The stock market loves SpaceX, but the bond market isn’t so sure

Two weeks after the largest listing in market history, a company sitting on more than $100 billion of cash went to the bond market and borrowed $25 billion more. That is the fact to sit with. While the equity market bought a story, the bond market priced the risk: in the fortnight between the listing and the debt deal, those two prices stopped agreeing.

SpaceX (SPCX), the rocket and satellite group Elon Musk floated on Nasdaq on June 12, priced its initial public offering (IPO) at $135 a share and raised close to $86 billion with the over-allotment. It did not need the money. It borrowed anyway, and the terms it accepted say more about what this business is than the valuation the equity market has stapled to it.

The cash pile that still took out a loan

On paper the raise looks unnecessary. SpaceX disclosed about $100.8 billion in cash as of mid-June, and the bond proceeds are earmarked to repay a $20 billion bridge loan in full, cover fees, and leave the rest for general corporate purposes. The bridge is the interesting part: It was arranged earlier this year to fund the purchase of xAI, Musk's artificial intelligence (AI) startup, folding its compute ambitions onto the balance sheet the public now owns a sliver of.

Terming that short-term loan into 30-year paper is housekeeping. Doing that rather than write a cheque from the cash pile tells you management expects to be spending it for years.

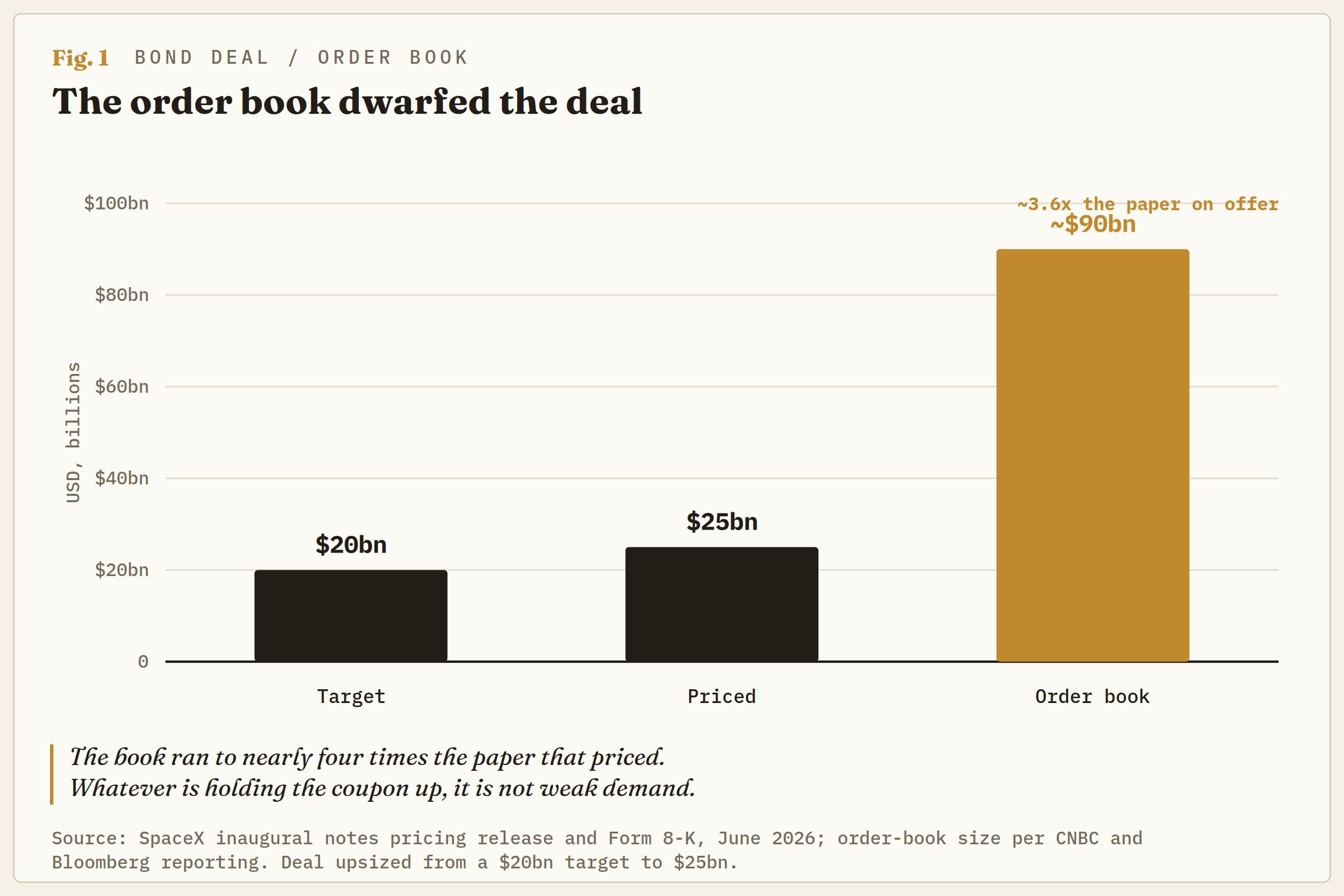

Demand was not the constraint. SpaceX targeted $20 billion and lifted the deal to $25 billion on roughly $90 billion of orders, one of the biggest debt sales of the AI era, alongside the Oracle, Amazon and Alphabet raises this year. The question is what the buyers are underwriting.

