Three new scenarios for the global recovery’s next phase

With the economic rebound from Covid-19 now in full swing, we look at what could be a turbulent path to a full recovery. Our new-look scenarios map out potential paths for the global economy depending on how the virus spreads over the winter, and how quickly a vaccine is certified and rolled out to the wider population.

Summer is almost over and the global economy is preparing for an exciting autumn.

How strong will the mechanical rebound be in the third quarter? How strong will the permanent damage be to different economies? Will there be a second wave of Covid-19 and subsequent lockdowns? And, how will governments balance between public health and economic interests? Hopefully, we'll get answers to some of these questions in the coming weeks.

In this second stage, all economic forecasts are again highly dependent on two factors: the further development of the virus and the timing and distribution of any vaccine. To some extent, we are in a similar situation as we were towards the start of the crisis when the main drivers of all forecasts were outside the economic arena.

We haven't become virologists but looking at the number of new cases over the summer, it appears that there is a wider discrepancy between infected people and death tolls. The mortality rate is currently much lower than it was from January to April. This can have several reasons: more testing, less social distancing and therefore younger age groups being infected (in Europe, the average age of new cases has come down by almost 20 years) and a weakening of the virus over time due to summer temperatures or mutation.

Unfortunately, the drop in mortality rate is neither an argument for ‘the worst is over' nor for complacency.

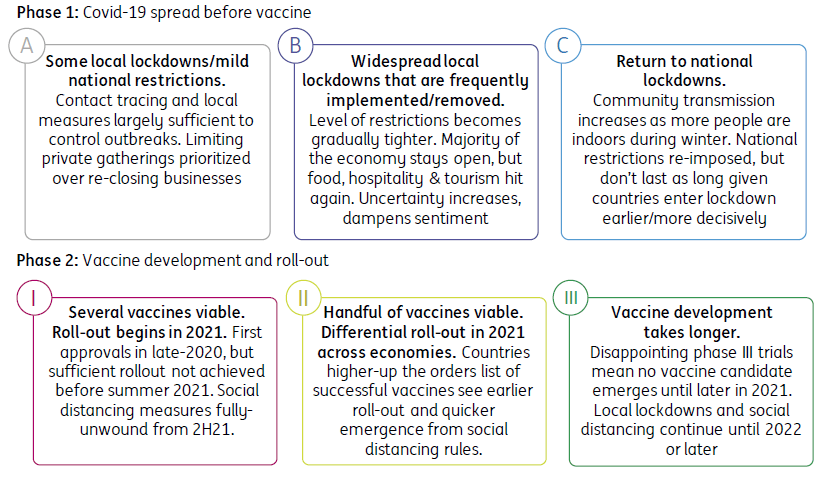

Mapping the next phase of the recovery

Source: ING

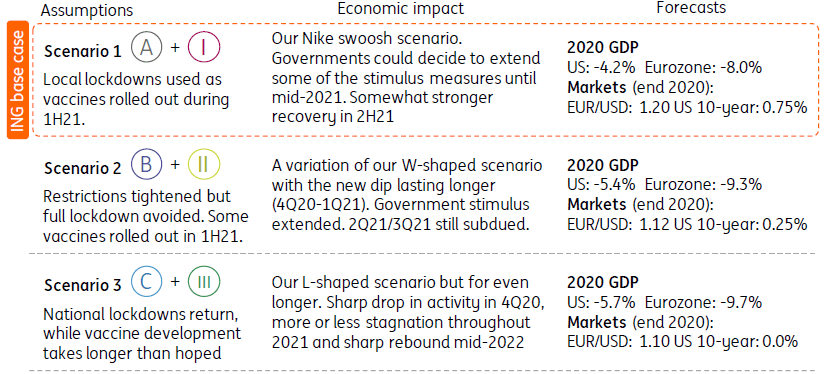

Three new scenarios

Source: ING

The economics of the vaccine

With a few vaccines now in third-stage trials, a scenario without any vaccine in the next 18 months looks highly unlikely. However, the effectiveness, as well as potential adverse side effects of any vaccine, remain uncertain. A recent study estimated a vaccine needs to be at least 70% effective if three-quarters of the population is inoculated, a tough task given the accelerated development timeline.

With the prospects of a vaccine increasing, the next question will be how to distribute it. We know that many vaccine producers have already started to produce millions of dosages in parallel to the final trial stages in order to be ready to distribute once their vaccine is allowed to enter the market. But how many doses will be available remains unclear. And even if there are enough doses available, distributing them will take time.

Also, it is likely that the distribution might not be equal across countries, possibly contributing to a new divergence between developed and developing economies.

Our three main scenarios

Looking ahead, there are many ways in which the virus and possible lockdowns and the distribution of any vaccine can play out. We try to capture the most likely outcomes in our latest three scenarios.

