The market may no longer be giving the Magnificent Seven a free pass

For much of the past three years, investing has felt surprisingly simple.

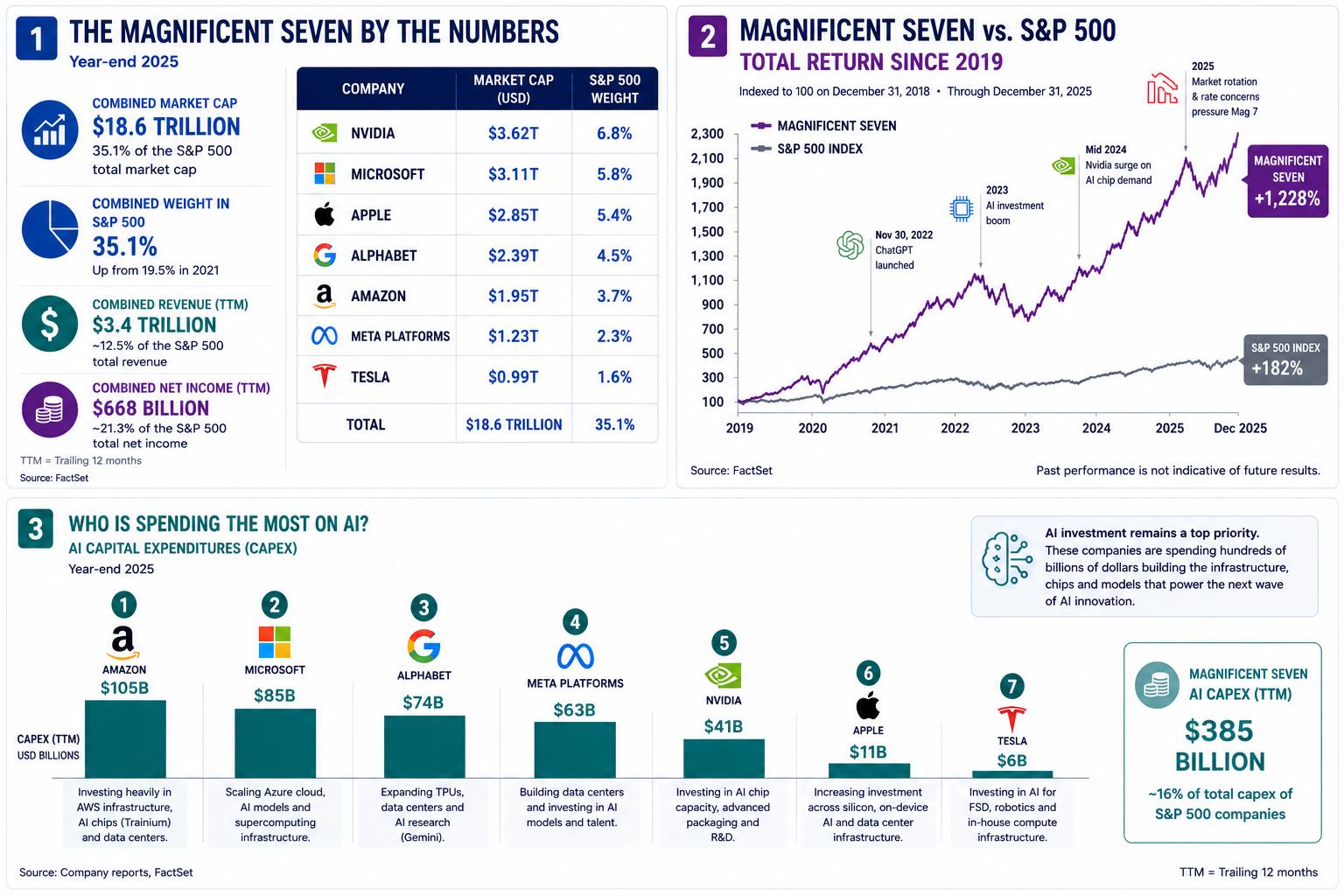

Whenever markets stumbled, investors knew where to look. Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta and Tesla repeatedly led Wall Street higher, shrugging off inflation fears, higher interest rates and geopolitical shocks. Together, the so-called Magnificent Seven became the face of the artificial intelligence boom and the engine behind one of the strongest rallies in modern market history.

