Trade tensions recede, central banks in focus: A market outlook for traders

Macro landscape

Trade war risk recedes, focus shifts to central banks

The global macro narrative pivots today as the US and EU clinch a historic trade agreement. By settling on a 15% tariff—half of the threatened rate—the deal averts an all-out trade war, removing a persistent tail risk from markets. Investor anxiety over supply chains, export-dependent sectors, and global growth has sharply diminished, fueling a broad-based “relief rally” in risk assets. The deal also offers a framework for further de-escalation, with US-China negotiations now in focus and a three-month tariff truce extension expected.

Key implications for traders

Equity and credit markets are likely to see reduced volatility and tighter risk premiums, at least until the next central bank decision. European autos, luxury goods, and industrials are catch-up plays, but face new operating realities. US exporters (energy, defense) stand to gain.

Initial EUR/USD strength faded as traders re-assessed the medium-term impact—tariffs are a drag on European growth, and USD regains favor on relative policy and yield.

Central bank week

Positioning ahead of the Fed and BoJ

This week is a critical inflection point. Both the Federal Reserve and the Bank of Japan will meet, with consensus for no change in policy rates. However, forward guidance is what matters:

Fed: Markets are split between those expecting a dovish tilt (potential cut signal later in 2025) and those seeing “higher for longer.” US data has been resilient, but the White House is pressuring for cuts. How Powell frames the balance of risks will drive the next leg in USD, equities, and gold.

BOJ: The yen remains weak, but policymakers are wary of further currency depreciation. Expect traders to fade extremes in USD/JPY unless BOJ signals a shift.

This is not a “wait and see” week. The window for repricing risk is open now, and the market will punish those who get caught on the wrong side of central bank language. Volatility is likely to spike around decision times.

Equity markets: Relief rally or last squeeze?

S&P 500 and EuroStoxx futures gapped higher at the open, confirming the “macro overhang” has lifted—for now. The S&P 500 remains at record highs, driven by a collapse in left-tail risk from tariffs, robust US corporate earnings (over 80% beat rate) and systematic and passive flows.

But the rally is late-stage as Technicals are overbought (stochastics, RSI) across indices. We also see on charts that breadth is narrowing (leadership is in megacap tech, autos, and select consumer cyclicals). While volatility is still suppressed, risk of reversal is high on any negative Fed or earnings surprise.

In Europe, Stoxx 600 is still 2.3% below March highs. Relief is most pronounced in sectors that were punished in Q2: autos, luxury, consumer. But watch for “buy the rumor, sell the fact” into the close as traders reposition ahead of central banks and earnings.