Two prices for the same bet

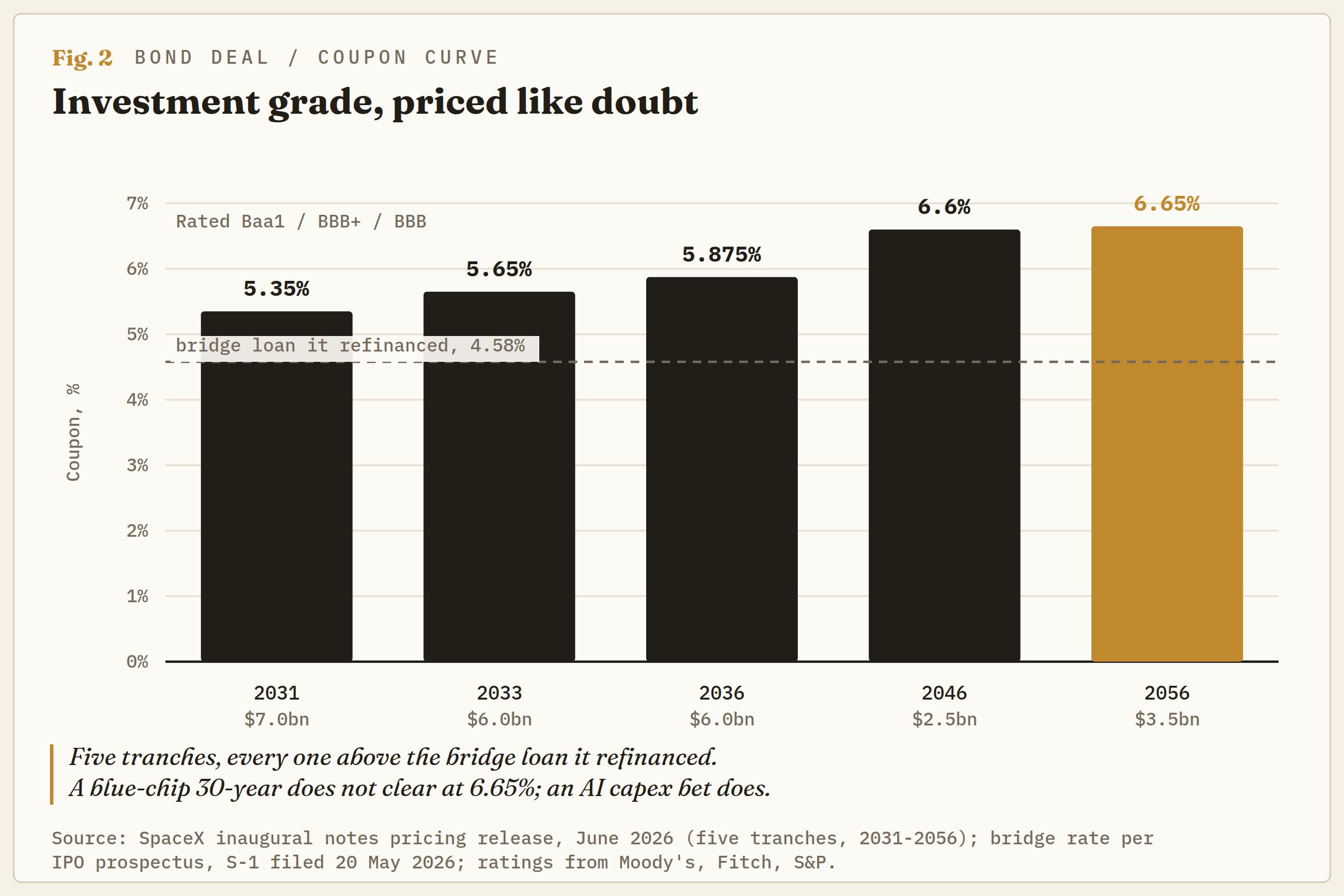

Start with the coupons. SpaceX priced five tranches maturing between 2031 and 2056, with rates climbing from 5.35% on the shortest to 6.65% on the longest. Those are investment-grade notes, rated Baa1 at Moody's, BBB+ at Fitch and BBB at S&P. They are also priced like a company the market is not sure about. A blue-chip 30-year does not clear at 6.65%; an AI infrastructure bet running a net loss and years of negative free cash flow does.

The ratings show where the confidence sits, and where it does not. All three agencies hung the investment grade almost entirely on Starlink, the connectivity unit that is the only dependable cash engine in the group, now past 12 million subscribers. The rockets and the orbital compute build are the story; Starlink pays the interest. S&P still projected negative free cash flow through 2029. That is the sober version of the company the equity market values near $1.75 trillion on what comes after Starlink.

Which is why the debt does not diversify the equity; it duplicates it. Owning the stock and the bonds together is not a balanced position. It is, in the words of Post Oak Group's Christopher Della Fave, "the same execution risk across two instruments." Starlink has to scale and Starship has to work, or both legs come under pressure together.

The tape has already sensed it. On June 18, the day the investment-grade ratings landed, the stock fell close to 4%. Good news for the credit was not good news for the equity, because the two are pricing different things.

