UK CPI inflation increased by 2.3% in October

A report released this morning by the Office for National Statistics (ONS) revealed that all key inflation measures exceeded expectations in October. As a result, the British pound (GBP) appreciated against all G10 currencies, with the strongest gains seen against the Japanese yen (JPY). Additionally, FTSE 100 futures experienced a moderate decline following the report, contributing to intraday losses.

Headline CPI inflation rose in October on higher energy costs

Headline Consumer Price Index (CPI) inflation increased by 2.3% year on year (YY), exceeding economists' expectations (2.2%) and accelerating from the 1.7% reading in September. On a month-on-month (MM) basis, CPI inflation rose by 0.6%, surpassing the market consensus estimate of 0.5% and the previous figure of 0.0%.

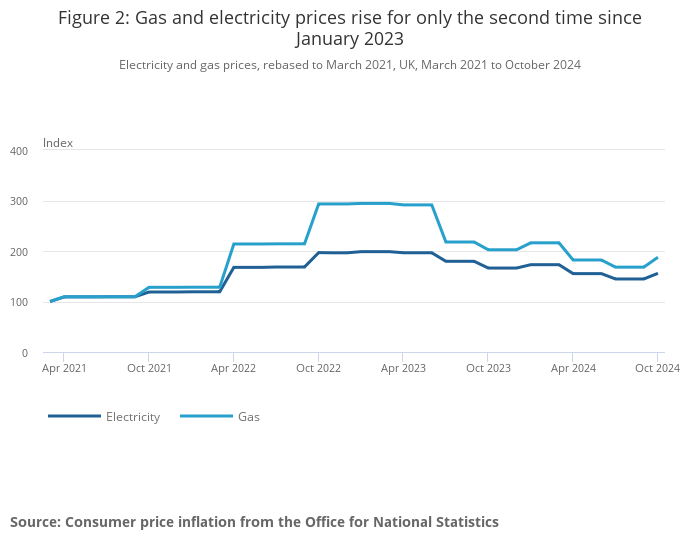

According to the ONS report, headline inflation increased in October due to rising prices in 'housing and household services’, which rose by 1.3% MM (from -0.3%) and by 5.5% YY (from 3.8%). The ONS noted that the most significant upward contribution came from electricity and gas prices, which offset the downward price effects of 'recreation and culture'. Additionally, the report indicated that electricity prices rose by 7.7% YY, and gas prices increased by 11.7% YY, both of which followed declines of 7.5% and 7.0% in September, respectively.

Economists widely anticipated increased price pressures in October due to a 10% rise in the energy price cap, which is now set at £1,717 per year for a typical household.

Looking further under the hood, you will see that ‘food and non-alcoholic beverages’ ticked slightly higher on a YY measure, rising 1.9% from 1.8% in September. The ONS noted: ‘The annual rate of 1.9% is down from a recent high of 19.2% in March 2023, the highest annual rate seen for over 45 years’, and added: ‘Vegetables (including potatoes) was the only one of the 11 food and non-alcoholic beverage classes to provide an upward contribution to the change in the annual inflation rate between September and October 2024’.

Excluding energy, food, tobacco, and alcohol, core inflation rose by 3.3% versus 3.1% expected and was up from 3.2% in September. Monthly, core inflation jumped by 0.4%, beating the market’s median estimate of 0.3% and bettering the 0.1% reading in September.

Undoubtedly, markets and the BoE were also focussed on the services CPI inflation numbers, which also reported higher-than-expected figures on both MM (0.4% versus 0.2% expected) and YY (5.0% versus 4.9% expected) metrics. Still, it is worth observing that service inflation aligns with the Bank of England’s (BoE) latest forecasts.

Markets and what next?

Money market expectations showed a minor dovish repricing in the BoE’s Bank Rate; investors have now almost fully priced out chances of a 25 bp rate cut next month, with around 60 bps of easing currently priced in until the end of 2025.

You will recall that the BoE reduced the Bank Rate by 25 bps to 4.75% at its previous meeting, signalling a gradual approach to easing policy. This was underlined by BoE Governor Andrew Bailey yesterday to the House of Commons Treasury Select Committee.

Ultimately, the latest inflation numbers triggered a rather muted response from major asset classes, with the GBP, gilts and equities all trading pretty much unchanged this morning.

Technically, for the GBP/USD currency pair, the lack of follow-through to the upside makes sense on the daily chart, having seen the pair test resistance at US$1.2708 after recently leaving ascending support unchallenged (taken from the low of US$1.2037). However, you will note from the monthly chart that support also entered the fray at US$1.2715; consequently, I am watching the aforementioned daily levels closely for signs of a breakout to determine technical direction.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,