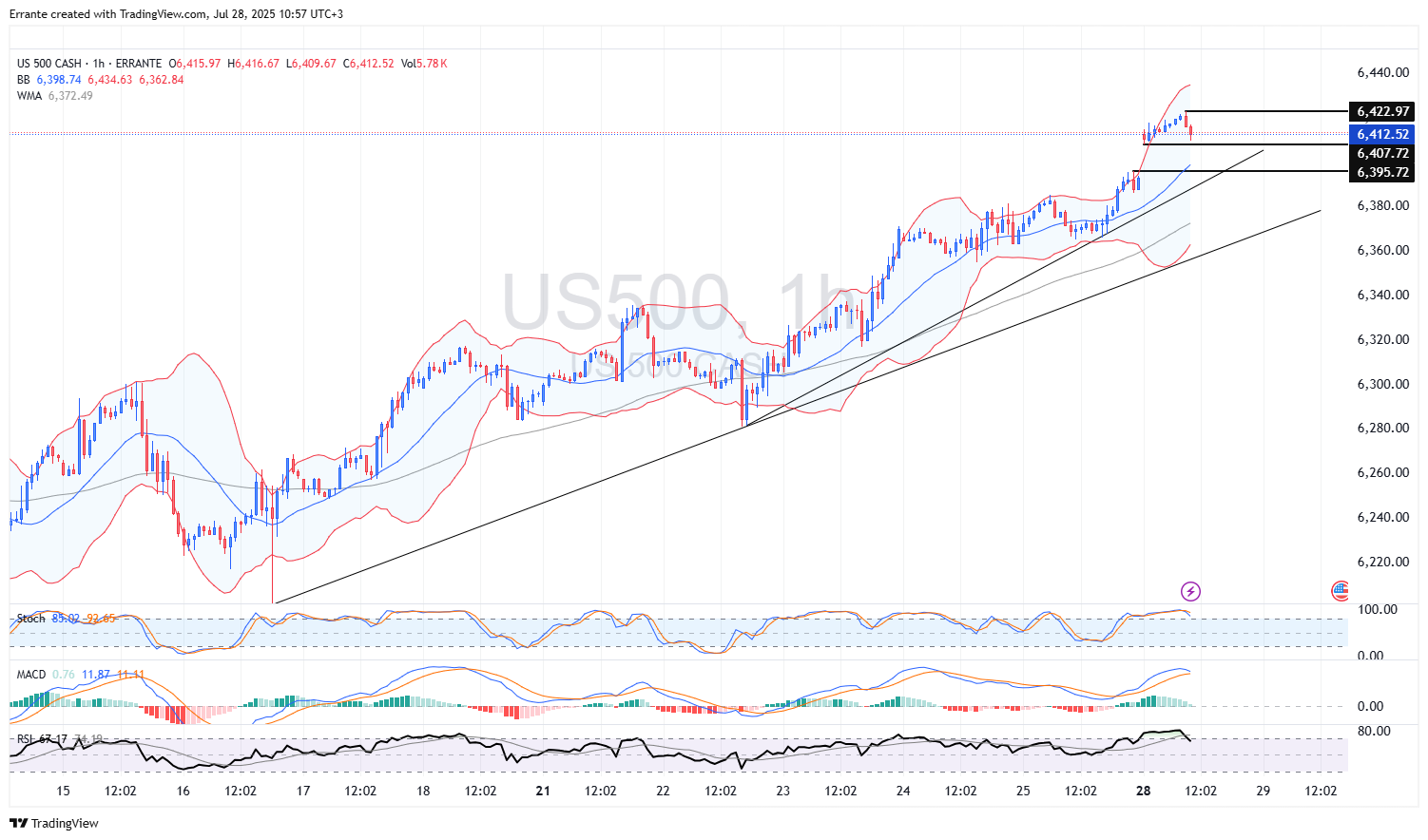

US500 (S&P 500 Index, one-hour)

The uptrend remains intact, making fresh highs after Friday’s record close. The US-EU deal extinguished a major macro headwind, fueling continuation buying in global equities.

Technical structure

-

Support: 6,407.7 (intraday), followed by 6,395.7 (trendline and WMA).

-

Resistance: 6,422.9 (intraday high).

Stochastic (83): Overbought, beginning to cross down.

RSI (67): Extended, not divergent, but risk of short-term mean reversion.

MACD: Still positive, histogram flattening.

Actionable take

The market is running on relief and momentum, but do not chase highs blindly. Wait for a retracement to 6,408–6,396 for new long entries.

The week’s catalyst will be Fed guidance—any dovish surprise could extend the rally, but a hawkish tilt or “no cut” disappointment will likely trigger a sharper pullback.

A break below 6,395 could trigger accelerated profit-taking toward the 6,372 support line (WMA).

