US Dollar Weekly Forecast: The Dollar rebuilds as the Fed doubles down on inflation

- The US Dollar clinched its second consecutive week of gains.

- Steady bets for Fed rate hikes lent support to the Greenback’s bounce.

- Markets’ attention now shifts to US NFP data and Warsh’s testimony.

The week that was

Another promising week for the US Dollar (USD). Indeed, the Greenback climbed to levels last seen in early May 2025 near the 102.00 barrier, as measured by the US Dollar Index (DXY).

The continuation of the move higher in the buck was propped up by rising bets that the Federal Reserve (Fed) might keep its cautious stance, or even hike rates, later in the year. This view gained particular momentum after the Fed delivered a hawkish message on June 17, during Kevin Warsh’s first meeting in charge.

However, the extra rebound in the US Dollar did not find an echo in the domestic money market, where US Treasury yields closed the week in the red across the spectrum.

Fed enters a 'new chapter'

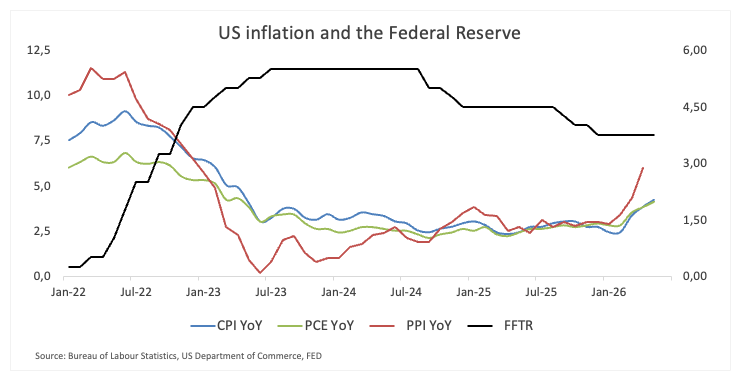

The Federal Reserve left interest rates unchanged at 3.50%-3.75% on June 17, but the updated economic projections delivered a distinctly hawkish message. Policymakers sharply raised their inflation forecasts, delayed the return to the 2% target until 2028 and lifted the projected policy rate path through 2028, reinforcing the view that interest rates are likely to remain higher for longer.

Chair Kevin Warsh echoed that message in his first press conference, stressing that restoring price stability remains the Fed's overriding priority. He also announced a broad review of the central bank's communications framework, balance sheet strategy and forecasting models, describing the changes as the beginning of a "new chapter" for the institution.

Officials reinforce the inflation message

Fed officials spent the rest of the week reinforcing the tone set at the June meeting. Chicago Fed President Austan Goolsbee acknowledged that inflation has recently been "going the wrong way," while arguing that persistent services inflation remains a greater concern than temporary increases driven by energy or goods prices. Although he pointed to some tentative improvement beneath the surface, he stressed that core inflation remains well above target and that price stability remains the Fed's primary challenge.

New York Fed President John Williams struck a similar tone, describing monetary policy as "well positioned" while reiterating that bringing inflation back to 2% remains imperative. He also acknowledged that recent inflation developments have pushed back the expected timeline for reaching that objective, while he maintained that the US economy and labour market continue to show resilience.

Taken together, this week's Fedspeak made it clear that the Committee remains firmly focused on inflation. Rather than debating when to ease policy, officials appear increasingly aligned around keeping rates restrictive until they see much clearer evidence that underlying price pressures are moving sustainably back toward the target.

