counting with as it expects inflation-adjusted wages to support the UK consumer spending. The period of negative inflation-adjusted wages stated in January last year was continuously weighing on UK shoppers until last month’s wage growth accelerated to 2.8% y/y while inflation decelerated to 2.5% y/y.

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.