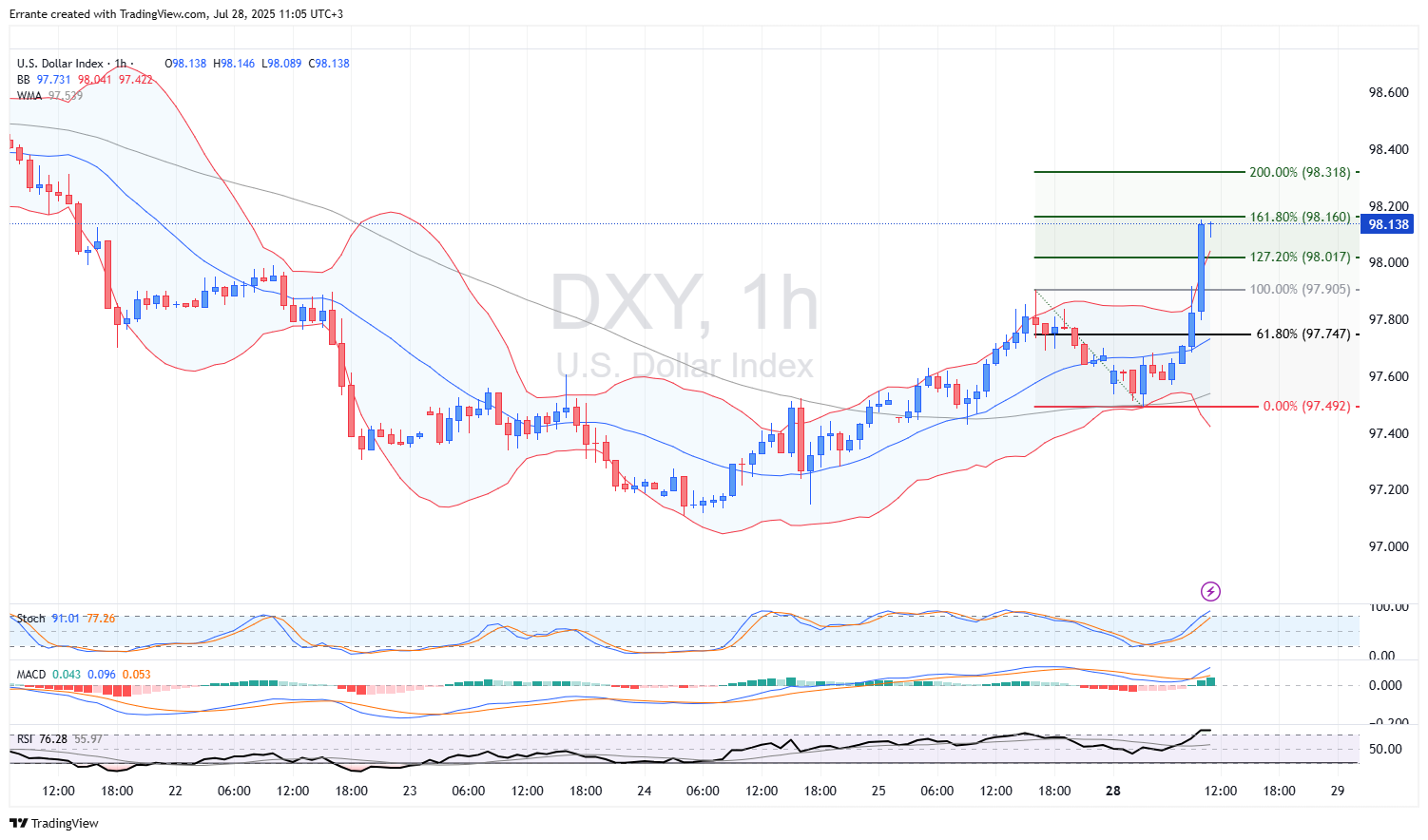

FX: Dollar regains the initiative

DXY Explodes higher post-deal, breaking resistance as short positions are unwound. USD strength is partly technical (short squeeze), partly a function of relative yield outlook. In other words, the dollar is benefitting from an unwind of “risk-off USD shorts” and renewed expectations that US yields will remain favorable.

Technical structure

- Key support: 97.75 (61.8% Fib of last leg up), then 97.49 (trend low).

- Resistance: 98.16 (161.8% Fib extension), 98.32 (200%).

RSI: 76 (deeply overbought).

Stochastic: 91 (extreme).

MACD: Bullish, but histogram peaking.

Actionable take

Don’t buy breakouts at these levels; look for retracement toward 97.90 or even 97.75 as an opportunity to fade or scale in long on renewed policy divergence. If DXY sustains above 98.20 after the Fed, a medium-term target toward 98.80–99.00 opens up.

If price rejects above 98.16 and closes below 98.00, expect fast mean reversion as short-term positioning resets.

Rates & Bonds: Duration Remains a Widowmaker

US yields: Firm as risk is taken off, but direction hinges on Fed.

