The nexus between price stability, financial stability and fiscal sustainability (Part 2)

Traditionally, monetary policy focuses on price stability and fiscal policy on other objectives. When inflation is well below (above) target on a sustained basis, this separation of roles implies that monetary policy may need to become extremely accommodative (restrictive). Consequently, interest rates have a large cyclical amplitude, which may have undesirable consequences for the economy and put financial stability at risk. Simulations show that a coordinated approach between monetary and fiscal policy reduces the optimal cumulative amount of rate cuts (hikes). However, putting this into practice would probably be very challenging.

Last week’s editorial of EcoWeek concluded that, given the interactions between price stability, financial stability and fiscal sustainability, it is important that each policy -monetary, fiscal, financial stability oriented- is conducted in a way that takes into account its influence on the other policy objectives in order to enhance overall economic stability. This week’s editorial applies this line of thinking to assess the potential for coordination between monetary and fiscal policy in the pursuit of a common objective: price stability. Such a coordination would be very different from the traditional approach of monetary policy focusing on inflation and fiscal policy on other objectives.

When inflation is well below target on a sustained basis -such as post the Great Recession of 2008-2009-, this separation of roles implies that monetary policy may need to become extremely accommodative through a combination of official interest rates that reach the zero lower bound, quantitative easing and forward guidance, which signals that this policy will be kept in place for the foreseeable future. Likewise, when inflation is well above target, which corresponds to the recent experience, a very significant monetary tightening may be required by hiking official interest rates, quantitative tightening and dropping forward guidance by moving to a data-dependent approach.

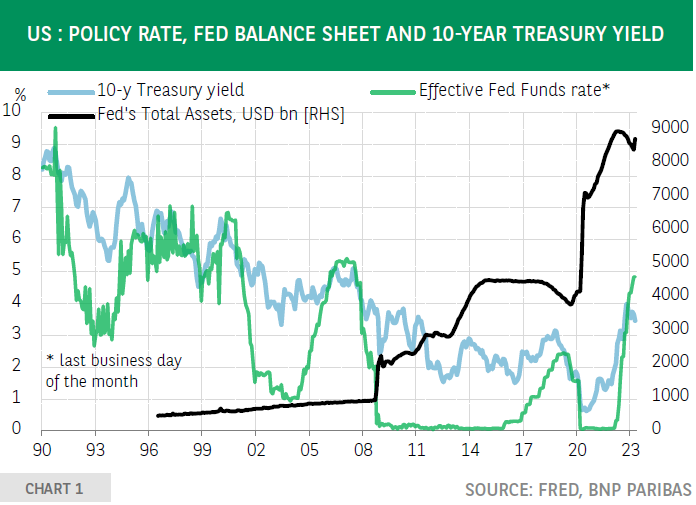

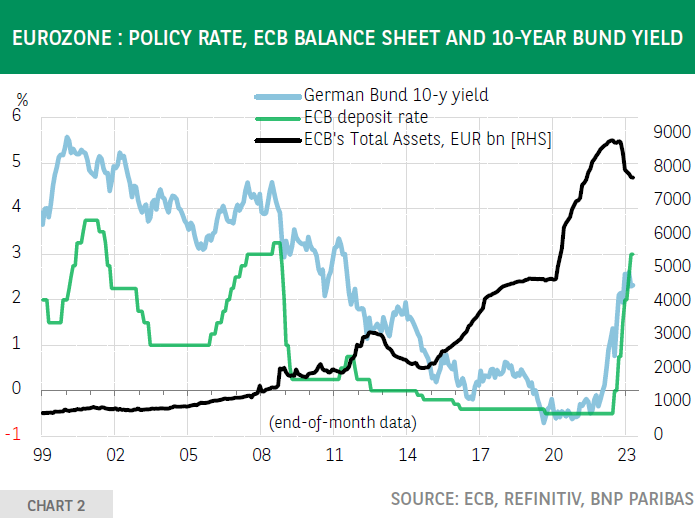

Consequently, over the course of a business cycle, market interest rates may drop significantly but rebound strongly thereafter (charts 1 and 2). Such a large cyclical amplitude of interest rates may have undesirable consequences for the economy and put financial stability at risk. Low policy rates and quantitative easing force financial investors to take more risk and aggressive rate hikes have the opposite effect.

