The Yen problem Japan’s rate hike couldn’t solve

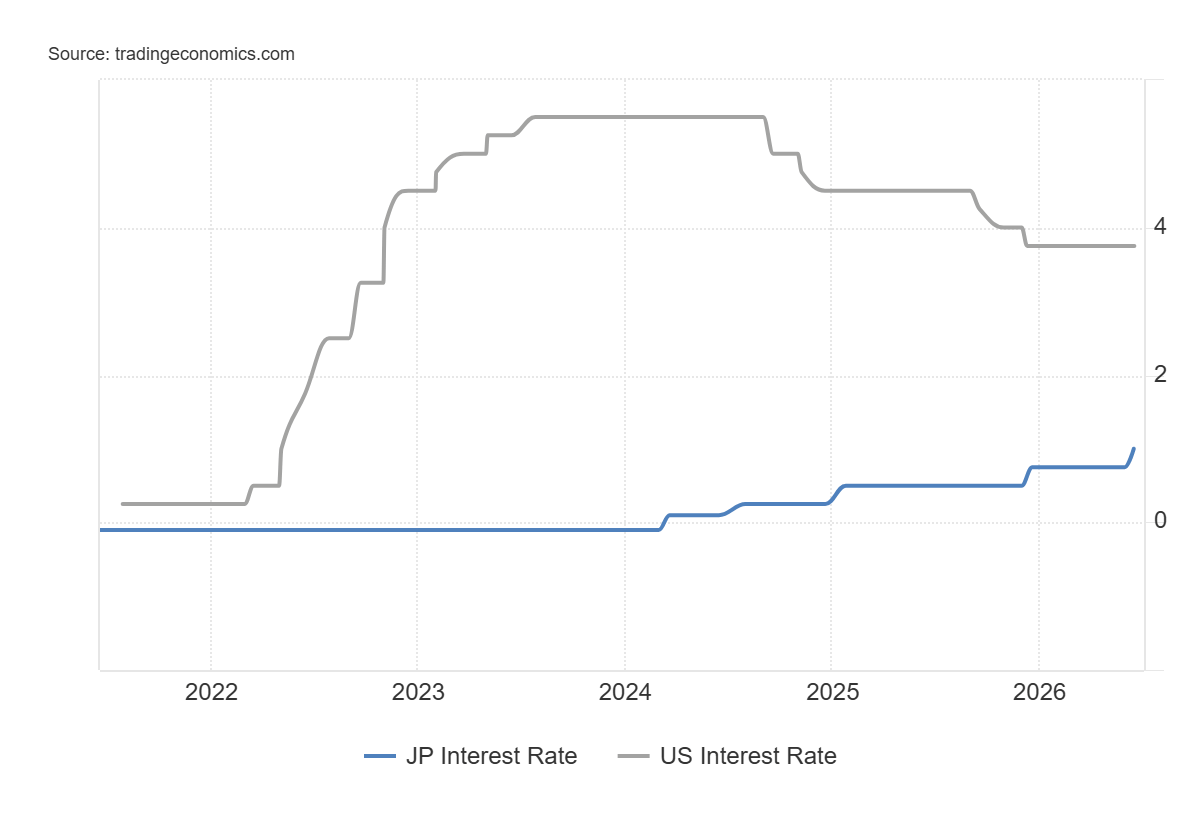

The Bank of Japan (BoJ) finally delivered what Yen bulls spent years asking for. On June 16, policymakers raised interest rates to 1%, the highest level since 1995 and a milestone few thought possible only two years ago. Yet the Japanese Yen (JPY) barely reacted.

USD/JPY remains near 162, a level that puts the currency close to its weakest point in nearly four decades. Tokyo has already spent roughly ¥11.7 trillion ($73 billion) defending the Yen this year, Oil prices have retreated sharply from their war-driven highs, and Japan has finally abandoned negative rates. None of it has changed the trend.

The question is no longer why the Yen weakened. The question is why nothing seems capable of stopping it.

Although the chances of intervention remain high, a wide interest rate gap between the US and Japan should keep the so-called JPY carry trade in play. This, along with Japanese Prime Minister Sanae Takaichi’s reflationary stance, might continue to weigh on the Yen.

Expected BoJ rate hike fails to lift JPY

In theory, a central bank raising interest rates should support its currency.

The BoJ’s move to 1% marks Japan’s highest rate since 1995. The problem is that currency markets care less about absolute rates than relative rates. In Japan’s case, domestic borrowing remains substantially lower than in the US. In fact, the US Federal Reserve (Fed) maintained its interest rate target range of 3.5% to 3.75% at the end of the June meeting.

That still leaves a gap of roughly 250 basis points in favor of the United States.

For global investors, the arithmetic remains simple: borrow cheaply in Yen and buy higher-yielding Dollar assets.

The $73 billion warning

Meanwhile, authorities have allowed the JPY to weaken above the 160 psychological mark against the USD since early June, raising doubts about Tokyo's appetite for a new intervention. Moreover, repeated warnings about decisive action reduce the element of surprise and, by extension, the effectiveness of any intervention.

Japan already spent a historic ¥11.7 trillion (nearly $73 billion) defending the currency between April and May, yet the impact proved short-lived as the Yen soon resumed its decline.

The episode reinforced what many investors already suspected: intervention alone is unlikely to change the trend while the US-Japan interest-rate gap remains so wide.

Fiscal concerns keep weighing on the Yen

Further, Japan’s heavy reliance on imported energy during a period when the Middle East crisis pushed Oil prices to multi-year highs proved to be another factor pressuring the Yen. That said, crude prices have retreated significantly following the interim US-Iran peace deal and the resumption of shipping activity through the Strait of Hormuz.

Yet the relief has done little to revive bullish sentiment toward the Japanese currency. Investors remain focused on the broader fundamental picture, particularly Japan’s worsening fiscal outlook and the wide interest-rate gap with the United States.

Japan’s government gross debt-to-GDP ratio is roughly 250%, the highest among advanced G7 economies. Adding to this, Prime Minister Sanae Takaichi's unprecedented ¥370 trillion ($2.3 trillion) public-private investment plan, spread over 14 years, has fueled debate about the country’s long-term fiscal sustainability.

The issue is becoming increasingly relevant as the BoJ continues to normalize monetary policy. While higher interest rates could, in theory, support the Yen, they also raise borrowing costs for a government already carrying one of the heaviest debt burdens in the developed world. As a result, investors increasingly question how far the BoJ can tighten without adding pressure on Japan’s public finances.

Intervention might only bring a temporary relief

This, in turn, could overshadow any future government intervention.

While Tokyo remains uncomfortable with USD/JPY trading above 160, previous efforts have shown that intervention can slow the Yen's decline but struggle to reverse it when the underlying fundamentals remain unchanged.

At the same time, expectations that the BoJ will continue tightening only gradually may do little to alter the Yen's role as a preferred funding currency for carry trades. With US interest rates still substantially above Japanese rates, investors have little incentive to abandon the strategy.

As a result, the Yen could remain under pressure even if authorities step back into the market. Should the Federal Reserve deliver another rate hike later this year, USD/JPY may push beyond the 162.00 mark for the first time since 1986, testing Tokyo's resolve once again.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.