GB10Y (UK 10Y Gilt Yield)

2061s collapse continues—down over 70% since 2022. Duration remains toxic for retail and institutional investors; “buying the dip” is not a strategy until inflation/fiscal stability returns.

Testing rising support, but yields are softening as “duration trades” falter.

Technical structure

- Support: 4.61 (trendline), 4.59, 4.55 (Fibs and structural).

- Resistance: 4.63–4.67 (last week’s highs).

Stochastic: 21 (oversold, no reversal yet).

RSI: 43 (neutral/slightly bearish).

Actionable take

The failure to hold above 4.63% suggests further downside risk in yields, with technicals favoring a push toward 4.59%–4.55%. This fits with the “losing bet” narrative around UK long bonds—private investors hoping for a reversal have been punished, and as long as the fiscal/inflation outlook is uncertain, rallies in Gilts will be shallow and sold.

Traders should reduce duration exposure into the Fed, and use rallies to rotate into shorter maturities or inflation-linked bonds. Tactical shorts in long-duration Gilts remain a high-probability trade.

Commodities: Oil and Gold diverge on risk sentiment

WTI and Brent rise modestly (0.9%) on trade optimism and expectations of extended US-China tariff truce. Despite bullish headlines, oil remains vulnerable to macro disappointment and supply shocks. News of resuming Venezuelan supply and possible OPEC+ increases are headwinds. If risk-on persists and supply disappoints, bulls could target $67–68, but the baseline is more rangebound volatility.

WTI (US Crude Oil)

Choppy range with a recovery bias after three-week lows. The US-EU deal and US-China truce extension hopes are lifting demand expectations, while OPEC+ supply guidance is the wild card.

Technical structure

- Resistance: $65.49 (intraday), $66.29 (swing).

- Support: $64.98/$64.73 (minor), $64.50 (trend).

RSI: 43.9 (bearish but flattening).

Stochastics: 59 (neutral), crossing lower.

MACD: Slightly negative.

Actionable take

Fade rallies below $65.50 unless OPEC+ surprises with an aggressive cut. The US-EU deal helps sentiment, but structural overhang (Venezuela, OPEC+ supply return) caps upside. Watch $64.73—loss of this level could accelerate liquidations toward $64.00, while break and close above $66.29 would be a technical game-changer.

