There is really no Gold/Silver disconnect

It might seem like silver is too overvalued in comparison to gold. But this is not true. Both of the precious metals are fairly valued relative to each other. Moreover, neither silver nor gold is too overvalued relative to stocks. In this analysis I will explain why both gold and silver valuations are not excessive.

Gold’s and Silver’s rallies

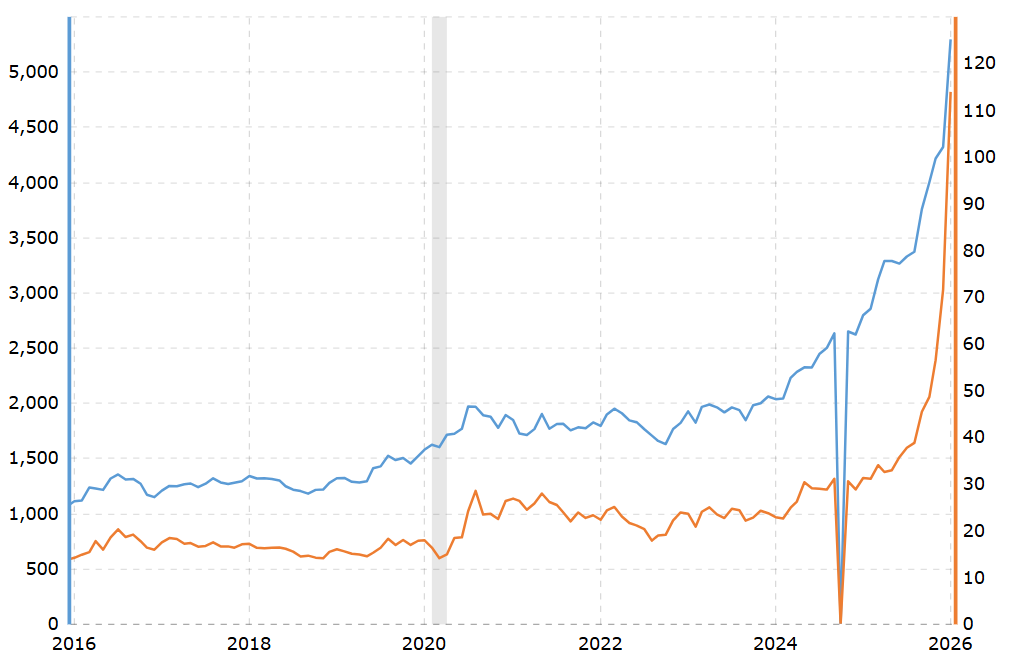

Some analysts might now say that gold is now cheap relative to silver, while both metals are now ridiculously expensive. It is true that both gold and silver prices have soared. This can be seen from the diagram below.

Historical Gold (blue) and Silver (orange) prices

At the same time, from the diagram above it seems clear that gold prices’ rise was much more even than silver’s meteoric surge even though both of these metals have recently performed fantastically. But it is not true that we are facing either gold or a silver bubble because the two metals have fundamental reasons to rally further.

