UK CPI inflation data ahead: Sterling hovering north of key support

Following today's mixed bag of employment and wages data, tomorrow’s attention is directed to the March UK CPI inflation release, scheduled to air at 7:00 am GMT+1.

Estimates Suggest Further Disinflation

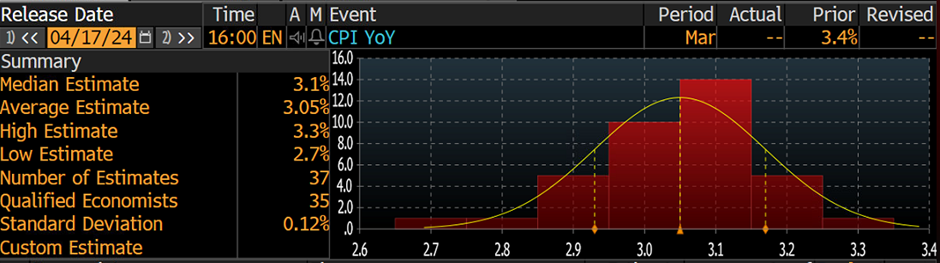

Both headline and core (excludes food, energy, tobacco and alcohol) measures have surprised to the downside in the previous two releases and are expected to demonstrate further evidence of disinflation tomorrow, forecast to rise +3.1% (from +3.4% in February) and increase +4.1% (from +4.5% in February) on a year-on-year basis, respectively. This is quite the contrast to the US inflation picture, which has seen headline year-on-year inflation come in stronger than expected for four consecutive periods, with the core year-on-year measure unable to budge from a near-three-year low of 3.8%. Upper and lower-range estimates will also be closely observed heading into the release. For the headline report, the upper and lower limits are between 3.3% and 2.7%, while the core is between 4.6% and 3.8%.

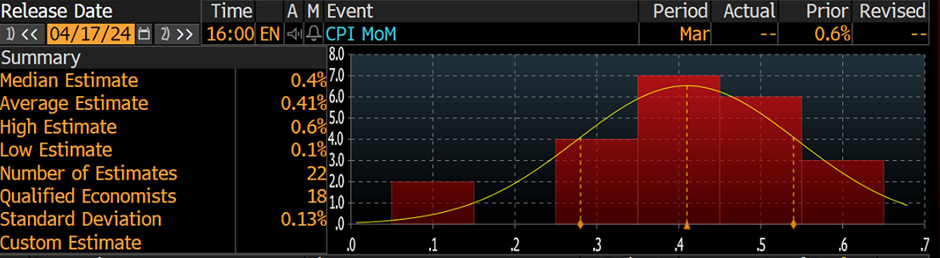

Between February and March, the median estimates also suggest cooling inflation. Headline inflation is forecast to rise +0.4% (from +0.6%), and core is expected to rise +0.5% (from +0.6%). Estimate extremes to be aware of for the headline release are between 0.6% and 0.1%, and for the core is seen between 0.7% and -0.4%. Services inflation will also be a key watch for investors and the Bank of England (BoE), which you may remember cooled to 6.1% in February, down from 6.5% in January.

As you can see, economists already foresee deceleration across the board for all the key measures mentioned above. For that reason, a broad miss would need to be seen to trigger a meaningful push lower in sterling: a release that tests space around the lower range estimate extremes, for example. Should this come to fruition, another disinflationary print could also result in a dovish repricing for rates.

Two rate cuts this year

The CPI measure is what the BoE use for their inflation targeting, which is currently fixed at 2.0% by the UK Government. In terms of the OIS curve, a total of -48bps is priced in for 2024 (essentially, two rate cuts); a notable hawkish shift was seen in recent weeks, triggered largely on the back of hotter US CPI inflation and commentary from BoE’s Megan Greene communicating that ‘rate cuts in the UK should be way off’.

May’s policy-setting meeting is unlikely to see the BoE cut rates, according to market pricing (10.0% probability currently forecasted for a -25bp rate cut [-3bps priced in]). June also looks unlikely, with -10bps of easing forecasted. As of writing, it’s now a hit-or-miss between August and September’s meetings for a -25bps cut. Of course, tomorrow’s CPI inflation report could change things.

GBP/USD support still calling for attention

You may recall that the FP Markets Research Team released a week-ahead post on the technicals for the GBP/USD currency pair. The Team noted the following (italics):

Both monthly and daily charts exhibit scope to navigate lower levels; the daily chart shows support is not expected to enter the fray until $1.2331-$1.2366, which leaves H1 price action technically free to take aim at the $1.24 handle, at least. With that, short-term traders moderately sold into a pullback at $1.2462 on Friday [level since removed], which may be enough to trigger further underperformance this week towards $1.24. Though should a pop higher unfold, eyes will be on $1.2498-$1.2489 as a potential area of resistance.

As can be seen from the charts, H1 price responded well from the decision point area of $1.2498-$1.2489 already this week and voyaged within striking distance of $1.24.

Focus going into tomorrow’s inflation print, therefore, will be on the daily support area between $1.2331-$1.2366, which, technically speaking, reveals room for a spike lower. This area consists of a handful of Fibonacci ratios, channel support (extended from the low of $1.2513) and ascending support (drawn from the low of $1.2037). A broad miss in the upcoming data could see the unit engulf bids around the $1.24 area, clear out any weak hands (sell stops located beneath the big figure) and perhaps recoil back to the upside from daily support.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,