UK third-quarter GDP Analysis: Consumption and trade lead the way while investment is a drag

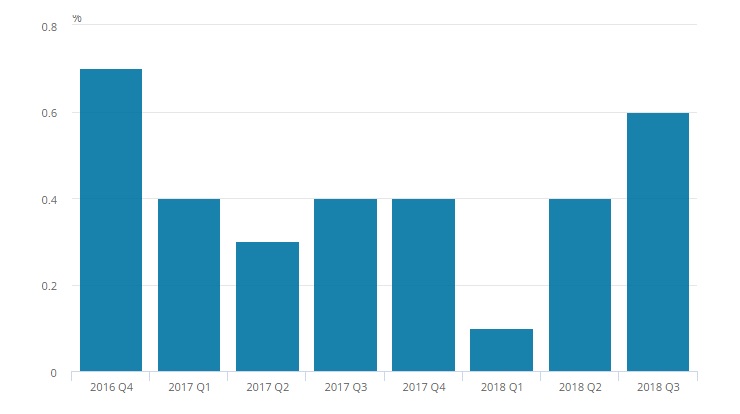

- Third-quarter UK gross domestic product (GDP) grew by 0.6%Q/Q, in line with market expectations.

- UK Q3 GDP growth was driven mainly by the services sector, although the construction sector also had a notable positive contribution.

- Over the year the UK third-quarter GDP rose 1.5%.

The UK third-quarter GDP came out in line with the market expectations as the quarterly rise of 0.6% and the annual increase of 1.5% were both projected by the consensus of market analysts and economists.

The structure of the UK third-quarter GDP was a bit of surprise, especially with production contributing positively to the third-quarter growth.

The main driver of UK GDP was services that contributed by 0.33% to the UK third-quarter growth rate followed by construction contributing by 0.13% and the production contributing by 0.11% the the third-quarter growth. Within this structure, the manufacturing contributed negatively to the third-quarter growth as it fell -0.2% over the quarter.

The head of the national accounts section at the Office for the National Statistics Rob Ken-Smith said that “the economy saw a strong summer, although longer-term economic growth remained subdued. There are some signs of weakness in September with slowing retail sales and a fall-back in domestic car purchases. However, car manufacture for export grew across the quarter, boosting factory output. Meanwhile, imports of cars dropped substantially helping to improve Britain’s trade balance.”

The UK third-quarter household expenditure growth increased to 0.5%, contributing 0.34% to GDP growth while investment was the only part to have contributed negatively to UK GDP growth by 0.14%, with increases in government and private dwelling investment being partially offset by a fall of 1.2% in early estimates of business investment.

The net trade also contributed positively to the UK third-quarter GDP growth, driven by a 2.7% rise in exports of goods and services.

UK GDP growth

Source: Office for the National Statistics

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.