The UK’s sovereign rating remains resilient, but risks are increasing

The UK’s sovereign rating has remained resilient to recent economic crises, underpinned by the country’s institutional strengths. But greater structural risks in the UK government bond market and a worsening public debt outlook are downside factors.

Scope Ratings (Scope)’s next scheduled publication date for the UK sovereign rating is 28 March. Any potential downside to the Stable credit Outlook would require the evidence of either: heightened risk to the resilience of sterling and/or gilt markets during crises; and/or a material increase in fiscal risks beyond those assessed in October 2024, when the agency last affirmed the UK’s sovereign credit rating.

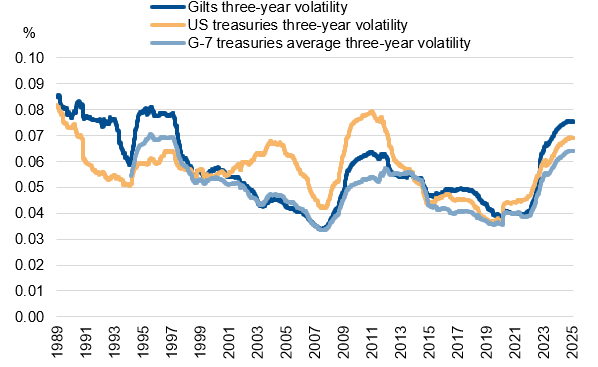

The recent sharp sell-off in gilts has underscored potentially greater sensitivities to market sentiment since the severe mini-budget crisis in 2022. From early December 2024 levels of 4.2%, 10-year gilt yields rose to post-financial crisis highs of 4.9% by mid-January. Although yields have since moderated slightly, the 10-year yield remains at the time of writing around 4.6% – above 2024 averages of 4.1%.

Global bond markets face increased volatility amid higher rates for longer

The fact that UK bond yields experienced the most pronounced rise among G-7 sovereign markets between December and January raises concerns. Gilts, traditionally viewed as a safe-haven asset and a stable store of liquidity and value, have faced disproportionate market sell-offs in recent times at the first signs of stress. This suggests greater risks for the sovereign borrower. The volatility of one-day changes in 10-year gilts has since 2022 exceeded that from 2008-09. However, this rise in volatility is not necessarily unique to UK markets and has rather been driven by the effects of the cost-of-living crisis on global sovereign risk.

Gilt market volatility has reached multi-decade highs

The rolling three-year standard deviation of one-day changes in 10-year yields.

Source: Macrobond, Scope Ratings calculations

Even so, the vulnerabilities of the UK government bond market have drawn some comparisons with riskier asset classes and with sovereign borrowers that do not necessarily enjoy safe-haven and reserve-currency privileges. These vulnerabilities are driven by the comparatively greater risk for the economy from inflation.

Greater hedge fund participation may contribute to the market dynamics

Nevertheless, changes in the investor base for UK government bonds are also potentially amplifying market dynamics. The rise in the outstanding volume of UK sovereign debt, especially since the pandemic crisis, has not been met by an equal increase in the capacity or appetite of commercial banks to absorb the new issuance. Without the Bank of England stepping in and making up for this disparity by purchasing through the Asset Purchase Facility (a trend in reverse since quantitative tightening), gilt markets have become increasingly reliant on hedge funds to bridge supply and demand gaps.

Hedge funds accounted for nearly 30% of gilt trades last year, nearly doubling their shares since mid-2018. The increased participation of highly leveraged funds has potentially accelerated gilt market swings during crises, reflecting their shorter holding horizons and lesser tendency for ‘home bias’. This may see the higher likelihood of holders of UK government debt today selling rather than holding or buying even more gilts during crises.

Factors such as this may undermine the resilience of the UK bond market. UK markets becoming more pro-cyclical during domestic or global crises rather than counter-cyclical may be a meaningful concern for the UK’s comparatively risk-free AA credit ratings.

Although the global use of Sterling has been little changed recently

To date, despite great challenges such as Brexit, holdings of global allocated reserves in sterling have seen little change in the recent years, standing at 5.0% as of September 2024. Cross-border lending in GBP, global payments in GBP in SWIFT and foreign-exchange turnover in sterling similarly remain comparatively unchanged recently.

The relative stability of sterling reserves has been an anchor of Scope’s UK sovereign credit ratings since they were first published in 2017. The AA credit rating has seen through-the-cycle stability despite the weakening of economic growth and budgetary performance.

Nevertheless, shifts in the global financial system, accelerated by the policies of the US administration, and the Global South opportunistically seeking to carve out an alternate global financial architecture centred around the renminbi and the rouble, pose greater long-run risks for currencies such as sterling.

The debt outlook on the United Kingdom increases risk

The UK has relied on its safe-haven status and the previous low-rates environment to support expansionary budgetary policies, but market dynamics today demand greater fiscal discipline. This requires balancing the government’s pro-growth policies with budgetary consolidation, including a tougher stance on current spending and/or higher taxes, especially given weaker economic projections, and re-instating confidence in the fiscal rules. Curtailing the budget deficit could help trim supply-demand mis-alignments in debt markets.

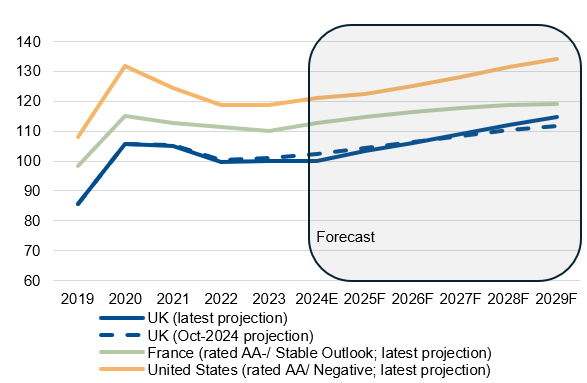

Risks take into account the continued rise of UK general government debt, which Scope Ratings forecasts reaching 114.8% of GDP by 2029, from 100.1% at end-2024. Net interest payments are projected to increase to 8.1% of general government revenue by 2029, a near tripling from 3.1% at the 2020 lows. The UK debt trajectory is slightly steeper than Scope’s October-2024 projections, as growth forecasts have been curtailed to 0.9% for 2025 and 1.3% next year, financing-rate assumptions have risen, and primary deficit-assumptions are slightly higher.

Nevertheless, compared with sovereign rating peers, the UK’s debt ratio remains moderately below that of France (rated AA- by Scope; government debt projected to increase to 119% of GDP by 2029), although UK debt is rising more steeply. UK debt also remains meaningfully below that of the United States (rated AA by Scope; debt reaching 134% by 2029).

Public-debt projections on the United Kingdom compared against those for select peer sovereigns

General government debt, % of GDP

Source: IMF World Economic Outlook historical data, Scope Ratings forecasts.

Author

Dennis Shen

Scope Ratings

Dennis Shen is Chair of the Macroeconomic Council and Lead Global Economist of Scope Ratings, the European rating agency, based in Berlin, Germany.