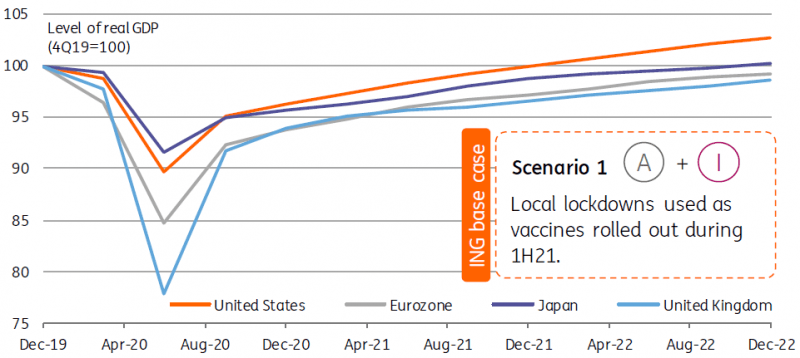

Our base case scenario assumes no real flaring up of the virus in the autumn and only local lockdowns. Governments put more intense focus on restricting private gatherings, with limited direct economic impact. Ongoing working from home arrangements and sharply reduced travel mean the virus spread takes longer and is easier to control.

Rapidly developing knowledge of the virus and the best way to treat it in the hospital will also help. Businesses also become more innovative at operating within constraints. That said, we may see a higher rate of business closures in the heavily-affected sectors as firms concede a return to profitability won't be possible for the foreseeable future. Vaccines will be rolled out in the course of the first half of 2021. Social distancing will gradually be reduced in the course of the second half of the year.

Scenario 1: The path for real GDP

Source: ING

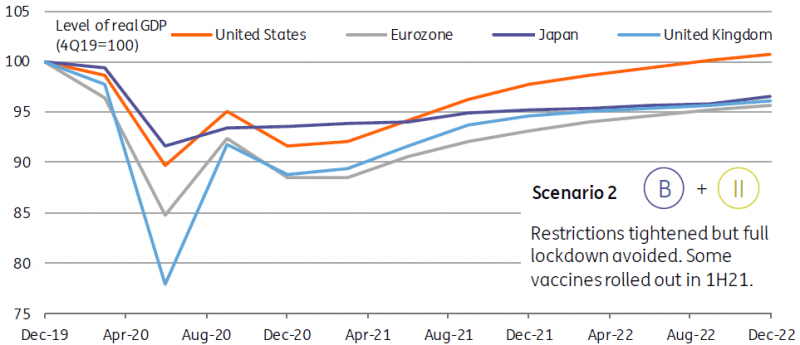

A not so unrealistic alternative scenario is our revised winter lockdown scenario (the W-shaped recovery). Here, the virus becomes more prevalent in the community throughout the winter months as people spend more time indoors. The level of restrictions becomes gradually tighter, potentially involving the re-closure of the food and accommodation sectors, as well as tourism.

Contrary to our previous assumptions, we would not see a return to full national lockdowns but rather a frequent on and off of local and regional lockdowns, substantially undermining business and consumer confidence. Businesses that survived lockdown may not be able to make it through, although it depends how reactive government support becomes when local lockdowns occur. Some vaccines are rolled out in the first half of 2021.

Scenario 2: The path for real GDP

Source: ING

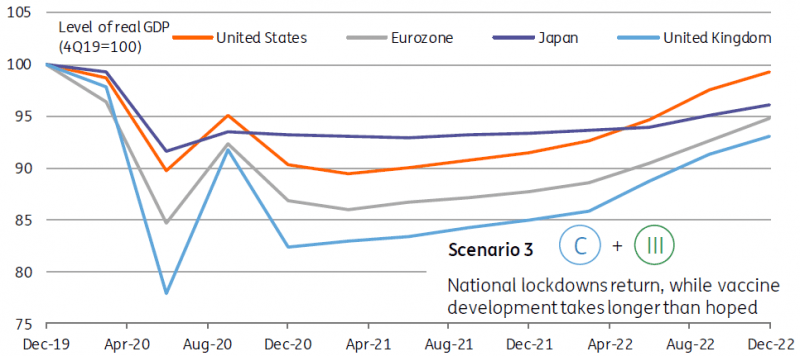

Our worst-case scenario (formerly the L-shaped recovery) remains one in which the virus mutates and spreads again during winter, with the death rate rising significantly.

Consequently, governments bring their economies into full lockdown again. The countries which reacted rather late in March and April are likely to react much faster this time. Therefore, the full lockdown could be shorter than it was this year. However, another wave of full lockdowns could push many businesses into bankruptcy and lead to a sharp increase in unemployment.

Some governments might react with another round of fiscal stimulus but not all will be able to afford it, adding to new tensions, particularly in the eurozone. The development of a vaccine experiences unexpected setbacks and takes until early 2022.

Scenario 3: The path for real GDP

Source: ING

For instance, while we think our scenario one best fits the current base case across the developed world, the growth path under scenario two is our new base case for China.

Read the original analysis: Three new scenarios for the global recovery’s next phase

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.