Think ahead: Mixed inflation data

Core CPI data from the US next week could ease concerns about prolonged elevated inflation while in Central and Eastern Europe, inflation readings look set to remain high.

Think ahead in developed markets

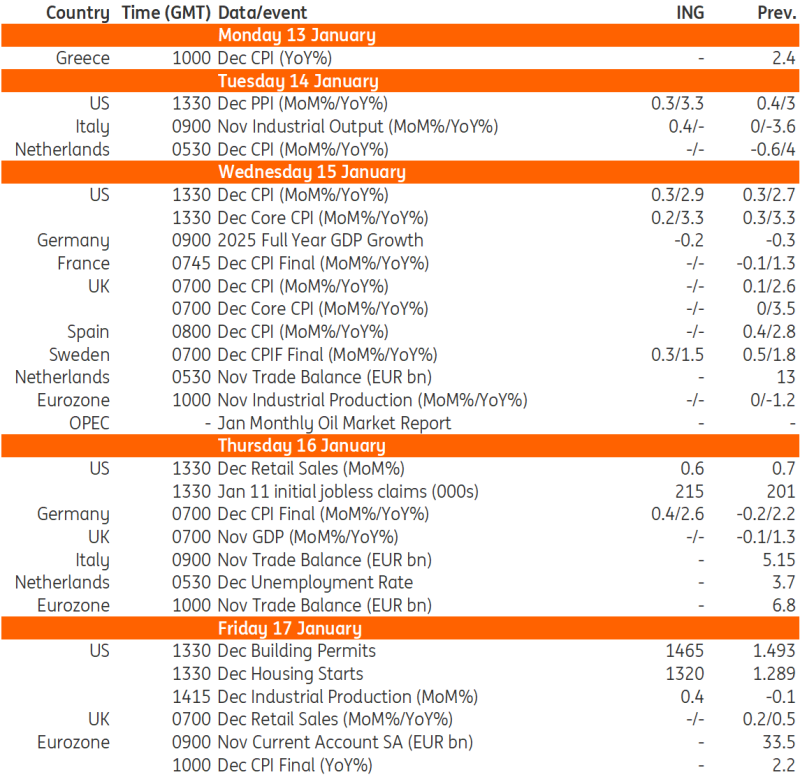

United States

Markets are barely pricing two rate cuts from the Federal Reserve this year with Fed officials themselves suggesting they are of a similar mindset. President-elect Trump’s policy mix of low taxation and light touch regulations is thought to be supportive for growth in the near term while his focus on immigration controls and trade protectionism are likely to raise inflation pressures over the medium to longer term. Nonetheless, we think the bark will be worse than the bite from tariffs as deals are struck and we continue to see a cooling in the jobs market. Moreover, while the Fed has cut rates 100bp, mortgage rates have soared, consumer borrowing costs elsewhere remain elevated and the dollar has strengthened more than 8%. All of these are counteracting the Fed’s rate cuts and we take the view that the Fed may need to push harder and cut rates further than currently discounted.

The key data points to watch next are consumer price inflation and retail sales. Core CPI has been coming in far too hot in recent months, but the market is favouring a 0.2% month-on-month outcome for the December report, which may go some way to easing concerns about prolonged elevated inflation readings. Retail sales should be lifted by firm car sales, but outside of this component, we look for signs of softness, particularly given the weakness seen in recent consumer credit numbers.

