Think ahead: Huddle – We need to talk about the fifth quarter

James Smith reckons American football offers the perfect analogy for central banks. Only problem? He hasn’t the foggiest idea how the sport works. Take a time out, grab yourself a corndog and read on as he and the rest of the team look ahead to another important week for financial markets.

Think ahead: The fifth quarter

As an Englishman, I confess I’ve always been baffled by American football. Why does the game have so many stoppages? And why isn’t the ball round? I just can’t get my head around the rules, though I accept that’s a bit rich coming from the nation that gave the world cricket and rugby…

Even I must concede, however, that the game offers us an excellent analogy for central banks this year: a game of four quarters. Hang on, isn't that baseball?

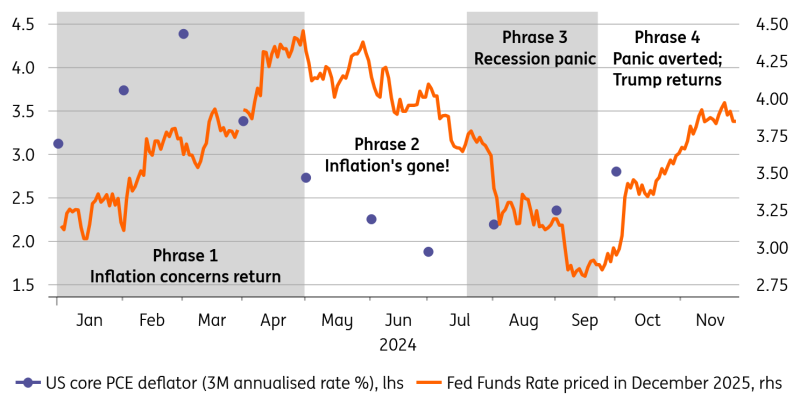

Anyway, check out the chart below. 2024 can be divided into four distinct periods of varying levels of concern about inflation and the jobs market. Remember when markets were briefly pricing an emergency Fed rate cut at the start of August? Just like the rate hike cycle that came before, it’s a reminder that these rate-cutting processes rarely follow the nice straight lines us economists like to draw into the future. I could just as easily draw a chart like this for the European Central Bank.

Chart of the week: How Fed expectations have developed this year

Source: Macrobond

It begs the question, what does the proverbial 'fifth quarter' look like? I say proverbial like I have any idea whether it’s a thing or not…

In the Fed’s case, most roads lead back to Trump. His strident tariff threats against Mexico and Canada this week are a reminder to central bankers in Washington: you can’t blissfully ignore his policy agenda for much longer. Incidentally, Chris talks about the effect of it all on FX markets here. A slower pace of cuts looks likely, and as James K explains below, next week’s jobs numbers will tell us whether or not the first pause comes in December or January.

Life’s rarely that simple, though, and remember the jobs data isn’t exactly giving us a clean read of the situation. I can sympathise; here in the UK, our dubious jobs figures might not get fixed until 2027, according to a recent Bloomberg story.

The recent US hurricanes don’t help, though recent state-level data showed that the weather can’t explain all of October’s weakness. Remember too that the American data is systematically overstating job creation on account of some questionable assumptions about the number of smaller companies being created or destroyed. Downward revisions are surely coming.

A blitz of unwelcome surprises on the US jobs market, regardless of Trump’s policy agenda, is perhaps the most obvious downside risk for early 2025.

The same is true of Europe, though the mere fact that the ECB is toying with a 50 basis-point cut in December tells us that weaker growth is already firmly on the radar. Whether the ECB actually follows through with that bigger cut is less clear.

On the face of it, the European jobs market looks decent. Monday’s figures are expected to show the unemployment rate close to its all-time low. The ECB’s wage figures, though volatile, are above 5%.

It’s therefore unsurprising that the hawks are mounting what we NFL aficionados would call a 'two-minute drill': a fast-paced strategy at the end of the half. Halves? This is all getting terribly confusing…

Anyway, as Carsten Brzeski writes, this week’s modest rise in German inflation and more resilient confidence data will bolster the hawk’s 'dee-fense', as the Americans would say, of a 25bp cut in December.

But the true fight, as hawkish-quarterback Isabel Schnabel’s interview this week demonstrated, is really about how low the ECB takes rates next year. Schnabel spoke of the inflationary risks from Trump's economic policies. Carsten is less convinced and points to the German jobs market, which is looking weaker and hints that lower wage growth is coming. That means the doves are likely to be in the ascendency next year, and that’s why he thinks the ECB will take rates below 2%.