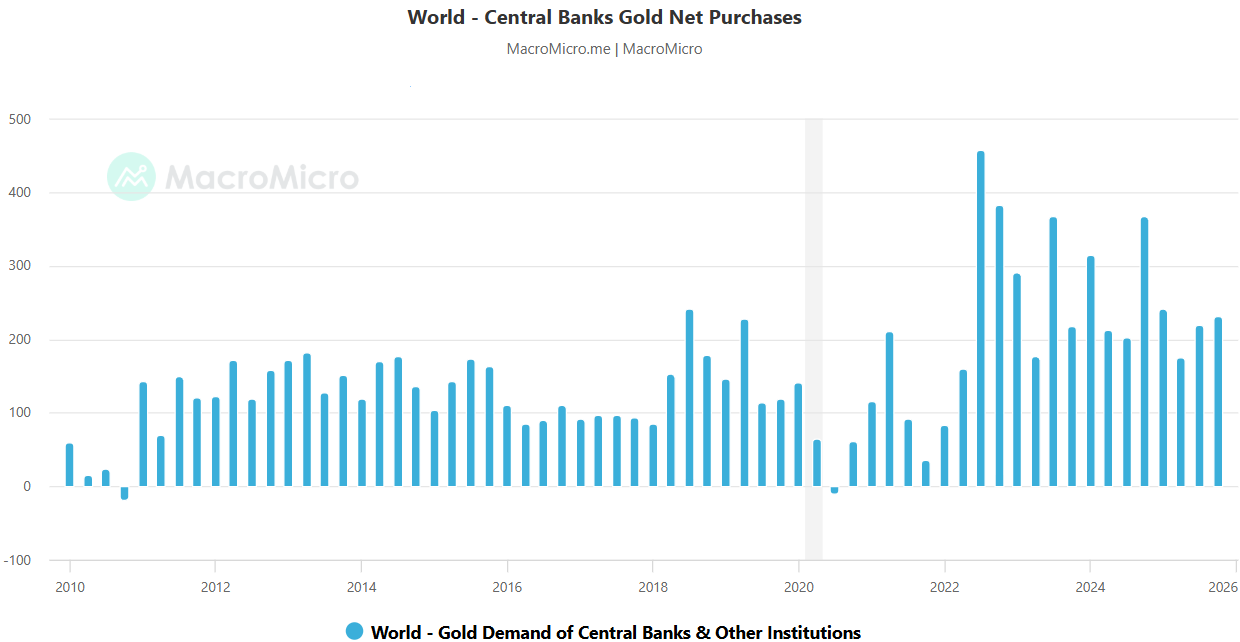

As concerns gold, it plays a crucial monetary role. The yellow metal has historically been used as money. Moreover, central bankers use gold to store it in vaults as foreign reserves. For several years already have major central bankers been actively raising their gold purchases.

This can be easily seen from the diagram below showing central bankers’ net gold purchases.

It was recently announced that President Trump nominated Kevin Warsh, an ex-Fed governor, for the role of the Fed’s chair. This made both gold and silver plunge somewhat on Friday because Kevin Warsh has the reputation of a “hawk” – in other words he considers inflation to be the Fed’s top priority, even more important than maintaining high employment numbers. But as I have mentioned in my other article, the US macroeconomic indicators suggest that more monetary easing may be ahead. Obviously, the Fed’s easing does not only involve decreasing the interest rates. It involves raising the money supply by quantitative easing (QE), which is inflationary and good for the precious metals. High demand for gold co-exists with its scarcity as I have mentioned in my other article.

As concerns silver, there is high industrial demand for it due to the need to build AI infrastructure, produce EVs and solar batteries all of which require a lot of silver. The supply of it is highly limited because silver is only available as a byproduct of mining other metals, including copper and zinc. Plus, just like for gold there is also investment demand for silver. So, the demand for the grey shiny metal also depends on the money supply and the Federal Reserve.

At the same time, silver is more critical for industrial uses than gold. Moreover, it is also much more volatile than gold due to the fact that silver markets are much tighter compared to gold’s simply because gold is much more often used as an investment asset. So, there is more portfolio allocation to gold. Simultaneously, there is much less physical gold – already mined or in the form of proven underground reserves – than physical silver. Gold is still a necessary component of the modern monetary system. It is in some cases viewed as an alternative to fiat currencies. For example, many central bankers nowadays prefer to store their countries’ national strategic reserves in the form of physical gold rather than the Euro or the USD. This is especially true of BRICS+ members – Brazil, Russia, India, China and South Africa – that have complicated relations with the collective West, namely the USA and Europe. But despite this strong demand from central bankers, silver still has appreciated much more than gold. But it is quite reasonable, given the high industrial demand and the lacking supply of silver. Moreover, as I have mentioned above, silver has always been much more volatile than gold.

Valuations

But is silver really so overvalued in relation to gold? A few valuation graphs below show us the valuation ratios for both precious metals.

The first one shows the relationship between gold and silver, it is the so-called gold-to-silver ratio. As can be seen from this diagram, it is substantially below its peak – when gold is very expensive relative to silver - and off its lows – when silver is expensive relative to gold. In other words, silver is fairly valued relative to gold.