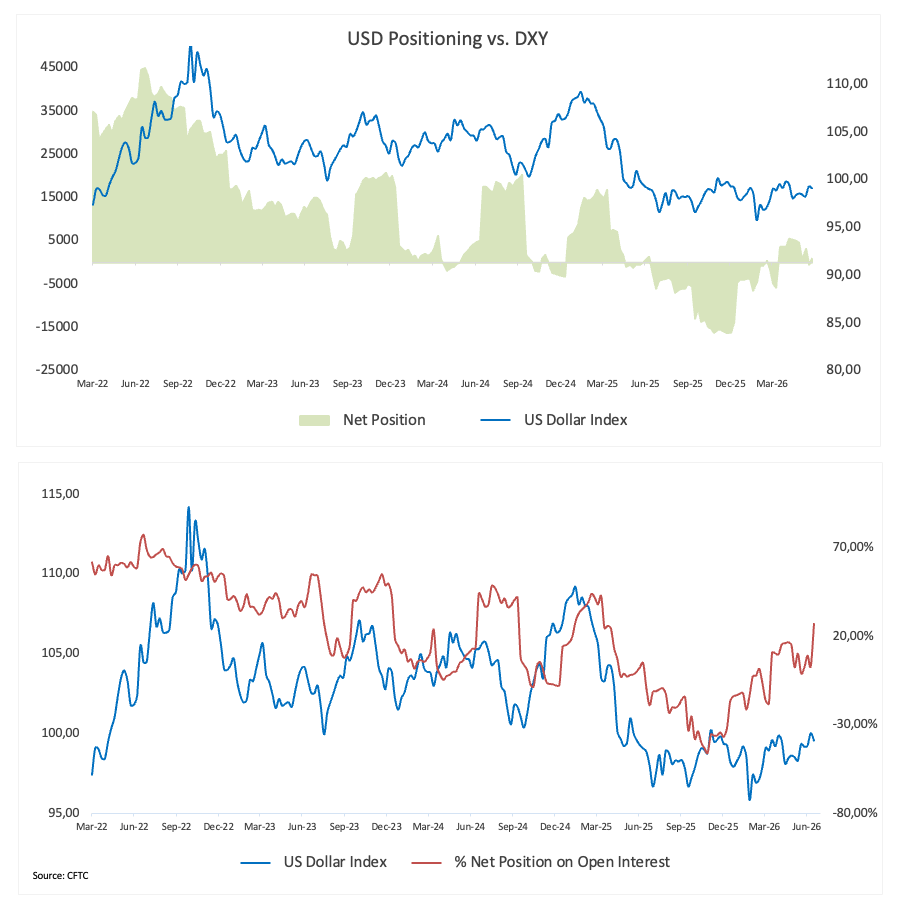

Dollar bulls return; positioning remains far from crowded

Latest Commodity Futures Trading Commission (CFTC) data show a new surge of speculative bullish sentiment towards the US Dollar, with net longs rising to 13.2K contracts in the week ending June 16, the biggest bullish stance since March 2025.

The increase was driven by an 11.8K-contract weekly rise in net positioning, while the four-week change stands at 13.7K contracts, suggesting investors have gradually been rebuilding long Dollar exposure over the past month.

Even so, the broader picture remains far from one of an overcrowded trade.

Although speculative positioning has turned more constructive, the current net long ranks in only the 57th percentile of its 5-year range. Likewise, the speculative exposure stands at 27%, placing it almost exactly in the middle of its recent historical distribution, with a 50th-percentile ranking.

In other words, traders are becoming more optimistic on the Greenback, but conviction still looks fairly measured by historical standards.

Open interest edged lower to 49.4K contracts from 50.3K the previous week, suggesting the improvement in net positioning was not driven by a broad influx of new participants. Instead, the move appears to be a signal of a slow change in sentiment among current market participants, rather than the start of an aggressive accumulation phase.

That distinction matters. When positioning rises while participation remains broadly steady or softens slightly, it often points to improving confidence rather than the kind of one-sided positioning that can leave a market vulnerable to sharp reversals.

To sum up

Non-commercial investors have become increasingly constructive on the US Dollar in recent weeks, pushing net longs to their highest level in more than a year. However, positioning still sits close to the middle of its five-year historical range, while exposure remains well short of crowded territory. For now, CFTC data suggest the Dollar's recovery is being accompanied by a measured rebuilding of bullish positions, leaving room for further accumulation should the macro backdrop continue to favour the Greenback.

Inflation refuses to fade

As widely expected, inflation picked up in May. Headline Consumer Price Index (CPI) inflation accelerated to 4.2% YoY from 3.8% in April, while core CPI, which excludes food and energy prices, edged up to 2.9% from 2.8%. This week's Personal Consumption Expenditure (PCE) report echoed that trend, suggesting underlying price pressures remain persistent.

The latest readings raise an uncomfortable question for both policymakers and investors: has the disinflation narrative that dominated the first part of the year already begun to lose momentum?