We’ll have more to say about 2025 and plenty more besides in our global economic outlook, hitting your screens next week. We're doing a webinar, too, on 9 December. So grab yourself a corndog and sign up here.

Until then, you’ll be pleased to hear it’s 'end of regulation' for this week. That means game over, apparently. I need a huggle.

Think ahead in developed markets

United States (James Knightley)

Labour market (Fri): The market remains split on whether the Federal Reserve will cut interest rates 25bp at the upcoming meeting on December 18 after inflation came in hotter than hoped. The Fed’s dual mandate, whereby it also has to maximise employment, is critical to the current debate, and in that respect, next week’s jobs report will be the clear focus. Last month’s 12k outcome for non-farm payrolls was considerably weaker than expected. State data shows that Hurricane Milton had a negative influence. Florida employment fell 38k in October relative to its six-month trend growth of 13k. This allows us to approximate that the hurricane effect depressed Florida payrolls by around 51k. There was some minor impact in the Carolinas and Virginia, so we can perhaps round that to a 60-65k impact from the hurricane. We also know that strike activity, predominantly at Boeing, subtracted 44k. All of these factors will reverse in next Friday’s report with these impacted people returning to work. This means we have 109k as a base for November before we consider any actual payrolls growth. We forecast headline payrolls growth of 225k, but given that 109k of this is the technical rebound, it implies "true" payrolls growth of just 116k (225k-109k). If that is correct, the Federal Reserve is likely to cut interest rates again in December, especially if the unemployment rate ticks up to 4.2% as we expect.

Think ahead for Central and Eastern Europe

Poland (Adam Antoniak)

Central bank rate (Wed): Inflation is well above the National Bank of Poland's (NBP) target and is still expected to trend upwards in the first quarter of 2025, so the MPC will keep rates unchanged in December. At Thursday’s press conference, the NBP governor, Adam Glapiński, is likely to declare that the outlook for monetary policy is broadly unchanged, even though the electricity price freeze is set to be extended through the majority of 2025. The Council is unlikely to start discussing rate cuts before it puts together its March 2025 projections.

Hungary (Peter Virovacz)

Economic activity (Tue/Thu/Fri): Next week will be all about economic activity in Hungary. On the one hand, we will finally get the details behind the surprisingly bad third quarter. We are betting on a big drag on GDP growth (Tue) from investment activity and perhaps a slowdown in consumption growth. For those who prefer to look ahead rather than in the rear-view mirror, we have the first batch of Q4 data. We expect a rebound in retail sales (Thu) due to some post-flood recovery, while industrial production (Fri) will continue to decline in line with the recent trend.

Czech Republic (David Havrlant)

PMI (Mon): The November manufacturing PMI likely fell after the previous uptick, with industry factoring in more uncertainty regarding potential tariffs from the new US administration. At the same time, we don't expect any panic-driven downturn in industrial confidence, given the Czech automotive sector doesn't seem to be dealing with the havoc in European industry too badly.

Wages (Wed): Real wage dynamics remained solid in the third quarter. Nominal wage growth softened only slightly, while consumer inflation also decelerated over the same period. Robust real wage gains will motivate consumers to continue doing what they do best.

Consumers (Fri): Meanwhile, annual growth in real retail sales likely slowed in October, partially due to a strong figure in the previous year. However, the consumer remains in good shape, supported by real wage increases, and is about to drive the recovery in the coming quarters.

Turkey (Muhammet Mercan)

Inflation (Tue): Despite temporary volatility, the Lira has outperformed other EM peers in November. Given this backdrop, in addition to the ongoing effect of monetary tightening, we expect the downtrend in the annual inflation to continue with a drop to 46.6% (forecasting a 1.9% MoM increase) from 48.6% a month ago.