The forced bid the rules were built to shrink

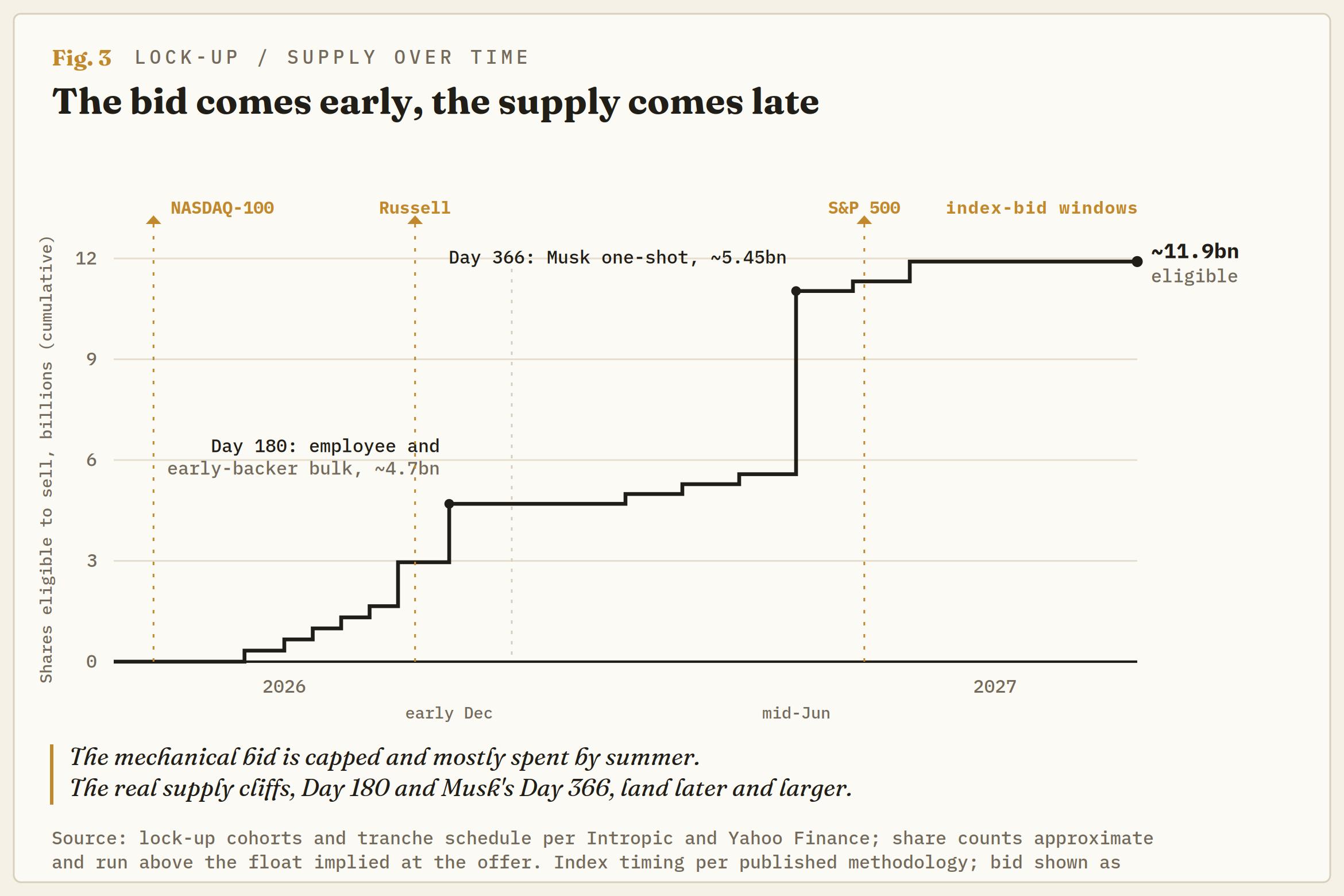

The other half of the bull case was mechanical, and it has quietly shrunk. The pitch was simple: A $1.75 trillion company floating only about 4% of its stock would drag index funds into buying whatever traded, at any price, the moment it qualified. That trade is smaller and later than advertised, for reasons written into the index rules this spring.

S&P rejected a fast-track proposal on June 4, so entry into its flagship index stays behind a 12-month seasoning bar and a profitability test SpaceX cannot currently pass, pushing the largest single wave of passive buying into 2027. The NASDAQ-100 does have a new fast-entry route, and SpaceX is on track to enter through it in early July, roughly 15 trading days after listing.

However, the same rule change capped how much index funds must buy: A low-float name is now weighted on the lesser of its full value or three times its floated shares, which throttles the exact demand the scarcity was supposed to unleash. The near-term mechanical bid runs to the low-to-mid $20 billion, not the flood the float implied, and it is funded by passive managers selling down the rest of the NASDAQ-100 to make room.

The tape already ran the round-trip

You do not have to model any of this, because the market already ran the experiment. In its first days the stock ripped to the mid-220s, up better than 60% from the offer, on retail frenzy, an options market live within days, and front-running of an inclusion that had not yet happened. Then it round-tripped the entire move, printing a low at exactly $135, the IPO price, by late June, before the NASDAQ-100 add even arrived. Buy the rumour, sell the news compressed its whole cycle into two weeks.

