UK: Economic recovery is set to continue

Key takeaways

The UK economy was one of the hardest hit by the pandemic but we think the economic outlook looks bright. The relationship between new cases and hospitalisations have weakened significantly and the economy is fully re-opened. Consumer and business confidence are high.

We expect GDP growth of 7.5% this year and 6.4% next year.

We expect the unemployment rate will be back below 4% by the end of 2022.

We expect CPI inflation to move higher, peaking in early 2022 and then ease to around 2% in H2 22.

Brexit uncertainties have declined but remain high. EU-UK trade has recovered somewhat but not fully since the implementation of the new free trade agreement in January. Brexit has moved to the background as a market theme but risks remain due to discussions over the implementation of the Northern Ireland Protocol.

Bank of England is moving gradually in a more hawkish direction. We expect the Bank of England will end QE this year (perhaps even prematurely) but not hike until H2 22.

Growth outlook: Recovery is set to continue

Looking at the UK economy, the UK was one of the hardest hit countries by COVID-19 but things have improved a lot since then. There has been a lot of focus on the UK over the past month due to the delta variant, but new cases have started to move lower again, although we do not know the full implications of the re-opening of nightclubs etc. Regardless, the good news is that the relationship between new cases and hospitalisations/deaths has weakened a lot due to vaccines, which is also the main reason why the UK government decided to move on with the full re-opening.

The UK strategy has changed significantly, as the idea now is that people should learn how to live with the virus instead of imposing restrictions, helped by the vaccines.

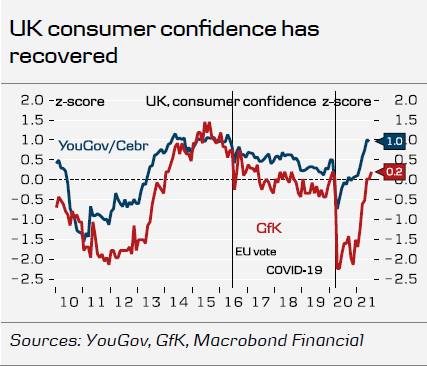

Monthly GDP rose by 2.1% m/m in April and 0.7% m/m in May so even without any growth at all in June, Q2 GDP grew by 4.4% q/q. Based on retail sales, private consumption rose significantly in Q2 after declining in Q1, as retail sales rose more than 10% (see chart to the right). Consumer confidence has recovered significantly (see chart to the right) suggesting still decent private consumption growth going forward. Private consumption remains the most important growth driver in the UK.

GDP declined by 9.8% in 2020 but we project GDP will rise by 7.5% this year and 6.4% next year. We expect GDP to be above pre-pandemic levels in Q4 this year.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.