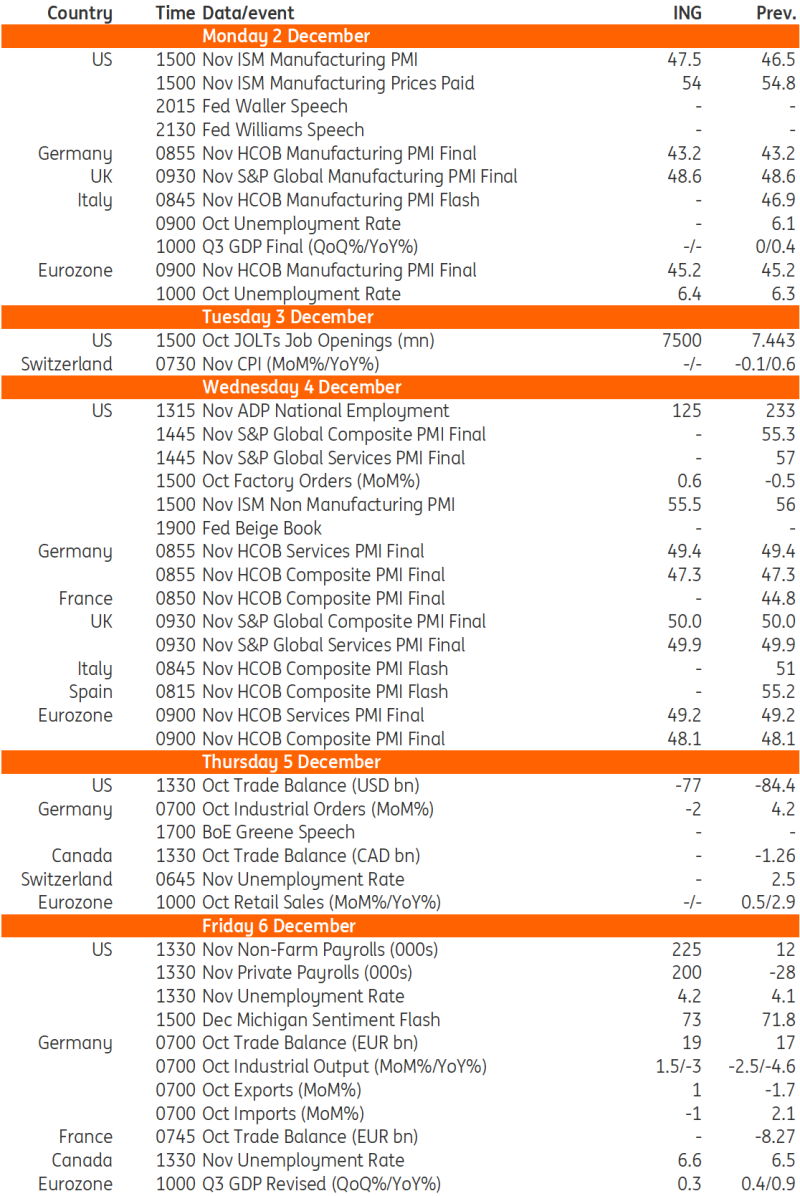

Key events in developed markets next week

Source: Refinitiv, ING

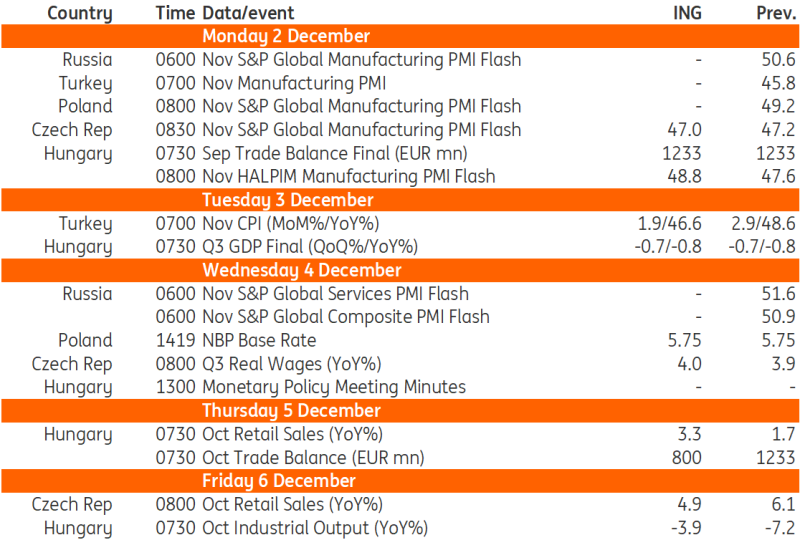

Key events in EMEA next week

Source: Refinitiv, ING

Read the original analysis: Think ahead: Huddle – We need to talk about the fifth quarter

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.