The stock has since clawed back towards the mid-160s and is probing the $175 area, roughly 130% of the offer. That level is not arbitrary: It is the same threshold that arms an early-release trigger in the lock-up, and about where inclusion front-running would be expected to peak. The $135 IPO price is the line in the sand beneath it, and it has already held once on the round-trip. Between the two, it is a range, not a trend.

The calendar is where the risk sits, and it is skewed the wrong way for longs. The forced bid is capped and mostly spent by summer; the supply is uncapped and lands later. The 180-day lock-up expiry falls around early December, freeing the bulk of the employee and early-backer float into a market whose passive tailwind has already blown through, with Russell reconstitution in the same window.

Musk's own stake sits behind a 366-day lock with no early release, and the institutional holders unlock in tranches through 2027. The bid comes early and small; the paper comes late and large. The lean is to fade rallies into the $175 zone rather than chase them, and to respect $135 as the level that decides whether this is healthy consolidation or the start of a longer bleed.

What the bond market already answered

So, what is SpaceX really selling? To the equity market, a $1.75 trillion claim on rockets, satellites and an orbital compute business that mostly does not exist yet. To the bond market, a Baa-rated cash-burn story that has to be paid 6.65% to hold the long end.

Both are looking at the same company, the same Starlink cash flows, the same Starship that either works or does not. One of them is being asked to believe a great deal more than the other. The debt already showed its hand; the equity is still deciding whether to blink.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.