Gold-to-Silver ratio

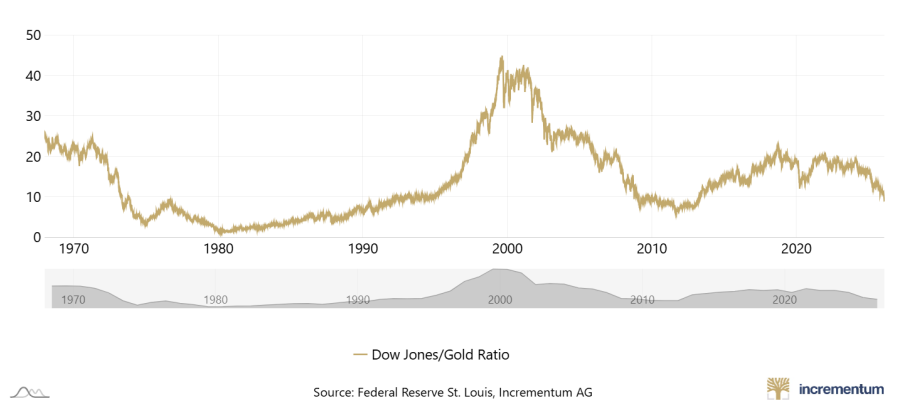

But how expensive are Gold and Silver relative to equities?

As can be seen from the diagram below, the Dow-to-gold ratio is close to average, meaning that it is neither too high – when stocks were highly overvalued to gold – like it was in 2000 during the Dot.com bubble, nor too low – when precious metals were too expensive relative to stocks – like they were in 2011 when both gold and silver touched their record highs.

Dow-to-Gold ratio

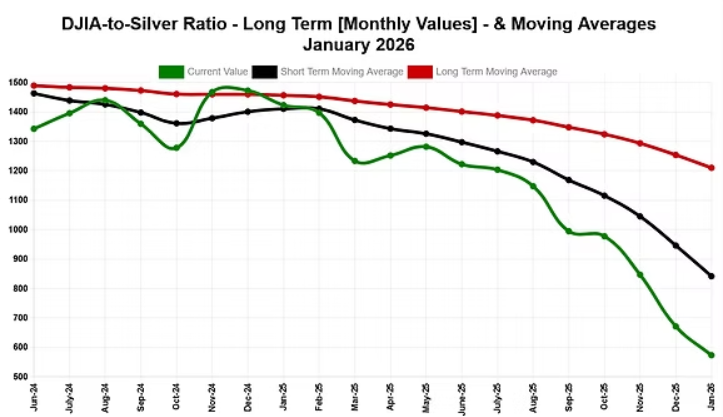

Below you could see a graph showing the relationship between Dow and silver prices.

Dow-to-Silver ratio

It is true that the ratio has been falling substantially and is now below 600, meaning that in order to buy one share of the Dow Jones index, only 600 ounces of silver are needed. It might seem like silver has become expensive relative to the Dow Jones index.

However, the Dow-to-Silver ratio has been showing very high volatility. Over the last 100 years it has been ranging from under 20 – when silver was very expensive relative to Dow - to more than 2,500 – when Dow Jones was highly overvalued relative to silver. On average, the ratio has often operated below 1,000. Only in several recent years has it operated higher than 1,000. The point I am making is that the 600 ratio we are having now, is quite average compared to where it used to be, meaning that both stocks and silver are quite expensive but fairly valued relative to each other.

Conclusion

In conclusion, I would say that neither gold, nor silver are expensive relative to each other. So, there is no gold/silver price disconnect. Moreover, neither gold, nor silver look expensive relative to stocks. As concerns their recent rallies, I would say that there were fundamental reasons for them.

Author

Anna Sokolidou

Independent Analyst

A research analyst, a freelance finance writer and an economics teacher looking for interesting investment opportunities. I have been investing for years. I am mostly interested in writing about commodities, precious metals and large corporations.