UK set for slow recovery after record second quarter economic decline

The UK economy is likely to experience a decent rate of growth during the third quarter, but importantly it will be at least a couple of years before all of the lost ground is recovered. Consumer caution, the unwinding of the Job Retention scheme and the end of the post-Brexit transition period are pose risks to the recovery.

The 20.4% fall in UK second-quarter GDP will catch most of the headlines today. Britain’s lockdown was more protracted than most others, and that unsurprisingly means that the overall slowdown in activity through the first half of the year (-22%) was more pronounced than that in the Eurozone as a whole (albeit this masks big variations) and the US.

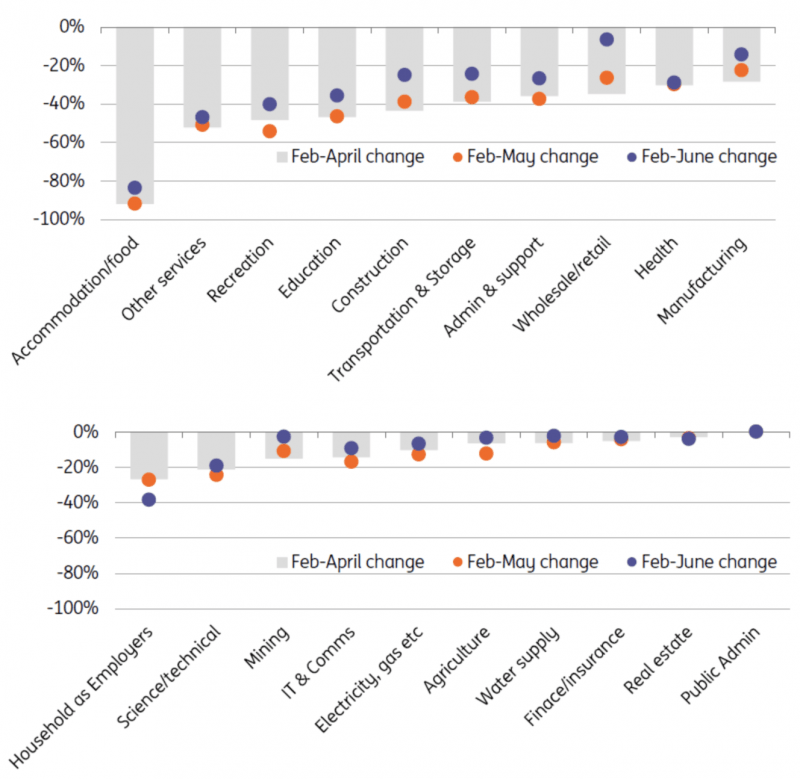

More importantly though, the latest monthly GDP figures indicate that activity saw a much more solid rebound in June than the disappointing outcome for May. Activity was up 8.7%, and unsurprisingly the industry breakdown shows that a fair chunk of the rebound came from wholesale/retail trade as shops began to reopen. Retail sales, don’t forget, are now essentially back to where they were before lockdown, although this partly reflects a big shift to online shopping.

We’d expect to see another decent bounce in GDP during July when a wider range of service-sector businesses were allowed to open. And arithmetically, the timing of all of these changes (towards the end of the second quarter, or early into the third) probably means that the UK’s third-quarter rebound is likely to appear larger than in many other economies. While we suspect the rebound may not be quite as large as the Bank of England’s 18% third-quarter growth forecast, it might not be far off.

Change in UK (monthly) GDP by industry

Source: Macrobond, ING calculations

Of course, percentages can be misleading, and the reality is that the overall size of the UK economy is still likely to be almost 10% smaller at the end of the third quarter than when to compared to pre-virus levels. We also suspect it will take at least another two-to-three years for the economy to regain all the lost ground, quite a bit longer than is being forecasted by the Bank of England (who assume a full recovery by the end of 2021).

Rising unemployment is probably the biggest threat to the recovery at the moment, and this is being linked to the gradual unwinding of the government’s furlough scheme over the next few months. Many firms, particularly in the hardest-hit hospitality/recreation sectors are still struggling as a result of ongoing consumer caution and social distancing constraints.

Investment is also likely to remain a major drag, particularly in light of the forthcoming changes at the end of the post-Brexit transition period. Even if there is a trade deal agreed this year, businesses will encounter a wave of new costs across a range of sectors. We'd note that the sectors likely to be most heavily affected (eg manufacturing) by these changes are not necessarily going to be the same as those hardest hit so far by the Covid-19 crisis (which has most severely hit consumer services).

For 2020 as a whole, we expect the UK economy to have shrunk by 9.7%.

Read the original article: UK set for slow recovery after record second-quarter economic decline

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.