Now, however, this dominance is being tested.

A broad sell-off across several of the group's biggest names has reignited a debate that many investors had almost forgotten how to have. Is this simply another pullback in a long-running bull market, or are the companies that have dominated global equities finally entering a more challenging phase?

The answer may shape the direction of markets for years to come.

Why this time feels different

Technology stocks have experienced plenty of corrections before, but this one carries a slightly different tone.

In previous sell-offs, investors were largely reacting to external events. Rising interest rates, stubborn inflation or geopolitical tensions temporarily pushed money away from growth stocks before confidence eventually returned.

This time, the questions are becoming more fundamental.

Can artificial intelligence continue generating the extraordinary earnings growth investors have come to expect? Will hundreds of billions of dollars being invested in new data centres eventually translate into stronger profits? And perhaps most importantly, have expectations simply become too high?

That shift in focus matters.

Markets are no longer questioning whether these companies are exceptional businesses. Instead, they're asking whether even exceptional businesses can continue outperforming after years of spectacular success.

Great companies can still become expensive stocks

One of the oldest lessons on Wall Street is also one of the easiest to forget.

A great company doesn't automatically make a great investment.

Few would question the quality of the Magnificent Seven. Collectively, they generate trillions of dollars in annual revenue, produce enormous cash flows and continue investing heavily in technologies that are likely to shape the global economy for years to come.

Yet success comes with its own challenges.

The group now represents roughly a third of the S&P 500's total market value, giving it an influence over global equity markets unlike almost anything seen before. Their combined market capitalisation runs into tens of trillions of dollars, meaning their earnings reports can move entire indices rather than just individual stocks.

In many ways, the Magnificent Seven are no longer competing against one another.

They're competing against the extraordinarily high expectations investors have placed upon them.

That means even strong earnings can trigger disappointing share price reactions if they fail to exceed already ambitious forecasts.

Is the AI boom losing momentum?

Probably not.

Artificial intelligence remains one of the biggest technological transformations in decades. Companies continue spending aggressively on chips, cloud infrastructure and data centres, while demand for AI-powered services shows few signs of slowing.

The challenge isn't the technology, it's the timeline.

Investors are asking more and more when these massive investments will start to deliver returns that justify their expense. Markets have happily rewarded companies for leading the AI revolution, but they are becoming more demanding about seeing tangible financial benefits rather than promises of future growth.

That isn't necessarily a bearish signal. It's what often happens when an emerging technology begins moving from excitement to execution.

Have the Magnificent Seven become victims of their own success?

Perhaps that's the more interesting question.

History suggests that every bull market eventually broadens: the dominant companies of one cycle rarely disappear overnight, but they often stop outperforming as leadership gradually spreads across different sectors of the economy.

That doesn't mean that Apple or Nvidia will suddenly become poor businesses. Nor does it mean artificial intelligence was simply another market fad. It may simply reflect a market becoming more selective.

As companies grow larger, maintaining the same pace of expansion becomes increasingly difficult. Expectations rise alongside valuations, leaving less room for error and making every earnings report a bigger test than the last.

What investors should watch next

Rather than focusing on day-to-day share price swings, investors would probably be better served watching the fundamentals.

- Can earnings continue growing fast enough to justify premium valuations?

- Will AI investments begin generating stronger profits and free cash flow?

- Can profit margins remain resilient despite record levels of capital spending?

- And, finally, does the next phase of market leadership continue revolving around the same seven companies, or does it gradually broaden to include other sectors that have largely remained in their shadow?

Those questions are likely to matter far more than whether the next trading session finishes in the red or the green.

All in all

It would be premature to declare the end of the Magnificent Seven. These remain some of the world's strongest businesses, with dominant market positions, enormous financial resources and a central role in what could become one of the most important technological shifts of the century.

But markets evolve.

The recent sell-off may ultimately be nothing more than another buying opportunity. Equally, it may mark the beginning of a more mature phase of this bull market, one in which investors become less willing to pay any price for future growth.

The Magnificent Seven haven't stopped changing the world. The market is simply becoming more demanding about how much it's willing to pay for that promise.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.