UK GDP falls in May amid growing concern about the economic outlook

The UK GDP figures have been incredibly volatile this year, and May's decline looks more like noise than signal. But there are growing concerns about the UK economy, driven by weakness in the jobs market. If next Thursday's payroll figures are bad, then it would pile the pressure on the Bank of England to speed up rate cuts.

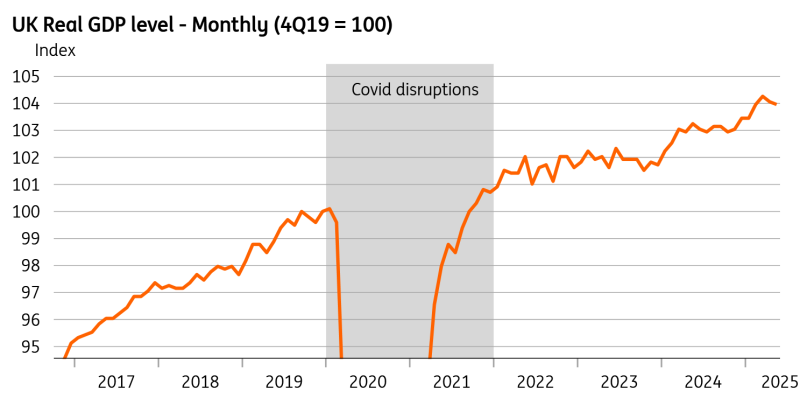

The UK economy contracted for the second month in a row in May, continuing what has been a tumultuous start to the year. In truth, the monthly GDP figures, which showed a 0.1% fall in May’s output, almost certainly exaggerate the volatility in underlying activity. The latest weakness follows a very strong first quarter, which was driven in no small part by tariff frontloading and home sales ahead of a Stamp Duty (tax) change in April.

We’ve also seen a pattern over recent years where the first quarter has recorded much stronger growth than the rest of the year, despite the data being adjusted for seasonal trends. This shouldn’t be the case now, and we suspect that seasonal adjustment has become much harder post-Covid and the most recent inflation wave.

The Bank of England opted to look through the first quarter strength, commenting instead that activity was probably more or less flat. We suspect it'll reach the same conclusion for the second quarter, where overall quarterly GDP growth is on track for 0.1%.

UK GDP had a suspiciously strong start to the year

Source: Macrobond, ING

Though it would be wrong to conclude from the GDP data alone that the economy is coming under greater pressure, there are genuine questions emanating from the jobs market and whether it is beginning to fall apart more quickly.

Remember that in May, payrolled employment fell at the sharpest rate outside of the pandemic (the data has been produced since 2014). This data may well be revised up, as is fairly common, but if that doesn’t happen – and indeed if June’s data is as bad as May’s – then it would raise difficult questions for both the Bank of England and the Treasury.

For the Bank, it would likely force a rethink on the pace of rate cuts. Until now, officials have appeared highly reluctant to move beyond their recent, gradual once-per-quarter cutting pace. In part, that is because the BoE assesses employment growth to be virtually flat. The latest data suggests that’s an increasingly optimistic view of the jobs market. For now, our base case is that the Bank cuts in August and November, but the risks are clearly tilted towards more frequent rate cuts before year-end.

For the Treasury, a jobs market that is deteriorating more quickly would – if confirmed – make life yet more difficult in the autumn. Tax rises already look fairly inevitable, and the option of a second round of hikes in employer taxation looks challenging in the current hiring environment. With the possible exception of extending the tax threshold freeze by another year, there are few other levers the Treasury can pull that would raise material amounts of additional tax revenue. It’s therefore increasingly likely the government will have to revisit a manifesto pledge not to raise the major taxes on individuals.

Read the original analysis: UK GDP falls in May amid growing concern about the economic outlook

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.