Think ahead for Central and Eastern Europe

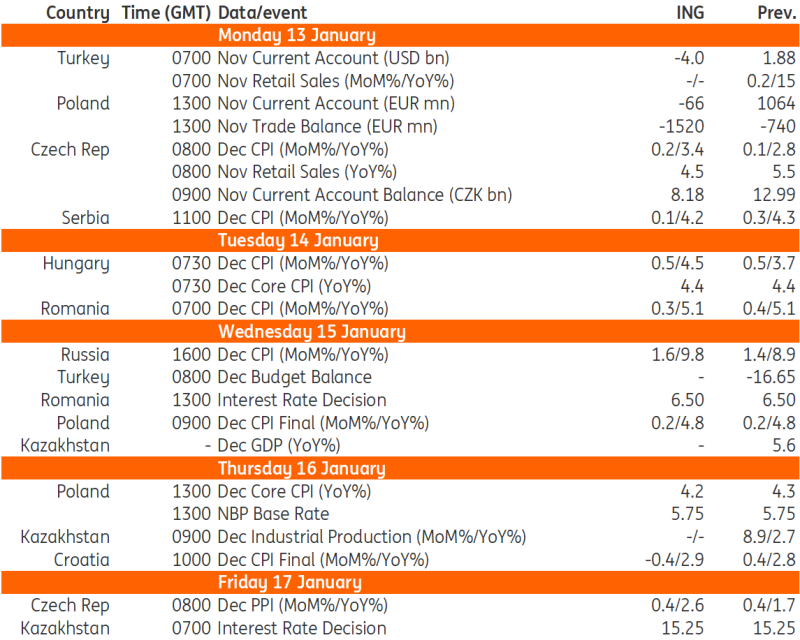

Poland

NBP rate decision (Thu): Polish policy rates will remain unchanged in January. The National Bank of Poland's policy stance turned more hawkish in December as Governor Adam Glapiński highlighted the inflation risks and attempted to convince the markets that a discussion on rate cuts would be initiated in late 2025 rather than in March as suggested earlier. The MPC seems to be confused and some policymakers were genuinely surprised by this unexpected shift in the chairman's policy bias as there was a solid majority for a debate on cuts after the March 2025 projections, ahead of the December policy sitting. The December flash CPI gave no grounds for a more hawkish policy stance as it surprised to the downside. Headline inflation is projected to rise in early 2025, but should decline visibly in the second half of the year, giving room for policy easing. We still do not rule out a first cut in 2Q25.

Current account (Mon): We forecast that in November 2024, the current account posted a slight deficit amid a further widening of the trade balance. We see the 12-month rolling current account surplus narrowing to 0.2% of GDP from 0.4% of GDP after October. According to our forecasts, exports of goods in euros fell by 3.0% year-on-year, while imports rose by 0.9% YoY. External demand remains weak, while the domestic economy continues to recover. The zloty remains strong vs. the euro, reflecting the substantial inflow of EU funds that the government may not only exchange at the central bank but also on the market.

Core inflation (Thu): On the basis of the December flash CPI, we estimate that core inflation excluding food and energy prices moderated to 4.2% YoY from 4.3% YoY in November, remaining elevated. Wednesday’s detailed data on the CPI composition will allow us and market participants to make an even more precise estimate.

Hungary

Inflation (Tue): We forecast yet another strong monthly repricing with the headline reading expected to be at 0.5% month-on-month in December. We see fuel, unprocessed food and services prices driving price pressures higher. Last year’s low base means that the year-on-year headline print will jump out of the central bank’s inflation tolerance band, reaching 4.5%. As most of the monthly price pressures are coming from non-core items, core inflation is likely to remain flat at 4.4% year-on-year. Our forecast is only slightly higher than the National Bank of Hungary’s projection, so we don’t expect any major monetary policy or market reaction.

Romania

Inflation (Tue): We estimate that Romanian inflation closed 2024 marginally above the 5.0% mark as stronger-than-expected food and energy prices combined with sticky service inflation shifted the entire inflation profile upwards.

Interest rates (Wed): Stubborn inflation is likely to be the main argument for the National Bank of Romania (NBR) to keep the key rate on hold at 6.50% at its 15 January meeting. We anticipate a relatively neutral press release, underlining the uncertainties surrounding the adoption of the 2025 budget law, the unclear outlook for energy prices and the volatile external context. With inflation more likely to average close to 5.0% in 2025, well above the NBR's 2.5% inflation target, we see limited scope for policy easing in 2025 and now pencil in only 50bp of rate cuts to come in the second half of the year.

Czech Republic

Inflation (Mon): Headline inflation likely increased in December and crossed the 3% upper bound of the Czech National Bank's tolerance band, driven by more substantial annual food price growth and a softer annual price decline of fuel. The annual dynamic in both categories is partially affected by a low comparison base from the preceding year. Core inflation is estimated to have remained unchanged in December, while price growth in the regulated segment has softened only slightly.

Retail sales (Mon): Real retail sales growth likely softened in annual terms in November, though it remained on a solid footing, with consumer spending still driving the economic rebound throughout the year-end. With continued robust real wage growth, households are filling the consumption gap from the preceding high-inflation years.

Current account (Mon): The malaise in European industry has limited Czech export growth. Meanwhile, imports received a boost from pre-Christmas restocking, implying a less buoyant current account surplus in November than previously. However, despite the weak foreign demand from the main European trading partners and elevated competition, producer prices likely accelerated in December, reflecting increasing natural gas prices and a weaker koruna against the dollar.

Kazakhstan

Interest rates (Fri): The National Bank of Kazakhstan (NBK) will be deciding on the key rate on Friday. Following the unexpected 100bp hike to 15.25% at the last meeting, the choice would be between holding and hiking further, as suggested by the communique. At this point, we believe in a wait-and-see approach as the year-end CPI reading of 8.6% YoY was well within the 8-9 official forecast range, preliminary economic activity data is also in line with expectations, while the exchange rate depreciation, which could have contributed to the previous key rate hike, seems to have been addressed by regular and emergency FX sales by the central bank.

Meanwhile, a further 50bp hike could be an alternative option worth considering, especially if the fiscal discipline remains lax, while inflationary expectations by households and corporates continue to grow, as was the case in the previous month. In any case, we expect the tone of the NBK's commentary to remain cautious, stressing the long road ahead before reaching the long-term CPI target of 5% for Kazakhstan.

Key events in developed markets next week

Source: Refinitiv, ING

Key events in EMEA next week

Source: Refinitiv, ING

Read the original analysis: Think ahead: Mixed inflation data

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.