UK labor market remains tight as wages rise less than expected

- The UK claimant count drops unexpectedly in May with the unemployment rate holding at a four-decade low of 4.2%. The April claimant count was revised down to 28.2K from 31.3K originally reported.

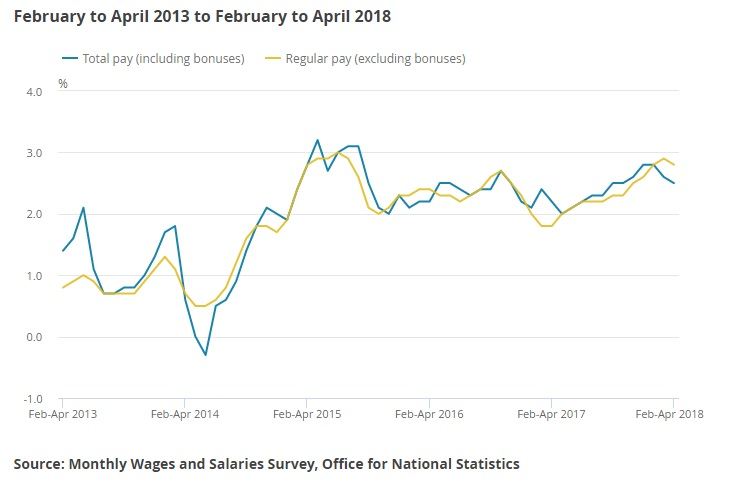

- The UK average weekly earnings excluding bonuses rise 2.8% y/y in three months to April, slightly less than 2.9% y/y expected.

- The UK average weekly earnings including bonuses rise 2.5% y/y in three months to April, slightly less than 2.5% y/y expected.

- The UK labor market report for May came out mixed with the claimant count falling unexpectedly by -7.7K and the April increase of 31.3K was revised down to 28.2K, while the wage growth slightly missed the market expectations.

Overall the tone of the UK labor market report was neutral with the labor market remaining tight, but not tight enough to generate strong wage growth to push the main policy goal-the inflation- higher.

While the wage growth in the UK is the key indicator of the underlying strength of the domestic demand in the UK, the recent labor market report was rather muted with the average weekly earnings excluding bonuses rising 2.8% y/y, slightly less than 2.9% y/y expected and the weekly earnings including bonuses rising 2.5% y/y, slightly less than 2.6% y/y expected.

The UK labor market report came out mixed while supporting GBP/USD around 1.3400, up from 1.3350 lows recorded earlier on Tuesday. The key voting in the lower chamber of the UK parliament is due on Tuesday and Wednesday after the House of Lords voted for the UK to remain part of the customs union after Brexit. The parliamentary vote is seen as a confidence vote for the UK Prime Minister Theresa May.

Meanwhile, the UK Justice Minister Lee resigned from the UK government to speak about the government Brexit policies. “When MPs vote on the House of Lords’ amendments to the EU Withdrawal Bill I will support the amendment which will empower Parliament to reject a bad deal and direct the Government to re-enter discussions. For me, this is about the important principle of Parliamentary sovereignty,” Lee wrote on his Twitter account.

Given the mix of relatively soft GDP reading for the first quarter, and slightly lower wage growth than expected, the Bank of England is in no rush to hike rates after turning increasingly dovish in May Inflation Report.

This is also reflected in markets’ expectations that see the Bank rate hike being priced in somewhere between NNovember2018 and February 2019. With Brexit legislation given some 3-4 months maximum before a final deal with EU can be done, the Bank of England is unlikely to hike rates as it repeatedly raised concerns about Brexit as a key risk for the monetary policy outlook.

The UK wage growth

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.