The answer is far from straightforward. Although the prolonged closure of the Strait of Hormuz briefly reignited inflation concerns by sending Oil prices sharply higher, last week's US-Iran agreement triggered a sharp reversal in West Texas Intermediate (WTI) prices, which receded toward the $68.00 mark per barrel, breaking below its key 200-day SMA and all but erasing the geopolitical war hype that had fuelled the earlier rally.

At the same time, the delayed effects of US tariffs are only now beginning to filter through supply chains and into consumer prices, suggesting some inflationary pressures may prove more persistent than initially anticipated.

Taken together, it is precisely the kind of backdrop markets were hoping to avoid: inflation proving stubborn just as the US “exceptionalism” narrative remains well and sound.

What comes next for markets?

Attention now shifts to next week's US labour market data, including the releases of JOLTs Job Openings, the job creation in the US private sector tracked by ADP, and the monthly Nonfarm Payrolls (NFP). In addition, the Institute for Supply Management (ISM) will publish its June Manufacturing gauge.

Beyond the data, investors will continue to track developments in the Middle East as well as comments from Fed officials and the testimony by Chair Kevin Warsh.

The market's Fed rethink

Until recently, investors operated under a relatively simple assumption: the Federal Reserve's next significant policy move would eventually be towards lower interest rates.

That assumption is becoming increasingly difficult to defend.

Sticky inflation, resilient economic activity, elevated energy prices and renewed supply-chain disruptions have all complicated the path back toward policy easing. More importantly, Fed officials no longer appear convinced that inflation will continue moving sustainably lower without monetary policy remaining restrictive.

None of these factors necessarily signals that another rate hike is imminent. It does, however, suggest that the bar for policy easing has risen considerably, while discussions about the possibility of further tightening have quietly returned to the conversation.

For the US Dollar, that shift matters. Expectations that interest rates will stay higher for longer should continue to underpin US Treasury yields and provide a supportive backdrop for the Greenback.

The Dollar's strongest ally: stubborn inflation

If recent months have taught investors anything, it is that bringing inflation down from very high levels is one challenge; eliminating the final leg of price pressures is another altogether.

That may be the US Dollar's greatest source of support in the months ahead.

Markets appear to have underestimated just how difficult the final stage of the inflation battle was always likely to be. As long as underlying price pressures remain stubbornly elevated, a prolonged period of restrictive monetary policy is likely to keep favouring the Greenback.

Nonfarm Payrolls FAQs

Nonfarm Payrolls (NFP) are part of the US Bureau of Labor Statistics monthly jobs report. The Nonfarm Payrolls component specifically measures the change in the number of people employed in the US during the previous month, excluding the farming industry.

The Nonfarm Payrolls figure can influence the decisions of the Federal Reserve by providing a measure of how successfully the Fed is meeting its mandate of fostering full employment and 2% inflation. A relatively high NFP figure means more people are in employment, earning more money and therefore probably spending more. A relatively low Nonfarm Payrolls’ result, on the either hand, could mean people are struggling to find work. The Fed will typically raise interest rates to combat high inflation triggered by low unemployment, and lower them to stimulate a stagnant labor market.

Nonfarm Payrolls generally have a positive correlation with the US Dollar. This means when payrolls’ figures come out higher-than-expected the USD tends to rally and vice versa when they are lower. NFPs influence the US Dollar by virtue of their impact on inflation, monetary policy expectations and interest rates. A higher NFP usually means the Federal Reserve will be more tight in its monetary policy, supporting the USD.

Nonfarm Payrolls are generally negatively-correlated with the price of Gold. This means a higher-than-expected payrolls’ figure will have a depressing effect on the Gold price and vice versa. Higher NFP generally has a positive effect on the value of the USD, and like most major commodities Gold is priced in US Dollars. If the USD gains in value, therefore, it requires less Dollars to buy an ounce of Gold. Also, higher interest rates (typically helped higher NFPs) also lessen the attractiveness of Gold as an investment compared to staying in cash, where the money will at least earn interest.

Nonfarm Payrolls is only one component within a bigger jobs report and it can be overshadowed by the other components. At times, when NFP come out higher-than-forecast, but the Average Weekly Earnings is lower than expected, the market has ignored the potentially inflationary effect of the headline result and interpreted the fall in earnings as deflationary. The Participation Rate and the Average Weekly Hours components can also influence the market reaction, but only in seldom events like the “Great Resignation” or the Global Financial Crisis.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.