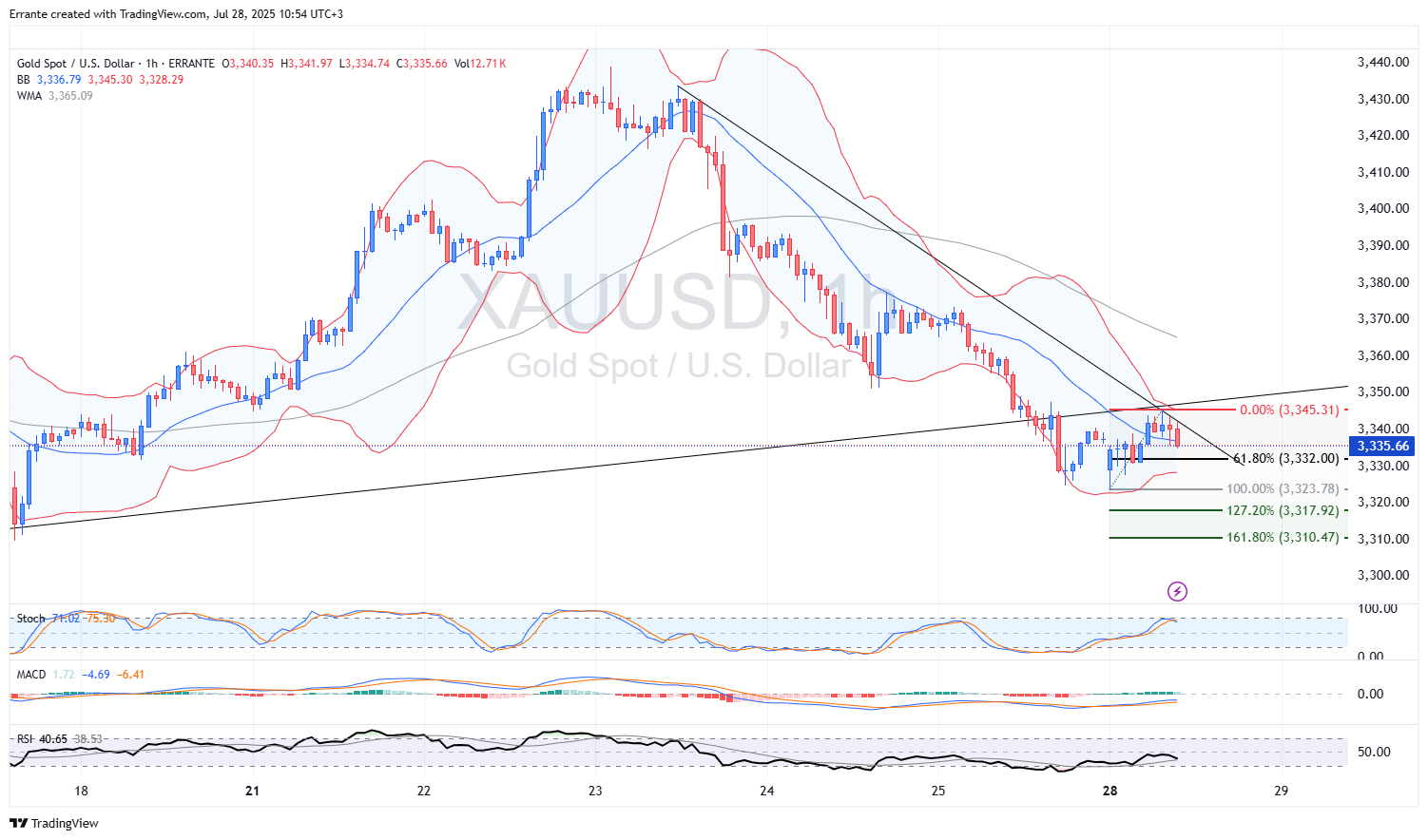

XAU/USD (Gold Spot, one-hour)

Gold’s softness is a direct function of lower volatility and receding tail risks. Any re-escalation in US-China or geopolitical news, or a dovish Fed, will restore its appeal. Don’t write off gold in this environment—volatility is never far away.

Sideways-to-lower after risk appetite returned, but strong technical support below.

Technical structure

- Support: $3,332 (61.8% Fib), $3,323, $3,318 (extensions).

- Resistance: $3,345 (trendline), $3,360 (WMA, breakdown origin).

RSI: 40 (bearish but not oversold).

Stochastics: 71 (losing upward momentum).

MACD: Negative.

Actionable take

Cautious traders should avoid chasing breakdowns. Look for stabilization above $3,332 or bullish reversal on Fed “dovish” language as a tactical long. If risk-on persists and Fed is hawkish, expect gold to grind lower toward $3,318, where stronger support and value buyers should emerge.

Industrial metals such as copper and platinum are muted; demand growth is being offset by macro uncertainty and FX moves.

Tactical themes and risks to watch

European autos, luxury, and exporters are likely to outperform short-term, but rallies will be tactical unless earnings deliver and tariffs do not escalate further. Mega-cap tech earnings will drive index leadership—watch for cracks in the narrative.

Market is hypersensitive to any deviation from “steady hands”—position for volatility spikes at FOMC, BOJ, and BOC events.

Thin summer trading could amplify both rallies and reversals; manage risk accordingly.

Trading playbook for today

-

Do not chase breakouts in overbought indices or FX.

-

Be tactical: Use retracements to add to positions; set tight stops on all new trades.

-

Watch sector flows: Look for tactical long opportunities in laggards (EU autos, luxury), but stay nimble.

-

Risk management: Hedge macro exposure—use gold and short-duration bonds as volatility buffers.

-

Stay flexible: Macro tail risks have receded, but the cycle is mature and prone to event-driven reversals. Let the market come to you.

Author

Ali Mortazavi

Errante

BEc, CMSA, Member of IFTA - International Federation of Technical Analysis, Associate Member of STA - Society of Technical Analysis (UK).