A recent ECB paper studies the effects of low short-term interest rates on the optimal portfolio allocation of investors and introduces the concept of portfolio instability. This corresponds to “the amount of optimal portfolio shifts needed to respond to exogenous shocks to the expected risk and return of the risky portfolio assets.” Positive (negative) shocks to expected risk (return) trigger a pressure to reduce the exposure to riskier asset classes.

This pressure is stronger the lower the risk-free interest rate. Based on counterfactual analysis, the authors demonstrate “that the sell-off in riskier asset classes during the Covid crisis in March 2020 was more severe than would have been in the presence of higher short-term interest rates.”

The outcome is caused by two channels. First, low rates create an incentive to ‘climb the risk ladder’ and to increase exposure to assets with a higher expected return, which comes with higher risk. Two, a sustained period of very low official interest reduces the volatility of riskier assets because through forward guidance the central bank signals that rates will remain low for a long time.

Moreover, low rates are growth-supportive and reduce concerns about negative shocks to cashflows. Consequently, both channels “incentivise the build-up of large and leveraged risky asset shares during calm periods which need to be unwound in the event of higher market volatility.” ‘Climbing the risk ladder’ can also consist of increased duration exposure of fixed income investments. In this respect, the ‘dash for cash’ in the UK early October[2] last year and the recent problems of a small number of regional banks in the US[3] are concrete examples of the havoc that may be caused when bond yields rise strongly. As noted by Isabel Schabel of the ECB recently, “we are coming out of a very long period with very low interest rates. That was a period in which a number of financial fragilities were built up, which are now exposed by the rapid hiking cycle. Rising interest rates affect funding costs and asset prices, and they affect everybody at the same time, banks and non-banks. This poses challenges we need to take very seriously.”

Against this background, it seems commendable to coordinate monetary and fiscal policy. When inflation is too low (high), fiscal stimulus (restraint) could help in boosting (lowering) inflation and reduce the extent of monetary accommodation (tightening). Such an approach has been analysed in a recent ECB working paper. The authors simulate rule-based monetary and fiscal policies that react to a divergence of inflation from its target[6]. When inflation is too low, interest rates are cut and fiscal policy reacts countercyclically by increasing government spending. This coordinated approach lowers the frequency of hitting the zero lower bound of the policy rate, i.e. it reduces the optimal cumulative amount of rate cuts.

Fiscal policy can also be used to cool inflation. This was analysed by the IMF in its latest Fiscal Monitor. Using a model that takes into account inequality in incomes, consumption and asset holdings, the authors conclude that “a reduction in the fiscal deficit leads to a similar level of disinflation but requires a smaller increase in interest rates than when central banks act alone.” Moreover, “the analysis also shows that deficit reduction combined with transfers to the poorest yields a smaller drop in total private consumption and a consumption path associated with less inequality across households. These effects are even more important when public debt is high because fiscal restraint limits the rise in the cost of borrowing and reduces debt vulnerabilities.”

Based on the experience since the Great Recession and model-based simulations, there is a clear case for monetary and fiscal policy coordination in the pursuit of their common objective of price stability. However, putting this into practice would probably be very challenging.

Firstly, there is the question of calibration. When inflation is too low (high), the central bank, when deciding on the extent of monetary easing (tightening), will need to make an assumption about the effectiveness of fiscal stimulus (restraint) in generating more (less) inflation. Secondly, joint communication will be important to make sure that economic agents, when forming their inflation expectations, take into account the monetary and the fiscal policy decisions.

Clear communication must avoid the impression that the central bank is not doing enough to address the inflation issue because this could cause an unanchoring of inflation expectations. Thirdly, there may be concern that fiscal easing when inflation is too low would, for political reasons -upcoming elections, a new government- not be turned back when inflation has reached its target.

A rule-based fiscal policy would allow to address this issue, but what would be the credibility of such a rule? Finally, there may be concern that this would open the door to fiscal dominance and that monetary policy decisions, particularly when inflation is above target, would become influenced by the shape of public finances.

To conclude, in its latest World Economic Outlook, the IMF noted that “as inflation returns to target, the effective lower bound on interest rates may become binding again […]. This could limit central banks’ ability to respond to negative demand shocks.” According to the IMF, this could trigger the reemergence of a debate about the appropriate level of target inflation. With this in mind, having a debate on the pros, cons and feasibility of a coordination between monetary and fiscal policy would also be useful.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.